Hong Kong's legal system is completely independent from the legal system of mainland China. In contrast to mainland China's civil law system, Hong Kong continues to follow the English Common Law tradition established under British rule. On the top of law hierarchy is Basic Law of Hong Kong (Constitution of HK), adopted in 1990. Hong Kong has its own administrative governance, legislation, independent court procedure and supreme judicial authority.

The major corporate law is Companies Ordinance.

The principal forms of business organization in Hong Kong are:

The most common and suitable type for foreign businessmen to incorporate their business is a private company limited by shares.

Generally, any company can be registered if it is not identical with already registered and specified names in the Registrar of Companies. You can check a name for availability at Companies Registry’s Cyber Search Centre free of charge.

Company name can be registered in Chinese, English or both. but a combination of English words/letters and Chinese characters in a name is not allowed. However, it is not allowed to use Chinese and English symbols in the name. Chinese company names shall be registered in full characters, used in Hong Kong. Names in Cyrillic alphabet are not permitted.

The suffix to denote limited liability in company names is ‘Limited’, its short form ‘Ltd’ is not allowed as Companies Ordinance requires that the English company name must end with ‘Limited’.

The company name will not be registered if it is identical or similar to that of an existing company, if its use would constitute a criminal offence, or is offensive or otherwise contrary to the public interests. The following names and their derivatives require approval or a license: words which are likely to give the impression that the company is connected in any way with the Central People’s Government or the Government of Hong Kong or any department of either government: Department, Government, Commission, Bureau, Federation, Council, Authority; words and expressions that are covered by other legislation: Bank, Stock Exchange, Unified Exchange; Assurance, Insurance, Re-insurance; Certified Public Accountant (C.P.A.), Public Accountant (P.A.); other words: Building Society, Chamber of Commerce, Cooperative, Kaifong, Mass Transit, Municipal, Savings, Tourist Association, Trust, Trustee, Underground Railway.

To register a private company limited by shares, you need to go through the following procedure:

1. choose a name for your company;

2. register incorporation and business;

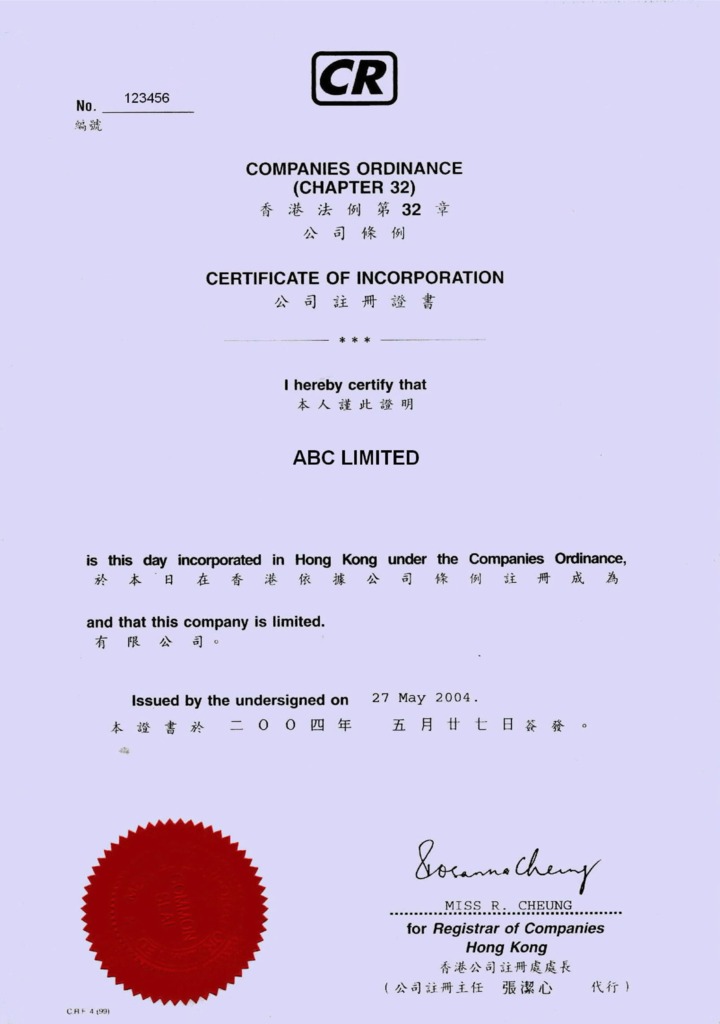

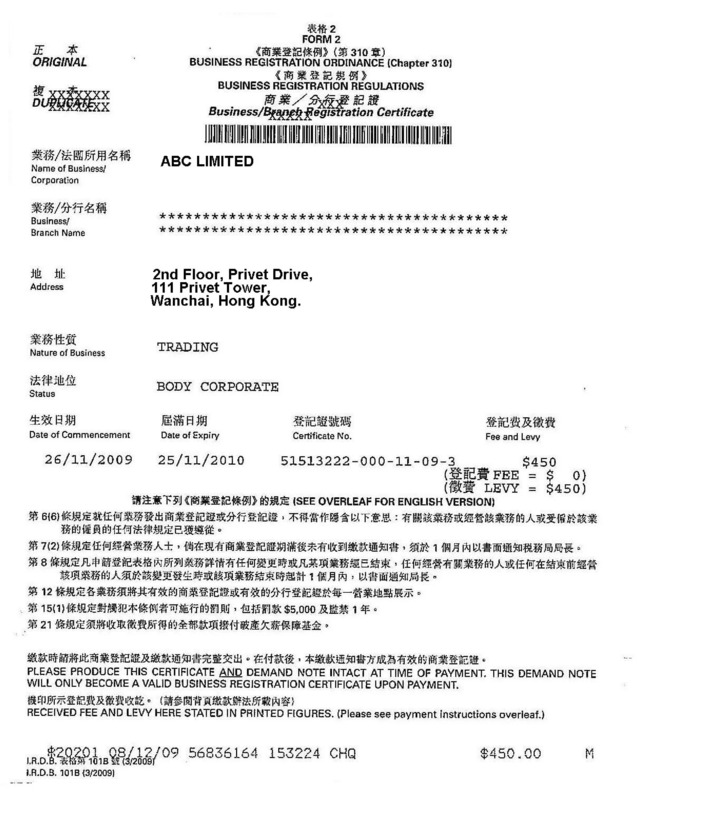

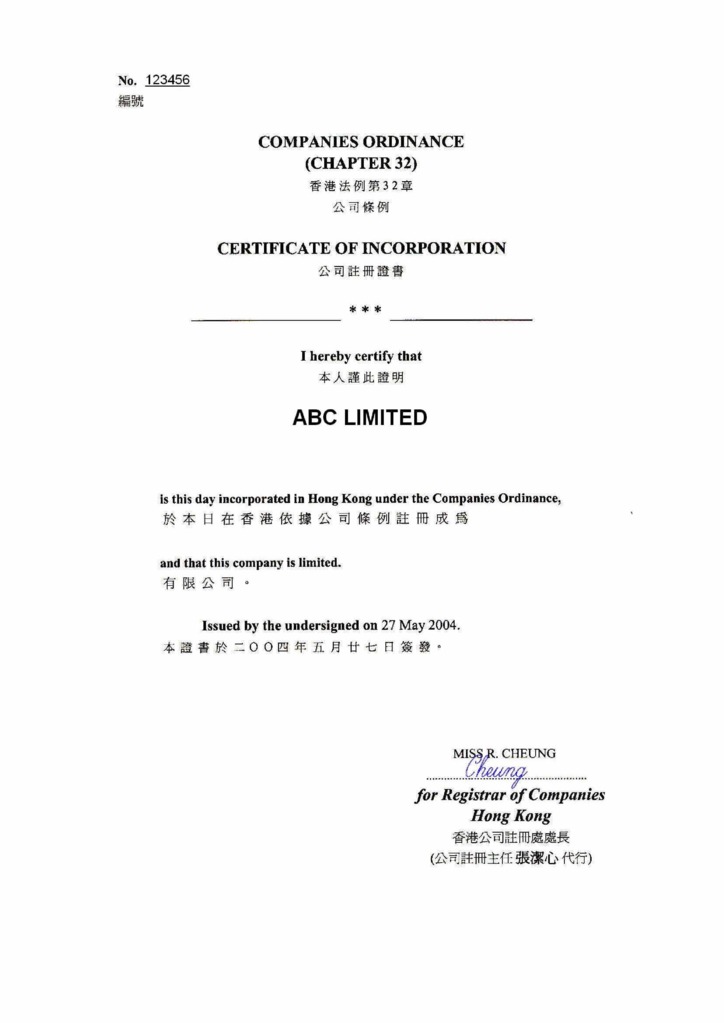

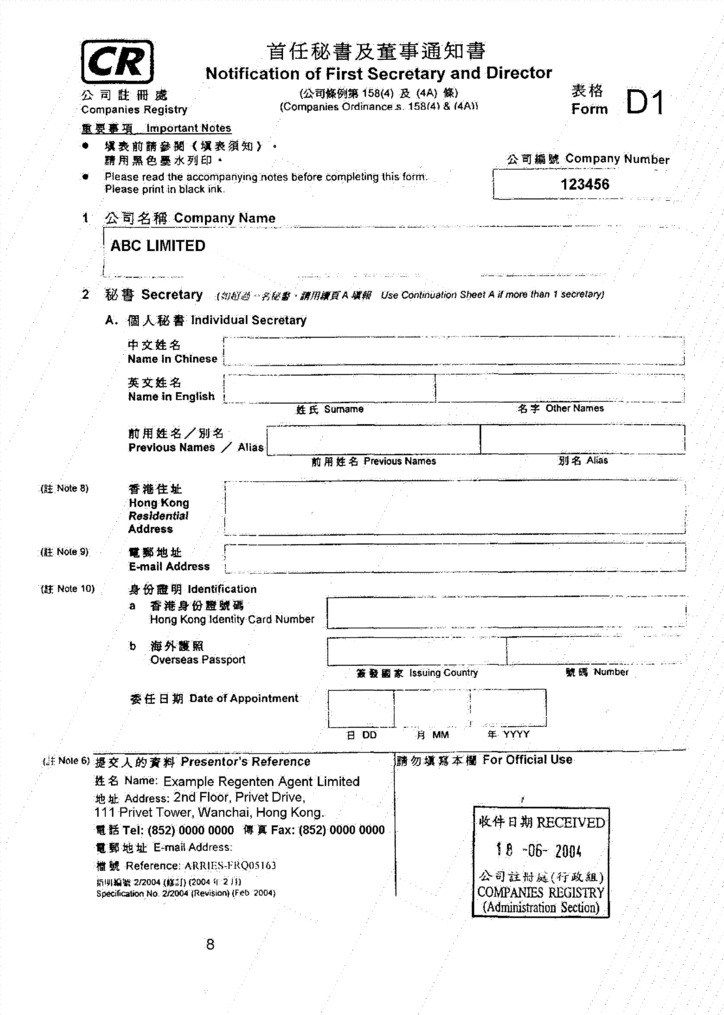

Any application for company incorporation includes a simultaneous application for business registration. If an application is accepted, Registration Office will issue Incorporation Certificate and Business Registration Certificate. You may simply submit the following documents online at the CR’s e-Registry with the correct fee:

3. obtain certificates and licenses.

Business Registration Certificate is issued for one or three years. If a type of business activity changes, a company should notify Inland Revenue Department in writing within a month. Only specific types of activities (e.g. restaurants, banks, tour agencies) need additional licenses.

Business registration certificate is issued in both hard and electronic copy (for online procedure). Both copies are equally valid..

As a rule, it takes four working days to issue an incorporation certificate and business registration certificate. When the documents are ready, the applier is notified by e-mail and has to arrive at Registration Office to get it. Electronic version may be ready within 24 hours.

There are a number of restrictions on the activities of a private company. It cannot undertake the business of banking or insurance or solicit funds from or sell its shares to public, unless a special permission is granted.

Hong Kong companies have a right to open banking accounts in Hong Kong and abroad. Banks in Hong Kong normally require a minimum deposit. This is typically around HK$2,000. Banks may request identity and residence information for all beneficial owners of the company before they will open an account.

Local registered office

Hong Kong companies must maintain a registered office in Hong Kong at which the following information and documents would normally be kept: registration certificate; register of directors and secretaries; register of members; books containing the minutes of proceedings of any general meeting, any meeting of directors or any meeting of managers; register of holders of debentures; a copy of every instrument creating any charge requiring registration; register of charges, and other. The companies may also choose a place other than registered office, but within Hong Kong, to keep these documents at, with notice of such place to be given to the Registrar.

Seal

Every Hong Kong company must have as its common seal a metallic seal with its name engraved in legible characters on it. A company whose objects require or comprise the transaction of business outside Hong Kong, may have for use in any territory, district, or place not situated in Hong Kong, an official seal, which shall be a replica of the common seal of the company, with the addition of the name of every place where it is to be used.

Renewal

Renewal of Hong Kong companies is held annually and normally includes the following fees

The redomiciliation of companies either to or from Hong Kong is not permitted.

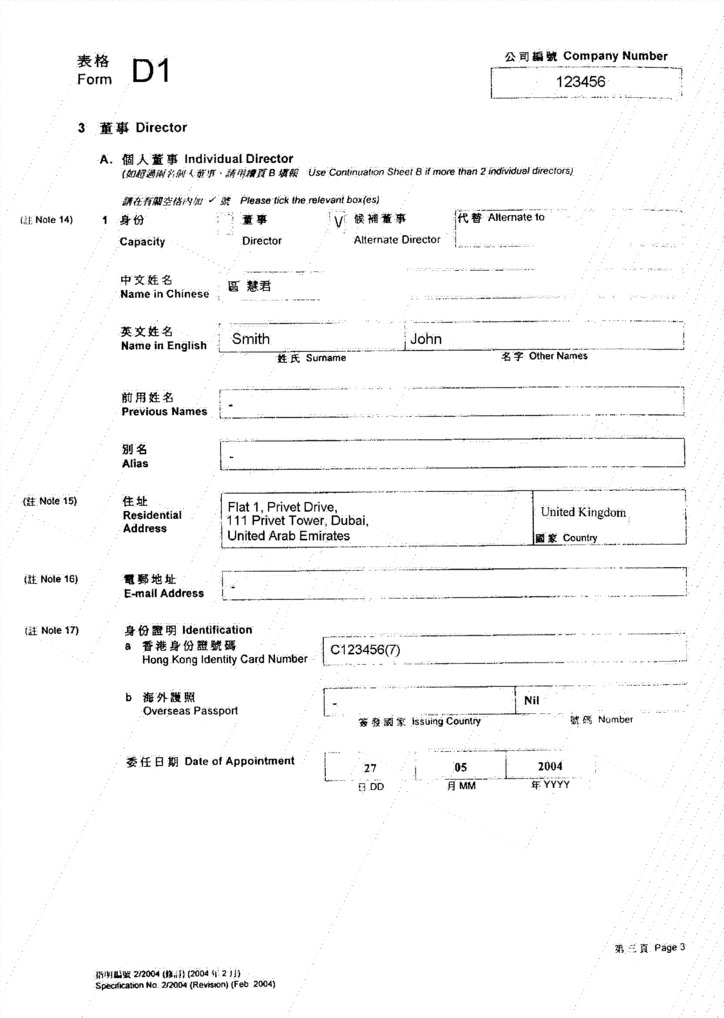

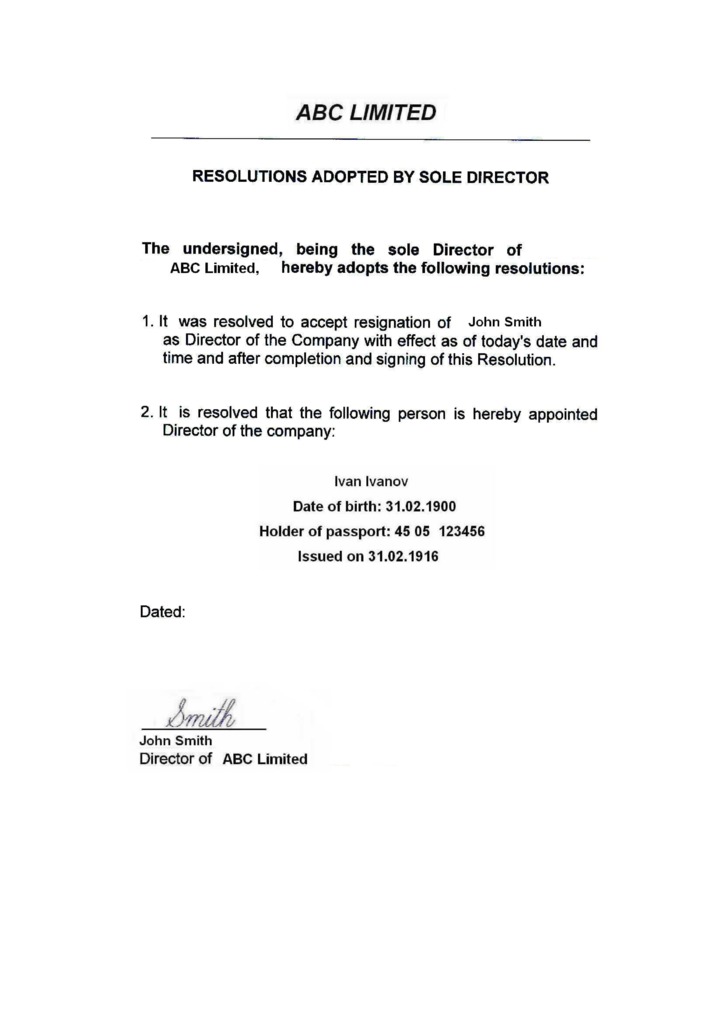

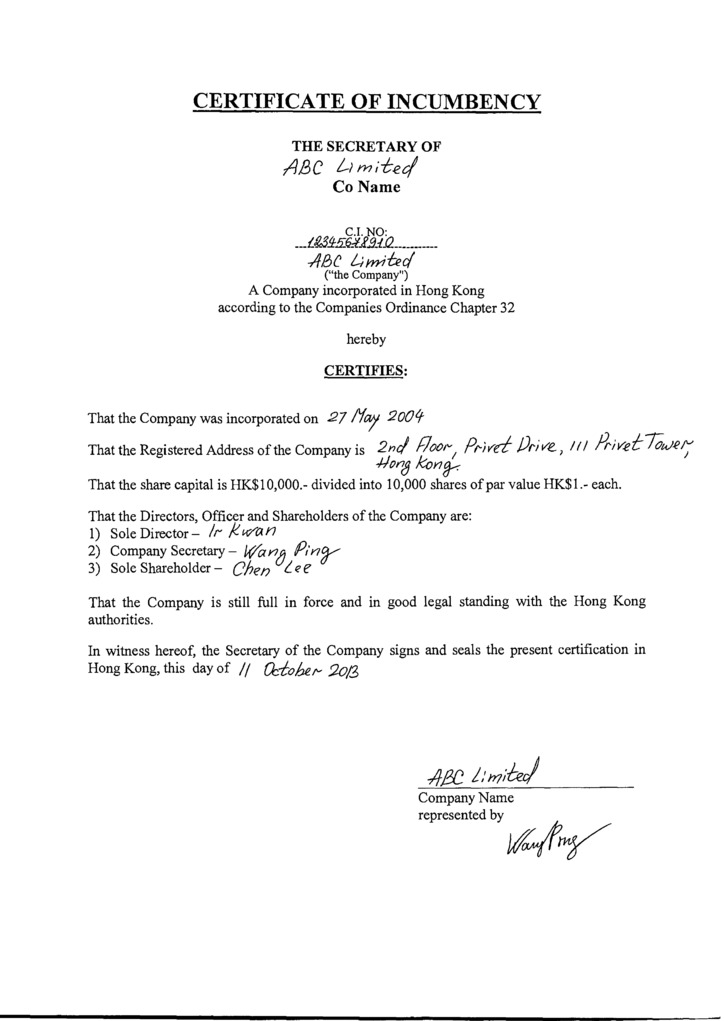

A Hong Kong company is required to have a minimum of one director who can be a natural person or a body corporate (corporate directors are allowed for companies that are not subsidiaries of public listed companies), a resident or non-resident. Director’s details are disclosed to the local agent and appear on the public file. In the meantime, at least one director should be a natural person. The board meetings may take place in Hong Kong or anywhere in the world.

All Hong Kong companies must appoint a company secretary who may be a natural person or a body corporate, but must be resident in Hong Kong. There are no special requirements for qualifications of the secretary. The law prohibits that the sole director of a private company be appointed as secretary. Besides, no private company having only one director may have as secretary a body corporate, director of which is a sole director of the private company.

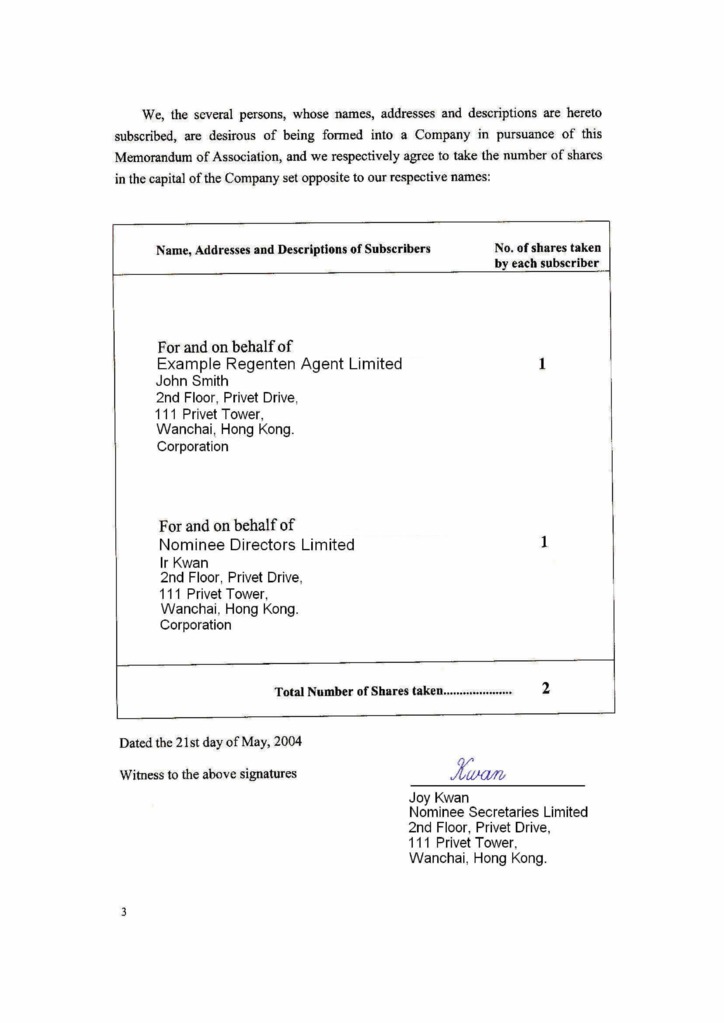

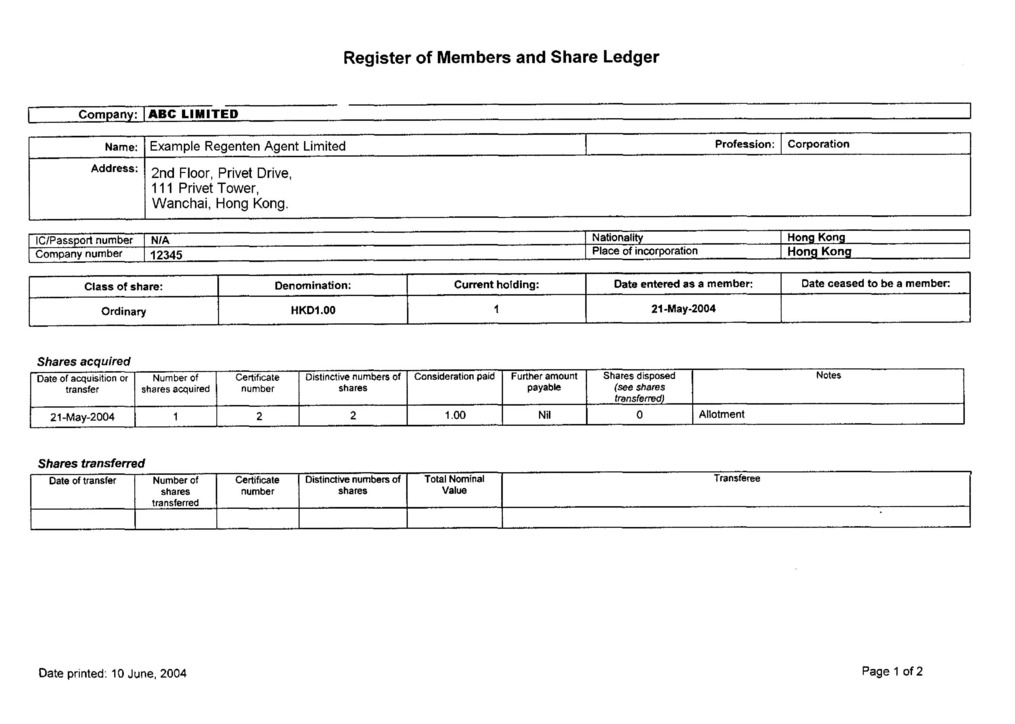

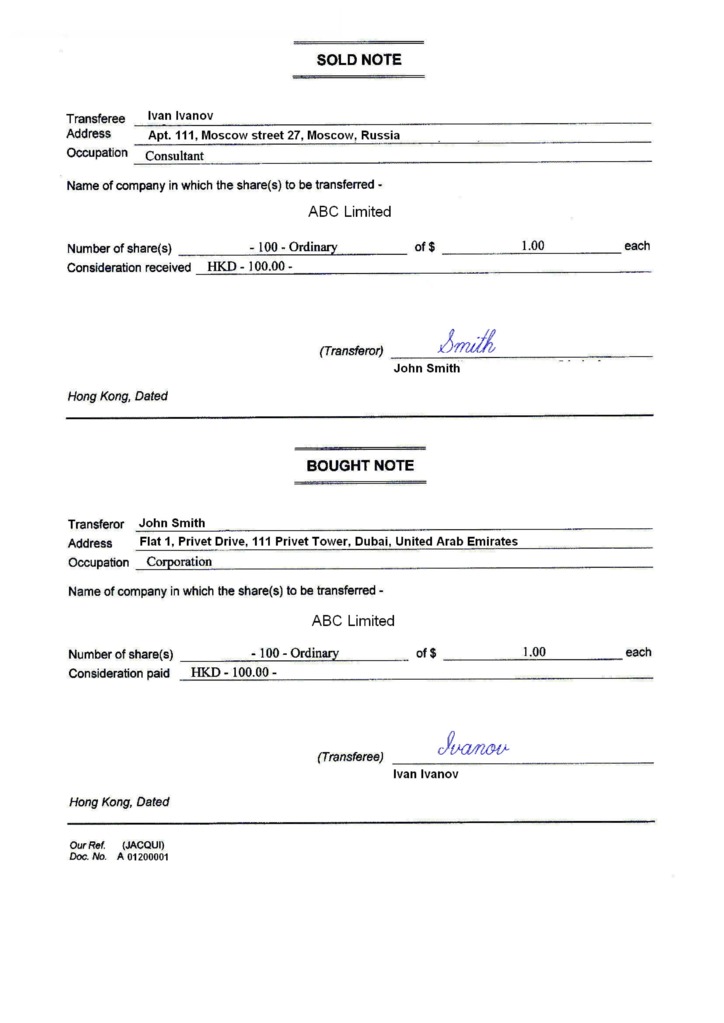

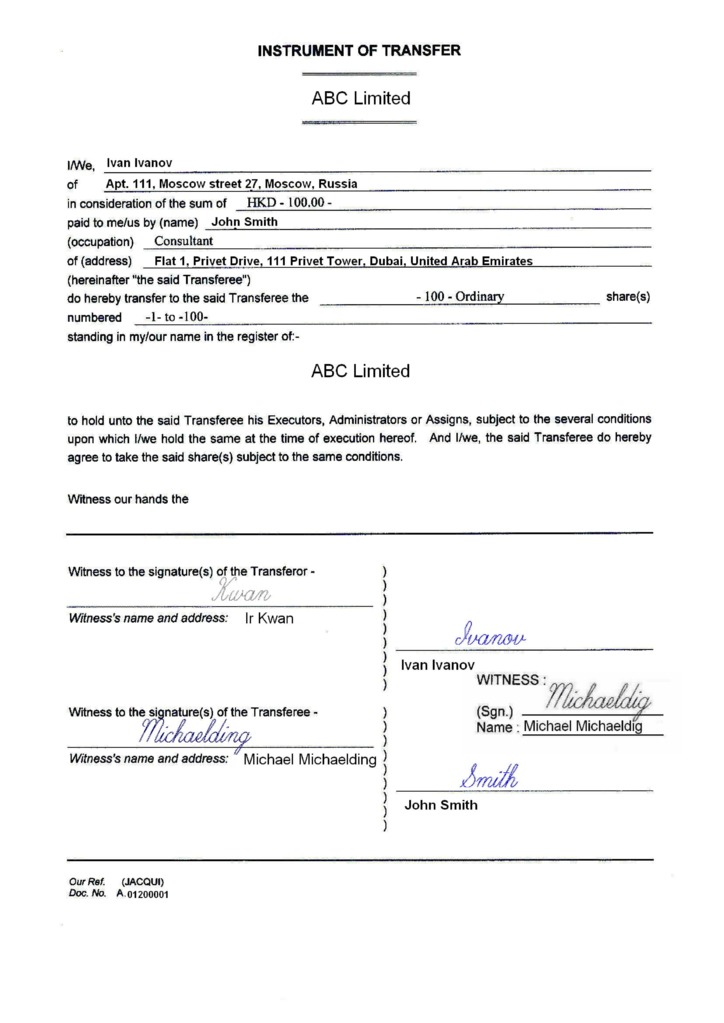

Hong Kong companies may have one or more shareholders, individuals or corporations of any nationality or residence. Sole shareholder can be director of the company. Shareholders’ details are disclosed to the local agent and appear on the public file. General meetings are to be held either in Hong Kong or abroad annually, with the first annual general meeting to take place within eighteen months of the company’s incorporation, and the following meetings to be held in 9 months after the end of financial year. At a general meeting director are to report about profit and losses, as well as balance sheet for the previous financial year.

The identity of the beneficial owner of a Hong Kong company is disclosed to the local agent and the auditor, and can only be disclosed by them in the cases stipulated by law and following statutory procedure. Besides, a bank may request information on beneficiary before opening an account.

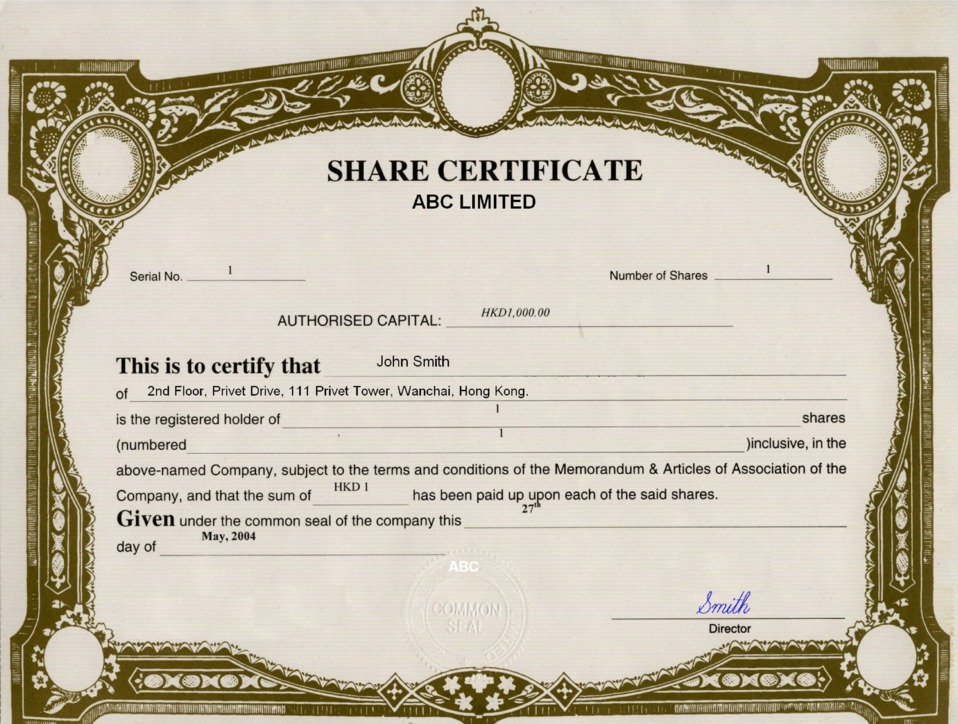

The share capital of a private limited company can be nominated in any currency. There is no minimum authorized share capital as the law simply provides for a minimum of one share to be issued and paid immediately upon issue or within time specified in the relevant resolution. No payments deadlines are set for the authorised capital. Usually the share capital is HKD 10,000 which is divided into shares of HKD 1.00 each. Bearer shares or shares with no par value are not permitted.

<h3>DISSOLUTION AND RESTORATION</h3>

A Hong Kong company limited by shares can be dissolved in the following two ways:

1. Liquidation/Winding Up

The winding up of a company may be either:

Winging-up by the court

A company can be ordered winding-up by the Court. The common reason for this type of winding-up is its inability to pay its debits. The company is deemed unable to pay its debts if has a debt exceeding HKD 10,000 and fails to pay it or make arrangement with creditor(s) which is accepted by them within three weeks of receiving their written demand.

Voluntary winding-up

Voluntary winding up of a Hong Kong company can be initiated either by members (shareholders) or creditors. The voluntary winding up of a company begins by a special resolution being passed for the company to be voluntarily wound up and publishing this information in the Gazette within 14 days. The winding up is said to begin on the date on which the resolution is passed.

• Members’ voluntary winding-up

A members’ voluntary winding up of a company can be carried out if the directors believe that the company will be able to pay its debts, in full, within 12 months after the commencement of the winding up.

To initiate such a winding up, a directors’ meeting must first be convened where majority of the directors must make a statutory Declaration of Solvency. The Declaration of Solvency must also contain the statement of assets and liabilities, based on the most recent financial statements of the company. The Declaration must be delivered to the Companies Registry within seven days of its making.

The directors then appoint a provisional liquidator, who is generally a solicitor or professional accountant. The notice of the appointment of the provisional liquidator and notice of the commencement of the winding up by virtue of delivery of the Declaration to the Companies Registry must be published in the Gazette within 14 days of the appointment of the provisional liquidator.

Within 28 days of delivering the Declaration of Solvency to the Companies Registry, the directors must convene an Extraordinary General Meeting for passing a Special Resolution to wind up the company, and an Ordinary Resolution appointing the liquidators. The company should, within 14 days of passing the special resolution for voluntary winding up, give notice of the resolution by advertising in the Gazette. The voluntary winding up is deemed to have commenced with the passing of the special resolution at the Extraordinary General Meeting. The liquidator will proceed to wind up the affairs of the company and file the necessary notifications required under the Companies Ordinance.

Once the company’s affairs are fully wound up, the liquidator must prepare a final account of the winding up, showing how the property of the company has been disposed of and how the winding up has been conducted. The account must be presented at a final general meeting. A copy of the account, along with a return stating that the meeting was held, must be sent to the Companies Registry within one week after the meeting. The company will be dissolved three months after the Registry receives the documents or at a later date as set by a court order.

• Creditors’ voluntary winding-up

When directors of the company do not believe that it will be able to pay off the debt, a creditors’ voluntary winding up will have to be executed. Soon after the meeting at which the resolution for a voluntary winding up is made, a creditors’ meeting should be convened. The company must advertise notice of this meeting in the Gazette and two local newspapers (one English language paper and one Chinese). The directors must present a complete picture of the company's affairs, along with a list of creditors of the company and the estimated amount of their claims. The creditors will then proceed to appoint a liquidator and may also appoint a committee of inspection whose role is to act in concert with the liquidator. The liquidation process is similar to that of a members’ voluntary winding up, as mentioned above.

Winding-up will take about one year and the company cannot be re-opened after dissolution.

2. Deregistration

If a private company, which is defunct and solvent, wants to cease its business, it must officially apply to the Companies Registry to deregister it from the register of companies. In order to do so, it must meet certain requirements:

Deregistration is a relatively simple, inexpensive and quick procedure for dissolving defunct private companies. An application for deregistration can be made to the Registrar of Companies in the specified form. However, there is no statutory provision for making an application to the Registrar of Companies for striking off. This is a statutory power conferred on the Registrar of Companies to strike the name of a company off the register where he has reasonable cause to believe that the company is defunct and the company shall be dissolved when its name is struck off the register of companies.

Reinstatement of a struck-off company should be fulfilled with application at court within twenty years from publication in the Gazette of the notice of strike off. Provided that the court is satisfied that the conditions in the law are fulfilled, it will issue an order of reinstatement which will be filed with the Registrar. The company is then considered as never struck off (as if always have continued in existence). And the court may by the order give such directions and make such provisions as seem just for placing the company and all other persons in the same position as nearly as may be as if the name of the company had not been struck off. So the court order has a pretty strong effect for the protection of a member of the company, a creditor or the company itself. It is also useful to know that the strike off does not mean the liability for the directors or a member is eliminated during the strike-off.

The conditions for reinstatement checked by the court are: if the company was at the time of the striking off carrying on business or in operation, or otherwise if the court deems just to reinstate it. So the conditions are not demanding or strict, they are rather loose and discretionary on the court (‘deems just’).

Price2 500 USD

including the preparation and provision of the originals of the company's founding documents and an apostilled copy of such documents, documents formalizing the issue of shares, as well as the company's seal, NOT including client verification - Compliance fee

PriceIncluded

Price1 740 USD

including the provision of a legal address, excluding reporting services, NOT including client verification - Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 750 USD

Price640 USD

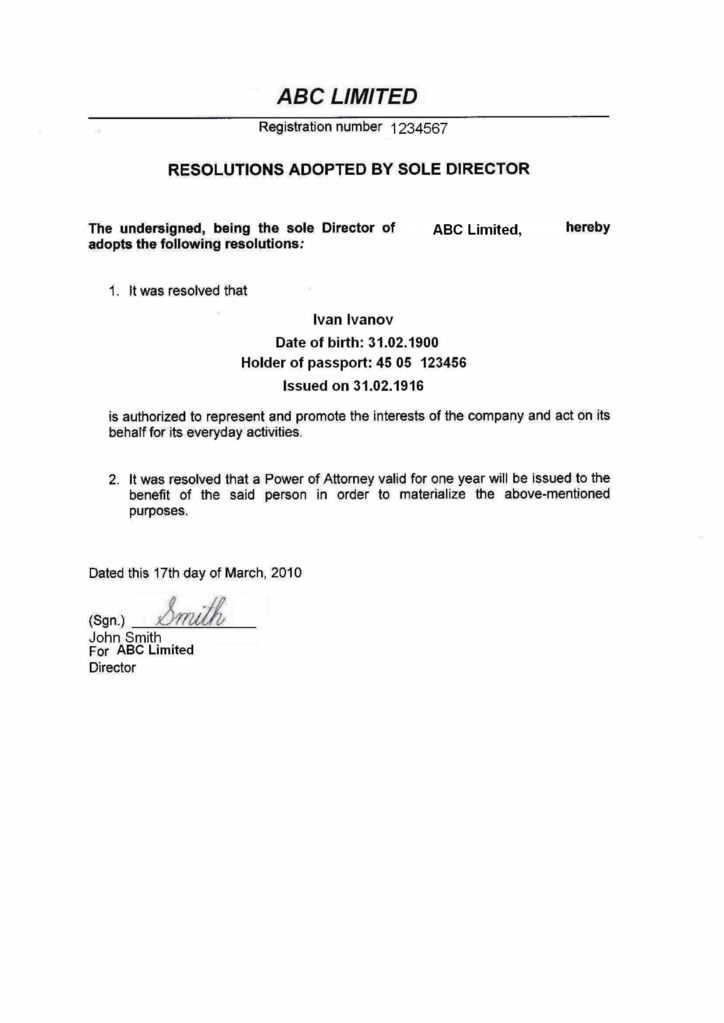

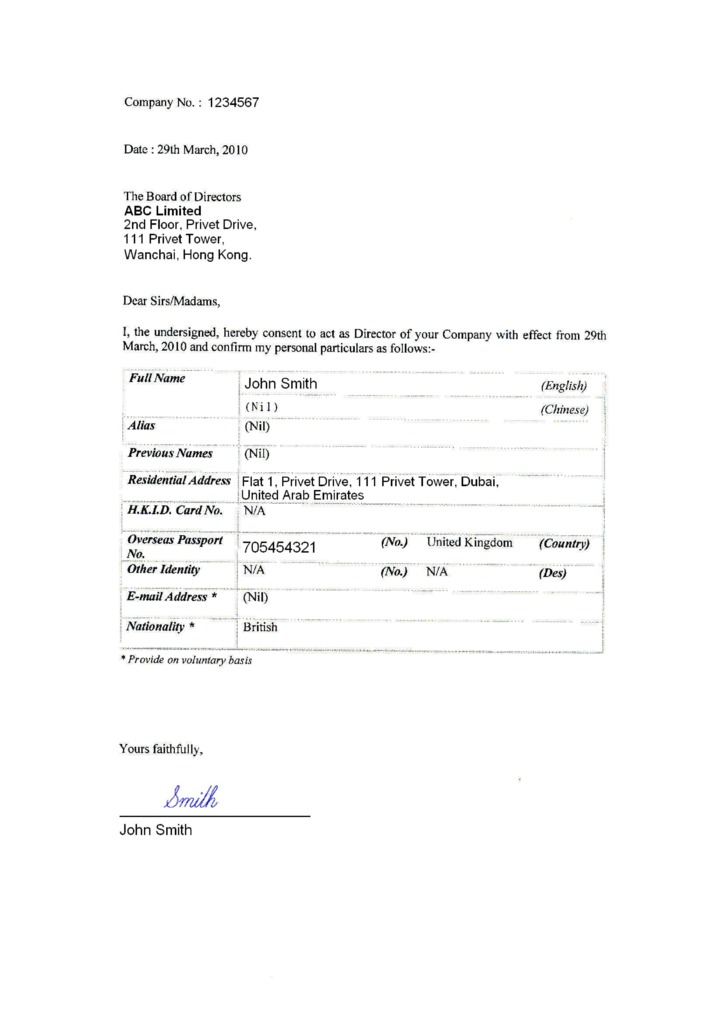

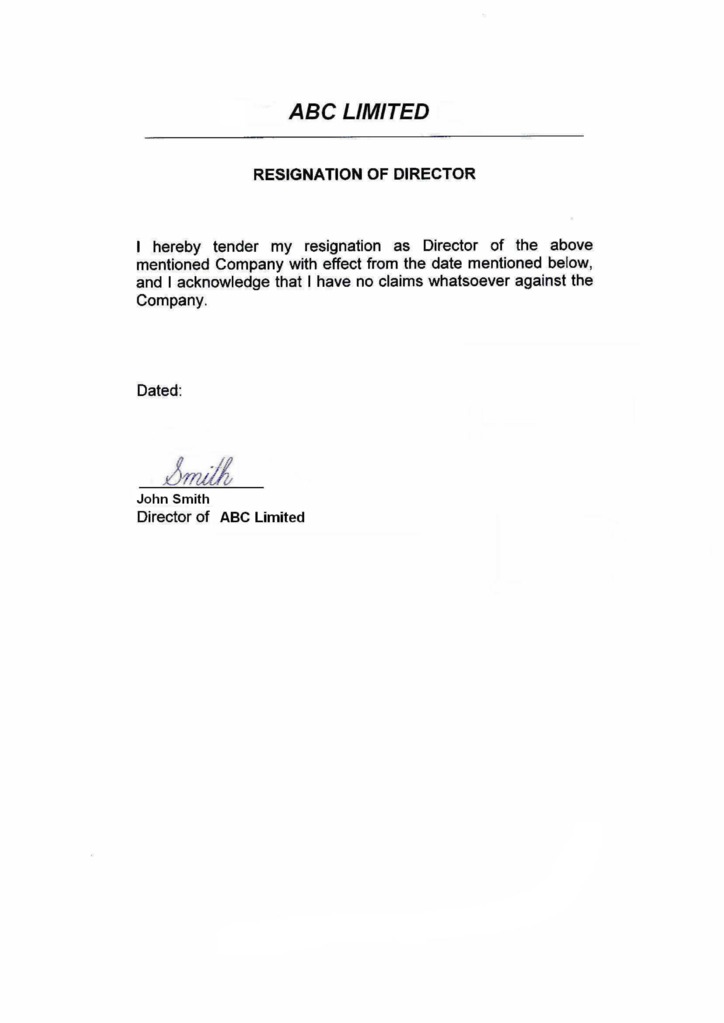

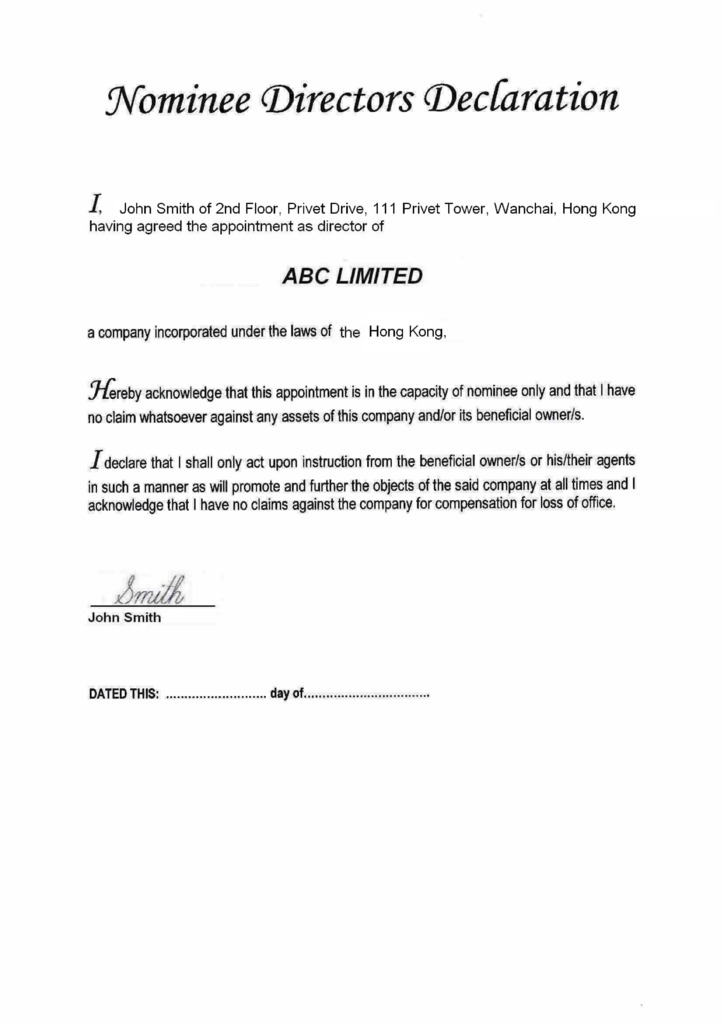

Paid-up “nominee director” set includes the following documents

Price480 USD

Paid-up “nominee shareholder” set includes the following documents

Price380 USD

Price350 USD

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD