There are two types of Partnership in Italy:

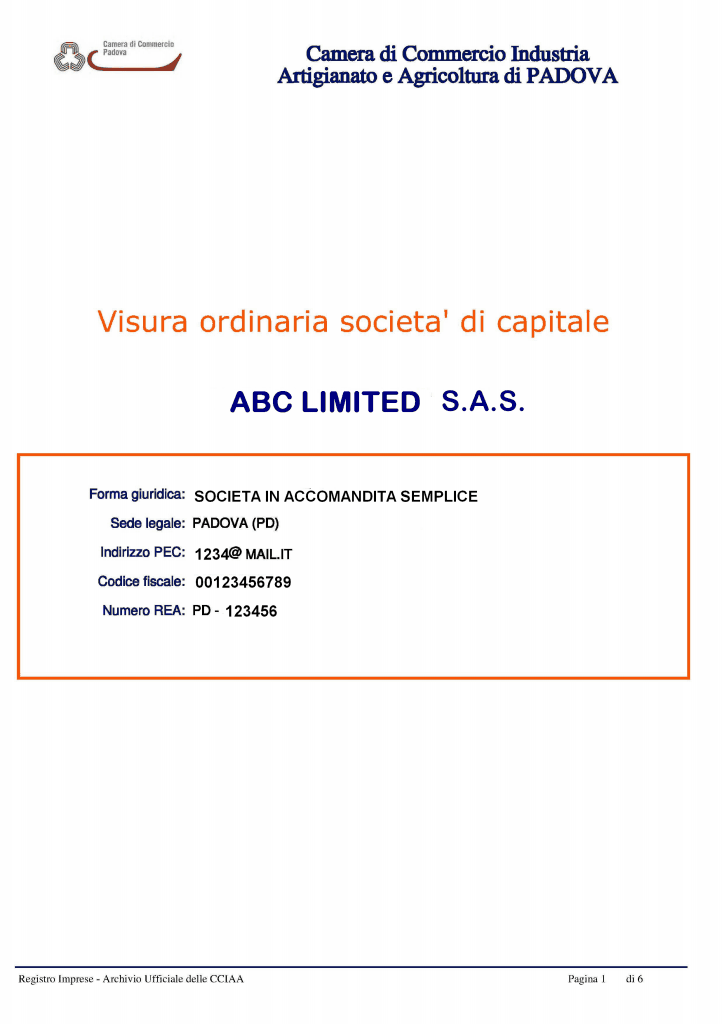

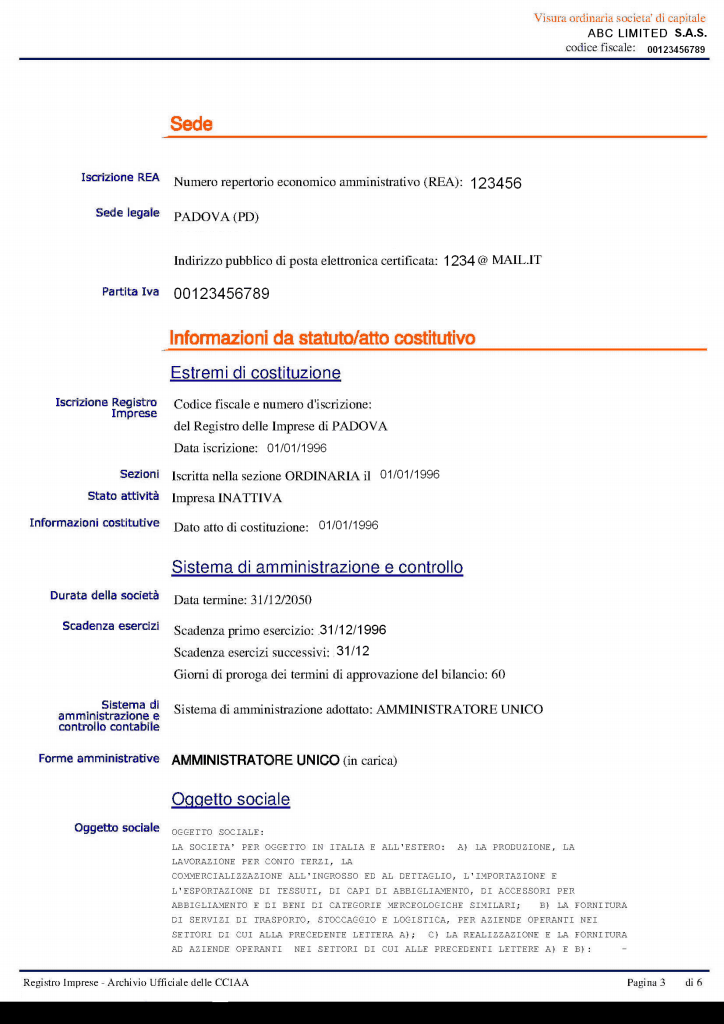

S.A.S. - Societa in accomandita semplice is the Limited Partnership in Italy.

The distinguishing features of S.A.S. in Italy:

minimum number of partners – two;

there is no limiting restriction to number of partners established by law;

at least one partner should be General Partner and at least one Partner with a limited liability;

there is no minimum share capital established by law;

there are no residency requirements to Partners;

there are no requirements to obligatory audit procedure;

it is enough to have a “virtual office”;

the participations may be transferred only by means of the consent of all the other partners.

Points 2 and 3 make S.A.S. profitable at the moment for people who invest in properties in Italy for several reasons:

The cost for incorporation of the company (S.A.S.) in Italy, including the corporate legal service for the second year

Price7 650 EUR

including Annual Duties for Chamber of Commerce for first year, NOT including Compliance fee

Priceincluded

Price1 210 EUR

including registered address and registered agent, NOT including Compliance fee

Pricefrom 1 200 EUR

(depends on the volume)

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR