Turkey has a civil law system, which has been wholly integrated with the continental European system. For instance, the Turkish civil law system has been modified by incorporating elements mainly of the Swiss Civil Code, the Code of Obligations and the German Commercial Code. The administrative law bears similarities with the French Counterpart and the penal code with the Italian Counterpart.

The principal forms of business organization in Turkey are:

The most common structure is the Limited Liability Company.

Every LLC in Turkey must have a name. The requirements for the company name are as follows:

The company name must be distinct from the names of all other companies.

It shall contain a company type as a suffix.

In case the trade name contains the name and last name of an individual, the phrasing that indicates the company type cannot be abbreviated or displayed in symbols.

It shall contain wording to indicate the business activity of the company.

The company name cannot contain the words such as Turkey or Turkish (only allowed with special permission).

The presence of foreign words in the trade name of a company is permitted unless such words do not contradict the law, national and the cultural and historical heritage of Turkey and where the name or brand promoting the goods or services constituting the business activity is in a foreign language or the investment is made by foreign shareholders.

To incorporate a Turkish company, the following steps are required:

1. Check the company name (see above for company name requirements).

2. Enter Turkey.

3. Get a Turkish identification number - TIN. TIN also can be received remotely - after visiting Turkey.

4. Put at least 25% of the initial capital in a bank and get the appropriate confirmation.

According to Articles 585 and 344 of the new Turkish Commercial Code, 25% of the share capital must be paid in prior to the new company registration. The remaining 75% of the subscribed share capital must be paid within 2 years.

Alternatively, the capital can be fully paid prior to registration.

Payment can be made from the founder's account or in cash directly to the bank.

5. Translate and notarize the company documents (the list of necessary documents varies, so you should check it with the consultant).

Company registration documents are exempt from stamp duty - no fee is charged on the Memorandum of Association and Signature Declarations. However, there are fees for notary services and securities.

6. Issue a power of attorney to a representative for registration actions.

7. Sign the company office lease agreement.

8. Apply for registration at the Trade Register.

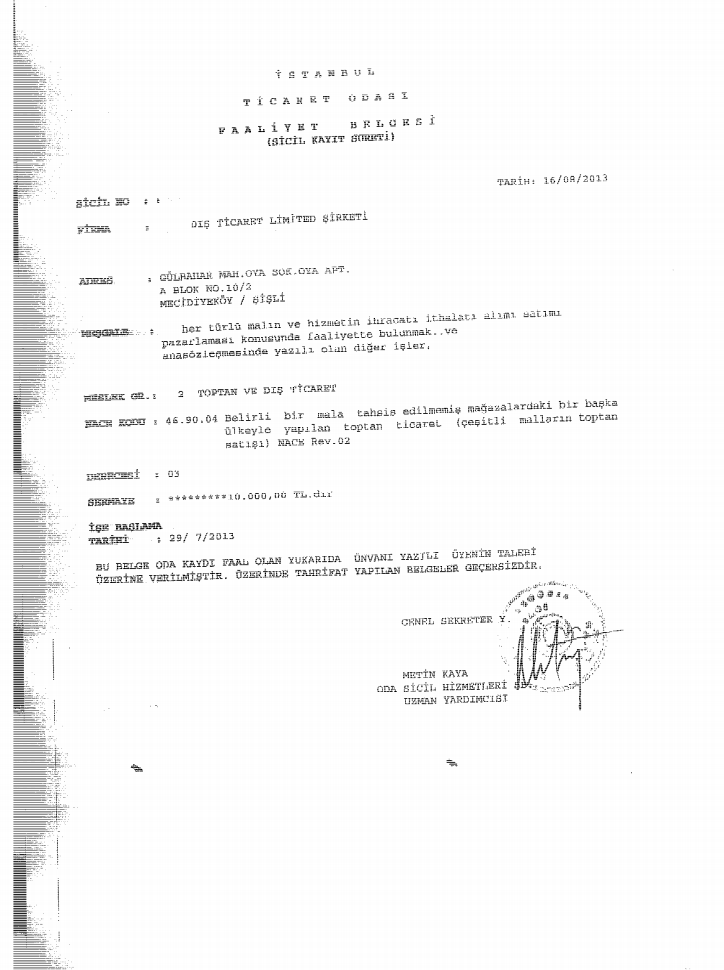

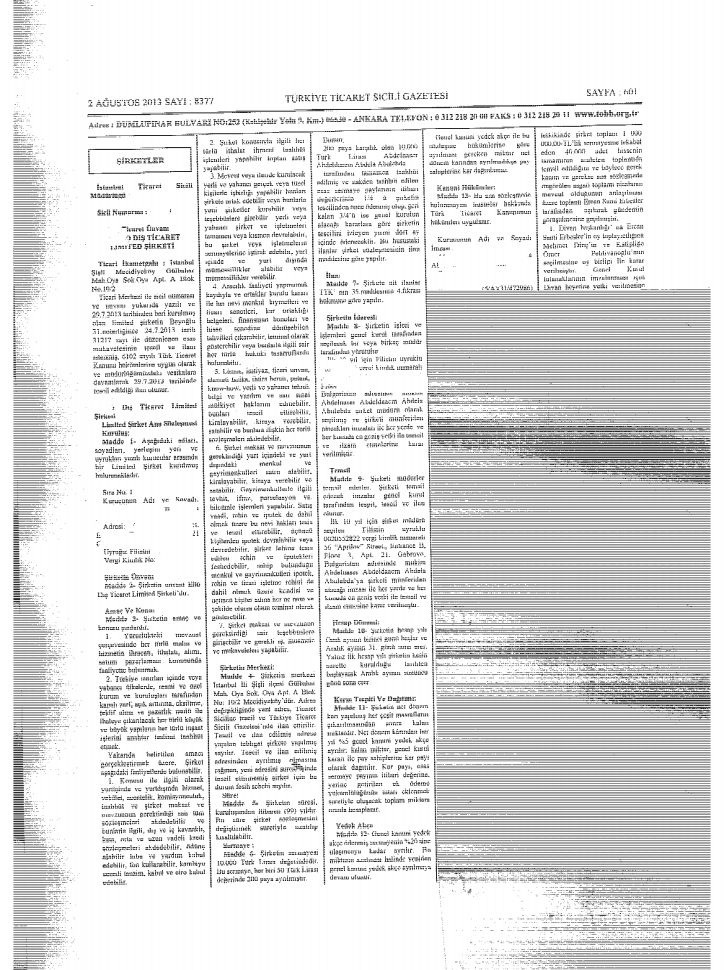

Following the completion of the registration phase before the Commercial Registry, the Commercial Registry notifies the relevant tax office and the Social Security Administration ex-officio regarding the incorporation of the company. The Commercial Registry arranges for an announcement in the Commercial Registry Gazette within approximately 10 days as of the company registration.

A tax registration certificate must be obtained from the local tax office soon after the Commercial Registry Office notifies the local tax office.

A social security number for the company must be obtained from the relevant Social Security Administration.

9. Sign a contract with a power of attorney for book-keeping of the company.

The procedure for incorporation takes less than 3-4 weeks.

After receiving the company registration documents, you can start the procedure of opening an account in a Turkish bank. This requires a personal visit to the bank by the director of the company.

The company can be active in any business even if it is not stated at its Articles of Association. Unless active in regulated areas where licensing is required (such as banking, telecommunication, energy etc.) the company can carry out any commercial or industrial activity.

Every Turkish LLC must have a registered office within Turkey.

Although there is no legal requirement (use of company title above the signature is sufficient) rubber company stamps are always used to signify the company name to be placed under the representing signatures once the signature circular is issued. Stamps are not issued officially and can be prepared by stationary offices in return of TRL 10.

The redomiciliation of companies to or from Turkey is permitted.

A Turkish limited liability company must have at least one director. One of the founders of the company shall become a director at the same time.

The director can be either legal entity or individual

The first director is appointed by the founder.

There are no residency requirements.

Director of the company is responsible to the state for the debts of the company.

For director who is a foreign citizen, it is mandatory to have a local work visa. The company must employ at least 5 residents of Turkey (one foreigner) to apply for such a visa. If the company fails to comply with this obligation, penalties may be imposed on the company (up to compulsory removal of such company from the Commercial Register).

Corporate Secretary is not required.

A Turkish limited liability company should have at least one founder and not more than 50 in total.

The founder can be non-resident companies or foreigner individuals.

Foreign investors are permitted to own 100% of the company.

There are no residency requirements for the founders.

The liability of the founders is limited to the amount of capital. However, the shareholders (subject to capital contribution ratio) and the management are also liable for amounts owed by the company to government authorities with their own assets for taxes, duties and charges that cannot be collected from the Company (such as taxes, administrative fines and social security premiums).

Information about the founders is kept in the Commercial Registry in the public domain.

It is required to hold a founders general assembly meeting for closure of previous year's accounts once every year.

In Turkey beneficiaries’ details do appear on a public profile.

In August 2021 the Turkish Tax Authority introduced the obligation for legal entities registered in the country to file a declaration of ultimate beneficiaries (owners).

The new requirement for annual declaration of information on ultimate beneficial ownership is related to bringing the country's domestic legislation in line with international standards (OECD).

Corporate taxpayers and other organizations without legal status registered in Turkey as of August 1, 2021 are required to regularly submit information on their beneficiaries to the State Tax Administration.

The following information shall be filed:

The minimum capital requirement for LTD companies is TRL 10 000.

25% of capital shall be paid into the company accounts (temporary accounts to be established before Chamber of Commerce filing for incorporation) at commencement (which can be freely used for expenses of the company following establishment) and the remaining could be paid in to the company in 24 months.

If a company has decided to obtain work visas for foreign nationals, the authorized capital of such company must be not less than 100 000 TRY.

If the founder of the company applies for a visa (work permit), his share in the Authorized Capital of such company must be at least 20%, but not less than 40 000 TRY.

Shares with no par and bearer shares are not permitted.

Price6 900 USD

including payment of fees to the Trade Registry and registered agent service

PriceIncluded

Stamp Duty and Trade Registry incorporation fee

Price2 000 USD

including registered address and registered agent, NOT including Compliance fee

Price150 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 700 USD

Company’s tax residence certificate for access to double tax treaties network

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD