Iceland has a civil law legal system and thus Icelandic law is characterized by written law.

Major sources of law in Iceland include the Constitution, statutory legislation, and regulatory statutes. Other legal resources are precedent and customary law.

The principal forms of business organization in Iceland are:

The most common structure is the Private Limited Company.

There is a range of requirements to the company name in Iceland:

The following steps are required to incorporate a private limited company in Iceland:

1. Search for company name online: The company name database can be accessed at the Internal Revenue Web site.

2. Deposit initial capital in bank account: The initial capital can be deposited in any commercial bank.

3. Apply for registration with Register of Limited Companies (Director of Internal Revenue): To apply for registration with the Register of Limited Companies, the company must provide five documents:

The register is also in charge of advertising the incorporation notice in the Official Gazette, the official journal. The total registration fee is ISK 130 500, which includes the company identification number (ISK 5 000), and the fee for publishing the notification in the Official Gazette (ISK 1 000 including VAT). Model incorporation documents and forms (in Icelandic) can be found on the Ministry of Industry and Innovation. The notification of incorporation form can be downloaded at no cost from the Internal Revenue Office Web site Signed documents can be sent via email to the Register of Limited Companies (Director of Internal Revenue).

4. Obtain VAT number from Director of Taxes: Companies that plan to sell goods or services valued at more than ISK 1 000 000 a year are required to collect and report VAT.

5. Notify tax authorities of employment of workers: The notification can be filed through http://www.skattur.is with a web key.

Upon the receipt of the required documents the formation of a new company in Iceland takes 5-7 days.

Special permission is required for banking, insurance, and financial services.

Non-residents may invest in business enterprises in Iceland with some limitations, which are stipulated in the Act no. 34/1991 on Investment by Non-Residents in Business Enterprise or in specific legislation, and upon the fulfillment of other conditions and acquisition of licenses required by law. Under the European Economic Area Agreement, investment in Iceland by EEA residents is in principle unrestricted, but few exceptions were negotiated in specific fields considered to be of national political importance.

Non-Residents (including EEA Residents) cannot conduct fishing operations within the Icelandic fisheries jurisdiction or own or run enterprises engaged in fish processing. Besides, only Icelandic citizens and other Icelandic entities, as well as individuals and legal entities domiciled in another member state of the European Economic Area, are permitted to own energy exploitation rights relating to waterfalls and geothermal energy for other than domestic use. The same applies to enterprises, which produce or distribute energy.

An Icelandic company must have a registered office in Iceland.

Register of shares must be kept at the registered office at all times.

Company seal is not required.

The redomiciliation of companies to or from Iceland is not permitted.

The dissolution of a private limited liability company is prescribed in detail in the relevant Acts. Shareholders controlling a minimum of two-third of a company's total share capital can take a decision at a shareholders' meeting to the effect that the company shall be dissolved. The private dissolution requires the appointment of a special winding up committee, which publishes a call to creditors in the Legal Gazette.

Special rules apply for the dissolution of financial undertakings as defined in the Act respecting Financial Undertakings No 161/2002.

The Board of Directors of a Private Limited Company in Iceland shall consist of at least three persons, unless there be four or fewer shareholders, then it is sufficient that the Board consist of one or two persons.

Directors should be natural persons.

At least half of the Directors shall be resident in Iceland. In case of one Director the condition of residence applies to him and it also applies to one out of two Directors. The Minister or he to whom he conveys his power may grant an exemption from the condition. Condition of residence does, however, not apply to the citizens of the States being parties to the Agreement on the European Economic Area, provided that the citizens concerned be resident in an EEA State.

The Board of Directors should be elected by a shareholders’ meeting.

It is possible to hold Board of Directors' meetings with the assistance of electronic media as far as this is in conformity with the implementation of the tasks of the Company's Board of Directors.

Icelandic private limited company is not required to have a company secretary.

Each Icelandic company should have at least one shareholder. A single party may establish a private limited company and be a shareholder. In such instances a single principal may constitute the board of directors and then there is no need for holding board or shareholder meetings as is else the case. At least one of the founders must reside in Iceland or be both a citizen and resident of an EEA or OECD country.

The identity of the founder or founders of a private limited company; the identity of shareholders that own more than 10% of total shares in a private limited company; and if all the shares in a private limited company are transferred to a single shareholder, the identity of that shareholder must be disclosed to the Registry.

An Annual General Meeting shall be held as Company Articles of Association determine, but yet no less than once a year and never later than eight months as of the end of each fiscal year. Annual accounts and Auditors´ or Inspectors´ report shall be submitted at an Annual General Meeting.

A shareholders´ meeting shall be held at a Company´s domicile, unless Company Articles of Association stipulate that a meeting shall or may be held at another place. It is permissible to hold a shareholders´ meeting elsewhere if that is necessary due to specific reasons.

A shareholders´ meeting may decide that a shareholders´ meeting will be held electronically only.

Although many jurisdictions are discussing the creation of an open registry of beneficiaries, Iceland does not yet have one. This means that beneficiaries’ details do not appear on a public profile. Generally, service providers including firm specializing in company formation, trust managers, lawyers, and accountants, keep beneficiaries’ information in strict confidentiality. It can only be disclosed to regulatory authorities (e.g. during examinations for its existence) or in compliance with a court order.

Share capital of an Icelandic company should be denominated in Icelandic kronas. A private limited company must have an initial capital of ISK 500 000, which has to be paid before registration. In case of failing to pay the capital, the company will not be registered.

Standard amount of the share capital is ISK 500 000.

Private limited company may issue share certificates. Each company should keep at its registered office a register of shares and all shareholders and the authorities should have access thereto and may acquaint themselves with the contents thereof.

Bearer shares and shares with no par value are not allowed.

Price6 000 USD

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and Registrar of Enterprises incorporation fee

Price2 000 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 700 USD

Paid-up “nominee director” set includes the following documents

Paid-up “nominee shareholder” set includes the following documents

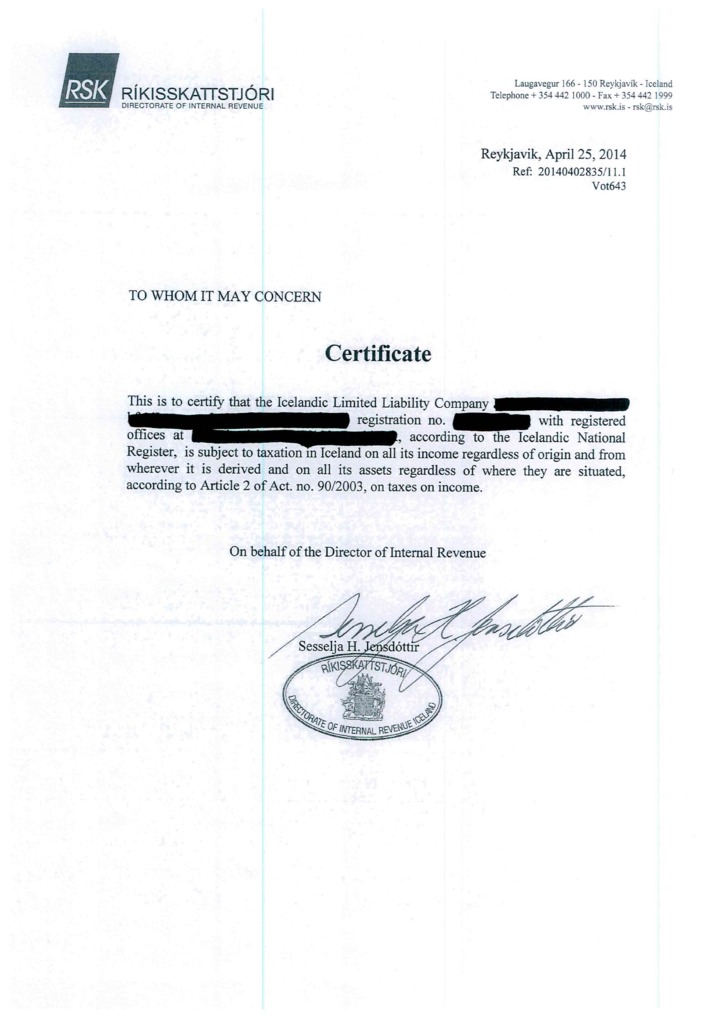

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD