Danish legal system is based on civil law and provides for judicial review of legislative acts. Denmark accepts compulsory International Court of Justice jurisdiction with reservations.

The principal forms of business organization in Denmark are:

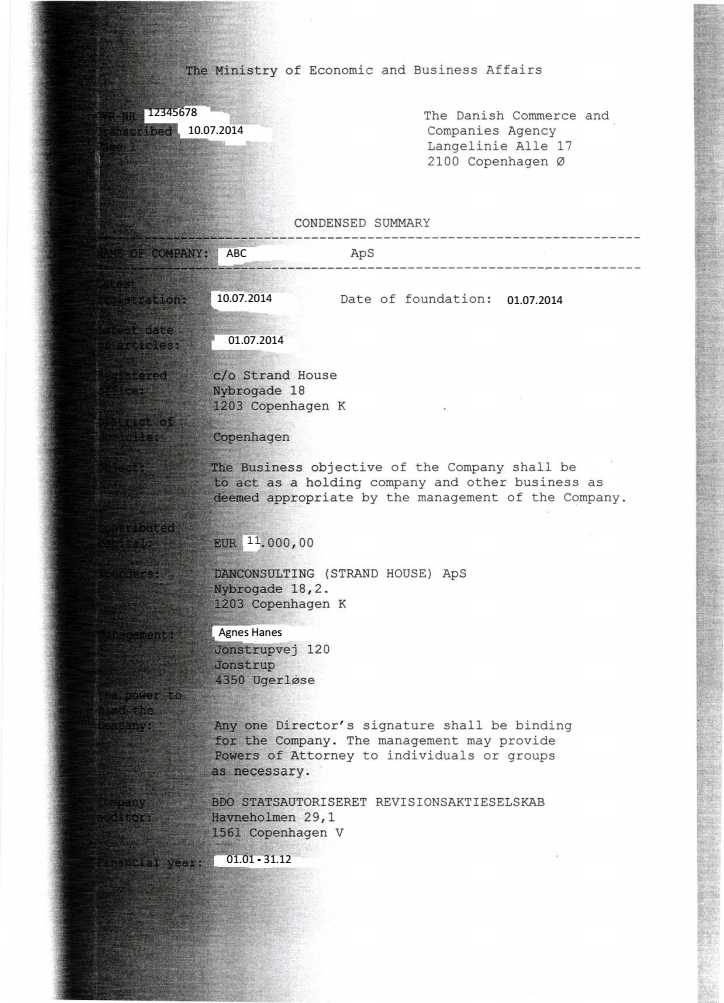

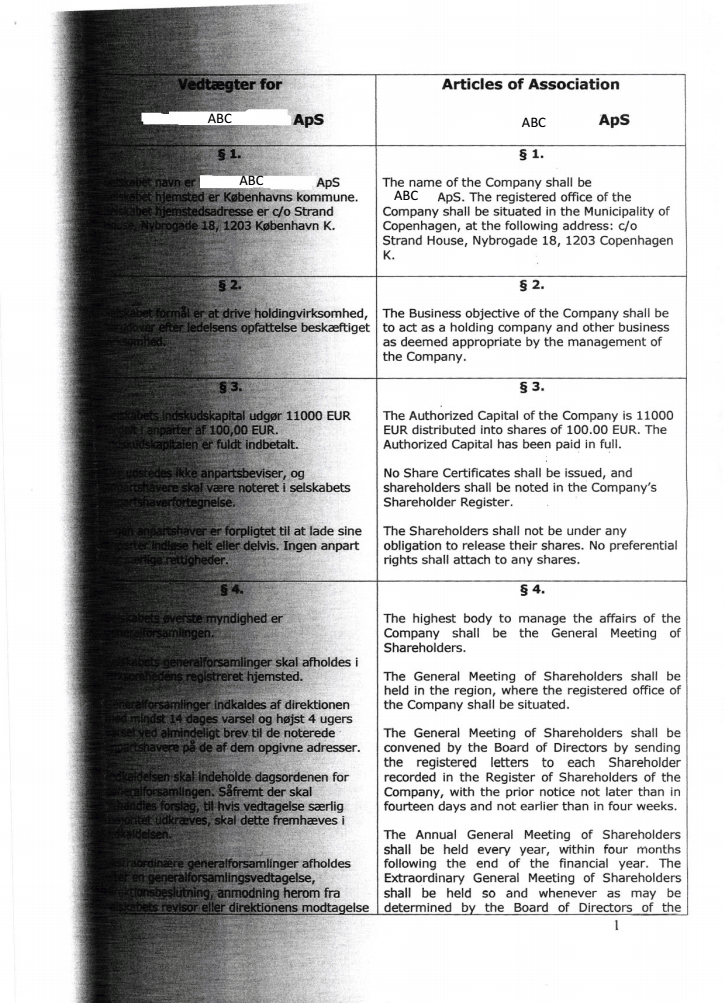

The most common structure is the Private Limited Company (Anpartsselskab, ApS).

The company must have a name ending with a suffix ‘ApS’.

Company names may be expressed in any language using the Latin alphabet if the Commerce and Companies Agency is in receipt of a Danish or English translation. Names in Cyrillic alphabet are not allowed.

The Commerce and Companies Agency can decline any name it considers undesirable or any name that is identical or similar to an existing company’s name, or implies illegal activity or royal or government patronage.

The following names, their derivatives or foreign language equivalents require consent or a licence: “Bank”, “Building Society”, “Savings”, “Loans”, “Insurance”, “Assurance”, “Reinsurance”, “Fund Management”, “Investment Fund”, “Trust”, “Trustees”, “Chamber of Commerce”, “Co-operation”, “Council”, “Municipal”, as well as any other names that may suggest association with the banking or insurance business.

To incorporate a company in Denmark the following steps are required:

1. Obtain a NemID signature: The NemID can be obtained online on www.nemid.nu. The new NemID was launched in July 2010 as an improvement on the previous Digital Signature.

2. Deposit startup capital at a bank: A private limited company (ApS) must have a startup capital of at least DKK 80 000. An amount equal to 25% of the share capital, but not less than DKK 80 000, must be paid up at all.

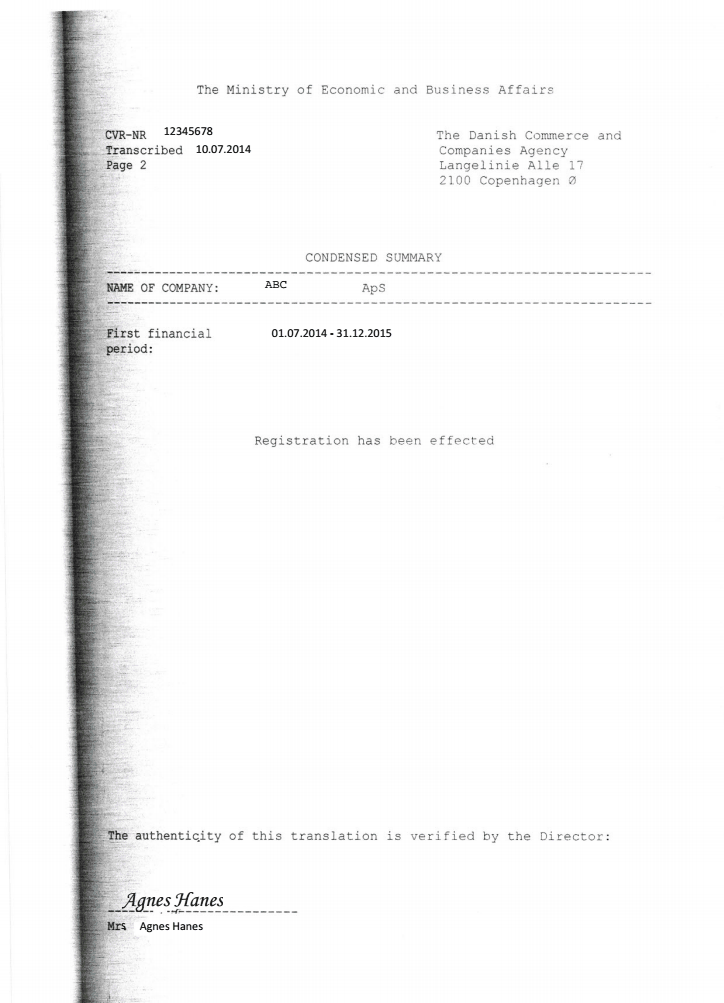

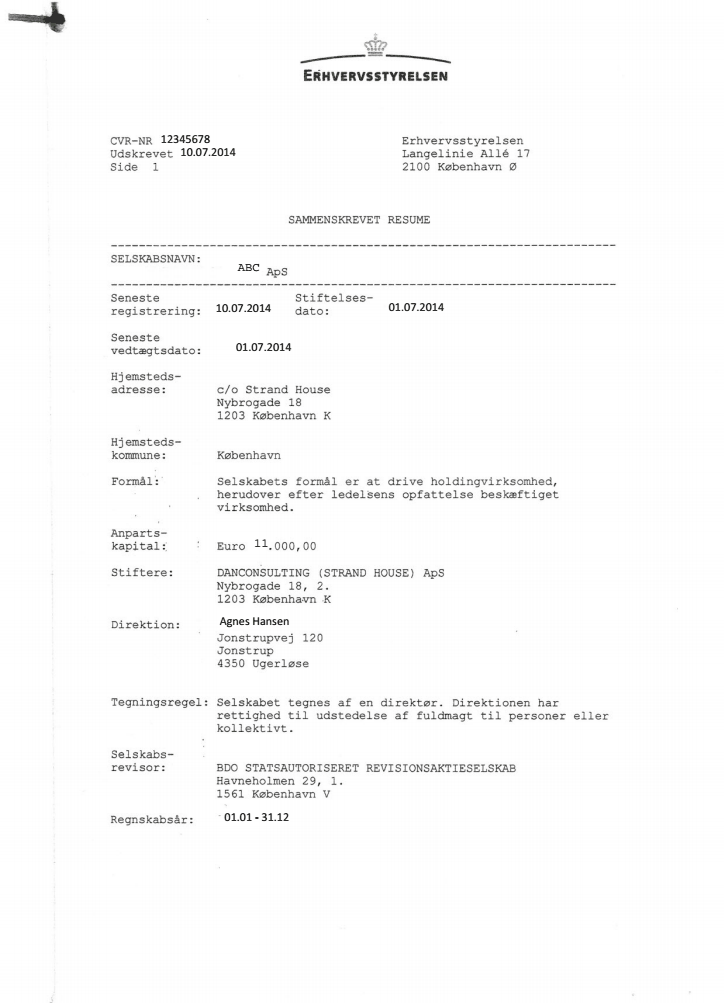

3. Register the company with the Danish Business Authority (DBA) Webreg system: The DBA provides to limited liability companies, a one-stop centralized service for business and tax registrations. The website www.webreg.dk captures new and updated company information and it is connected to a database that automatically validates the input data. The registration form may be completed and submitted electronically with the Memorandum of Association and the Articles of Association. The entire process takes place online, without the involvement of any agency official. For online registration, the registration is immediate. To secure payment of the startup capital, lawyers, accountants or bank employees may log on to the Capital Information page on www.webreg.dk and confirm the type and amount of capital by using their NemID (digital signature). On completion of the registration process, the client receives a registration receipt by email, stating a unique business identification number (CVR) and confirmation that the registration is visible at www.cvr.dk, where the National Gazette is published electronically.

4. Register employees with workmen's insurance: Employees must be insured against industrial accidents and occupational illnesses. The chosen insurance company must complete a form and register the insurance policy with the DBA. If the new business has a car, motor insurance must also be purchased. More information on insurance companies can be found at www.forsikringogpension.dk.

It takes about 5 days to startup a new company in Denmark.

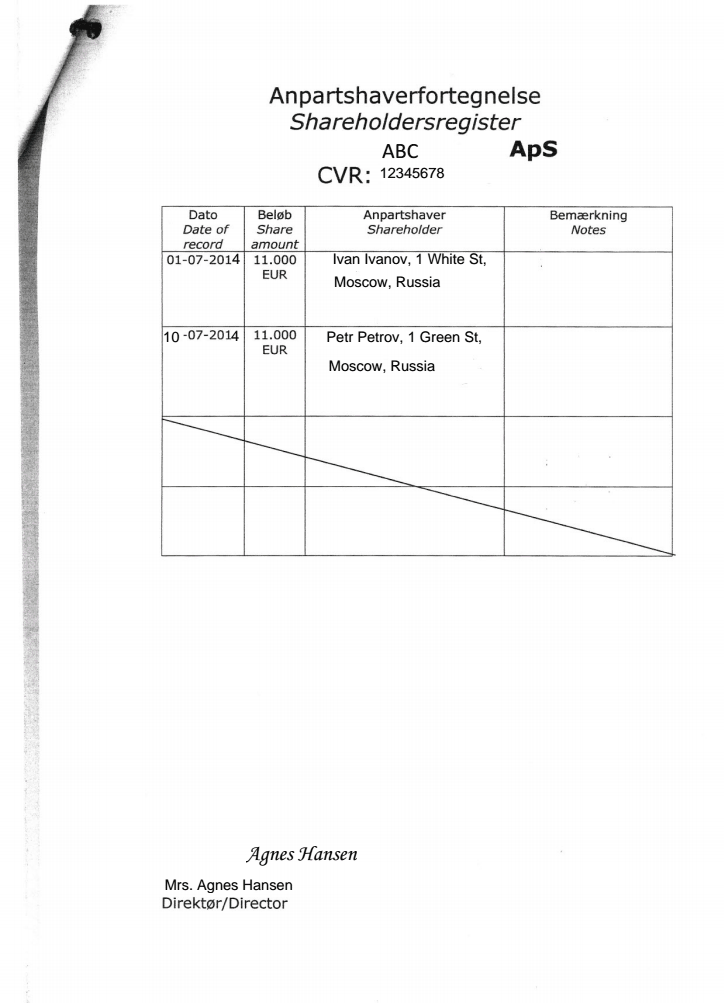

Danish ApS must maintain a registered office address within Denmark and keep at that address the register of shareholders.

There are no mandatory requirements regarding the company seal.

The redomiciliation of companies either to or from Denmark is not permitted.

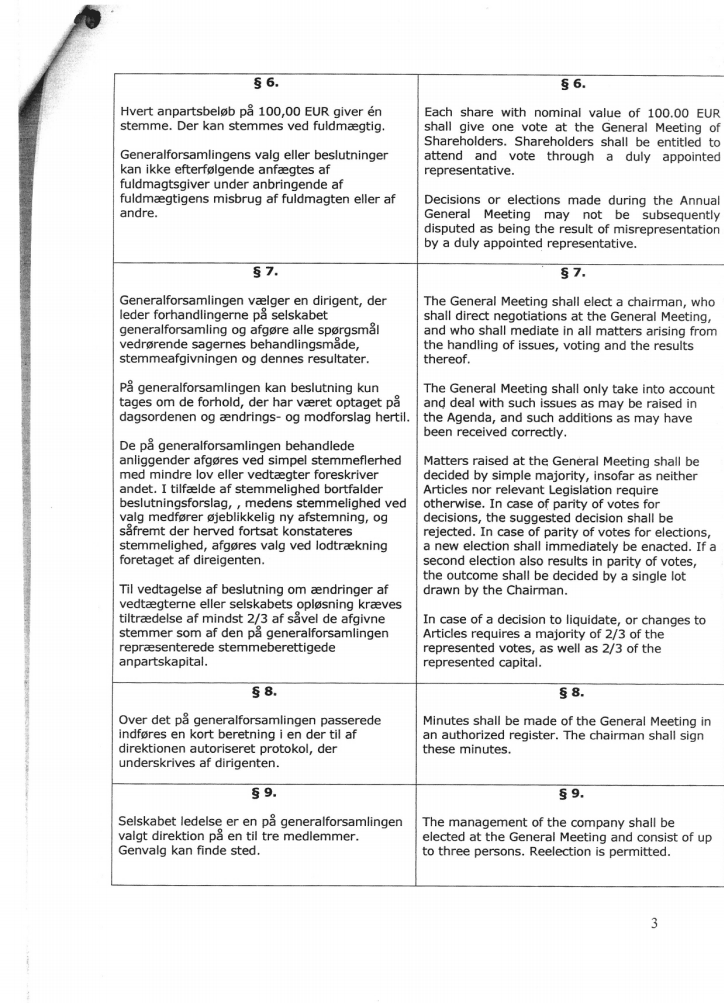

A private limited company is required to have a minimum of one director who may act either as a managing director or a sole member of the board of directors (or both). Such director may be of any residence or nationality, a natural person or a legal entity.

Director’s details are disclosed to the local agent and appear on the public file.

There are no restrictions on how often or where directors’ meetings should be held.

Danish companies are not required to appoint a company secretary.

ApS may have one or more shareholders, individuals or corporations of any nationality or residence.

Shareholders’ details are disclosed to the local agent and appear on the public file.

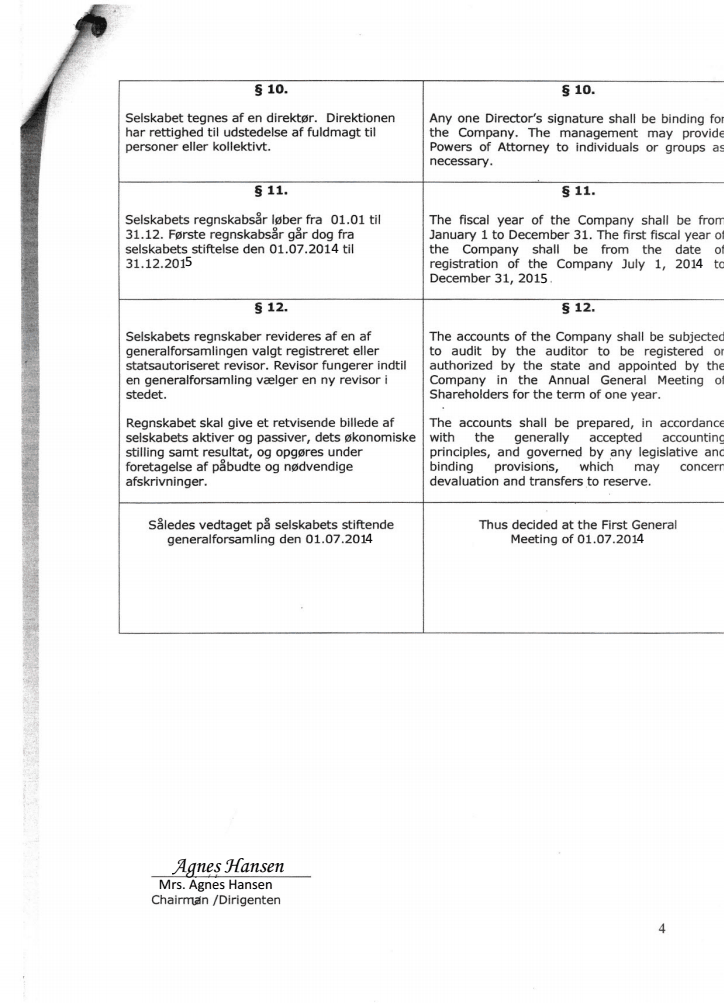

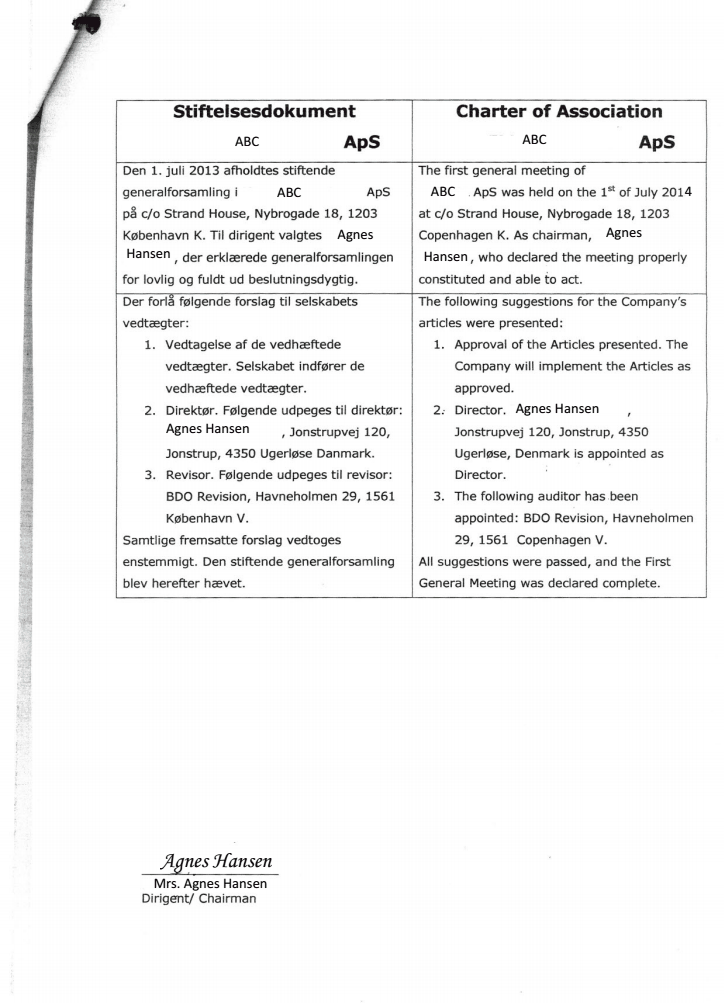

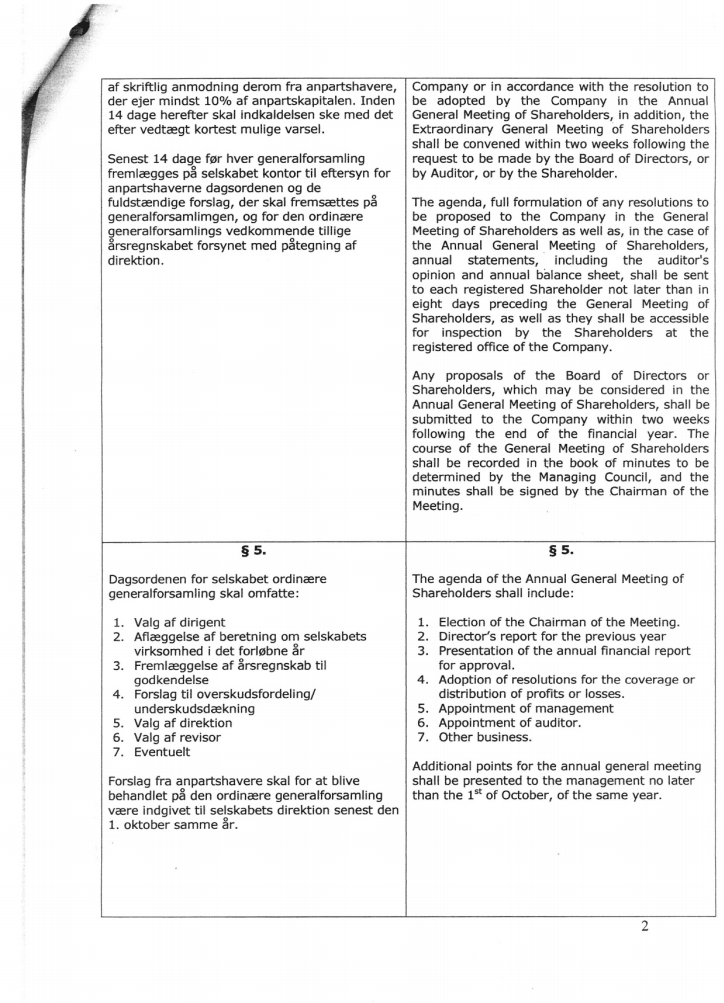

General meetings are to be held either in Denmark or abroad annually. By unanimous decision, the shareholders of a company may agree to waive the formal requirements of the Companies Act and the company’s articles of association applicable to general meetings and sign a written resolution.

A company may also elect to introduce electronic communication between the company and its shareholders, e.g. by convening general meetings by e-mail.

The register of beneficiaries in Denmark is public. They can be obtained from the official website of the Registry of Companies free of charge and without registration.

The following information about the beneficiaries is disclosed: full name, address of residence, basis of ownership, date of last change of data.

The obligation to provide data for the Beneficiary Registry is effective as of December 1, 2017.

The share capital of a private limited company can be nominated in DKK or EUR (or another currency if permission to use another currency has been obtained).

The minimum authorized and issued share capital of DKK 80 000 An amount equal to 25% of the share capital, but not less than DKK 80 000, must be paid up at all.

Usually the share capital is DKK 80 000 and the standard par value of shares is DKK 100.

Bearer shares or shares with no par value are permitted.

The company registration system is now fully computerised and a fair amount of information is, upon payment of a fee, available online to any interested party. This information includes:

Copies of annual reports are also available online whereas copies of articles of associations, minutes of general meetings etc. may be available by ordinary mail within a few days (or by fax the same day on payment of an additional fee).

Price17 200 USD

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and Danish Business Authority incorporation fee

Price6 200 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 700 USD

Paid-up “nominee director” set includes the following documents

Paid-up “nominee shareholder” set includes the following documents

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD