The names of all private limited companies in the UK must end in either ‘Limited’ or ‘Ltd’. However, if your company's registered office is stated as being situated in Wales (a "Welsh" company), its name may instead end with "cyfyngedig" or "cyf". The name cannot:

Below is the full list of words, which are disregarded when it is determined, whether the name is “same as” or not:

Before choosing a name you should use our WebCHeck service to ensure your chosen name is not the 'same as' an existing name on the index of company names. You should also check the Trade Marks Register of the UK Intellectual Property Office to ensure that the proposed name does not infringe an existing trade mark.

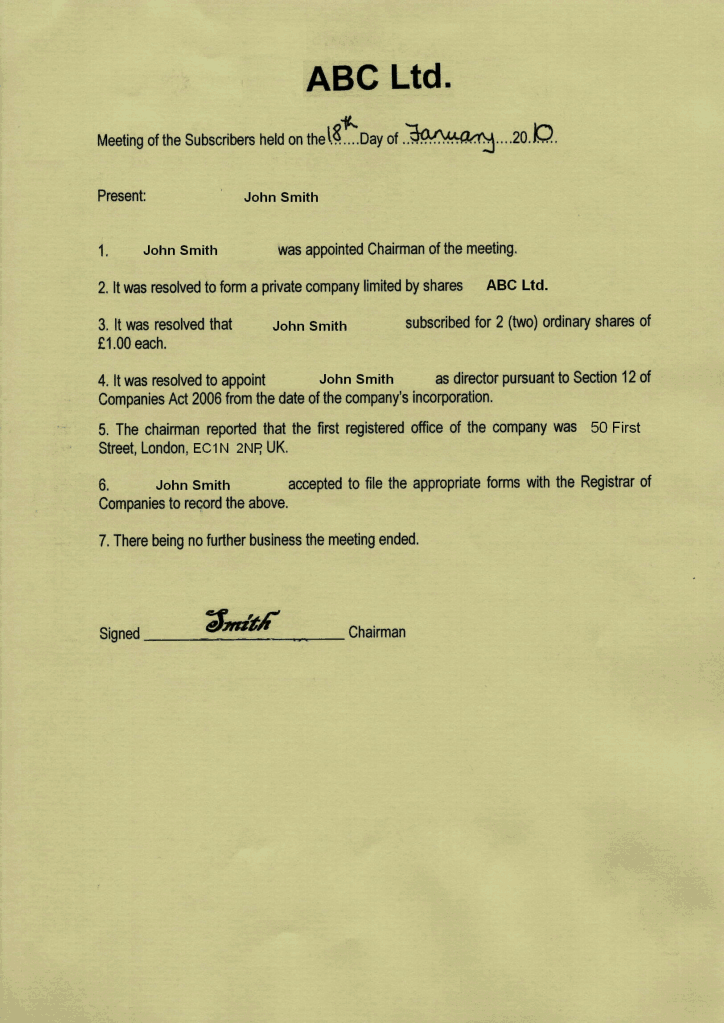

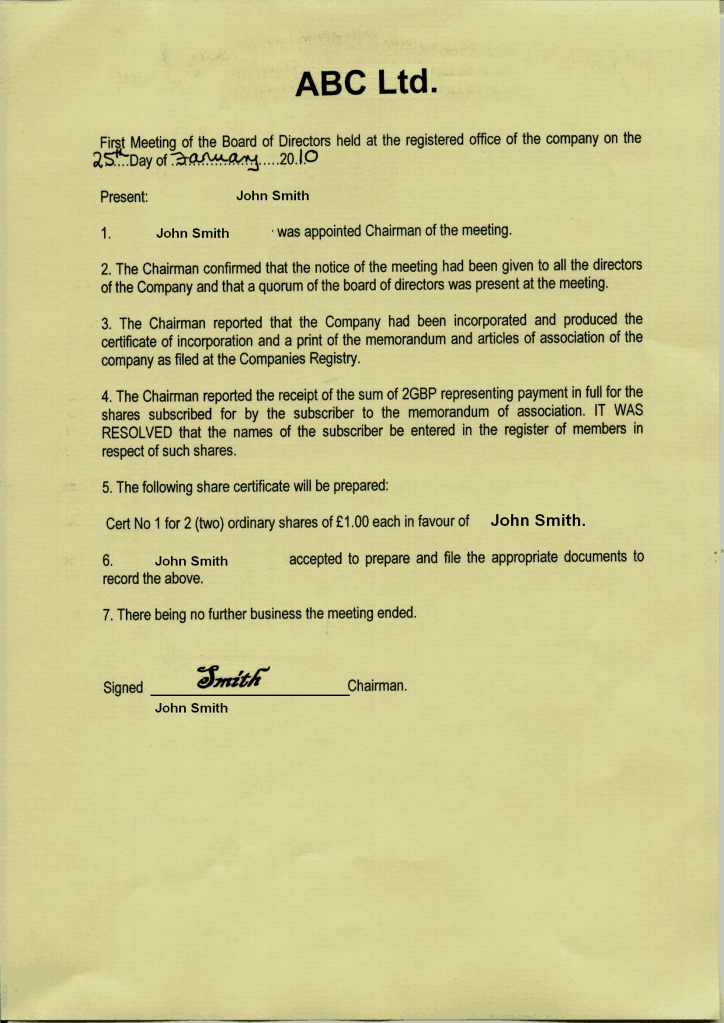

One or more persons can form a company for any lawful purpose by subscribing their names to a memorandum of association. In law, 'person' includes individuals, companies and other bodies. By completing the memorandum the subscribers are confirming their agreement to form a company.

There are three ways to incorporate a company:

Electronic Software Filing. Electronic incorporations can be submitted electronically through suitably enabled software. However, many incorporation agents and software providers have developed their systems to the point where they are able to offer customers a web-based electronic service (this is chargeable).

The standard fee for electronic filing is £13 (or £30 for the 'Same-Day' service for applications received by 3pm Monday to Friday). Straightforward applications are normally processed within 24 hours.

Web Incorporation Service. Web Incorporation is the safe and reliable way to file online, enabling you to quickly and easily incorporate your company. The standard fee for Web Incorporation is £15. There is no same day service and currently only applications for a private company limited by shares adopting model articles in their entirety with a proposed non sensitive name can use this service.

Paper Filing. Paper documents, which must be sent to the appropriate office, take longer to process than electronic documents. The standard registration fee is £40 (or £100 for the 'Same-Day' service for applications received by 3pm Monday to Friday).The fee is £20 (or £100 for the 'Same-Day' service) in the following circumstances:

Straightforward applications are normally processed within 5 days of receipt.

To incorporate your company you must file the following documents:

Application to register a company (form IN01) requires the following information:

The memorandum of association confirms the subscribers' intention to form a company and become members of that company on formation. In the case of a company that is to be limited by shares, the memorandum will also provide evidence of the members' agreement to take at least one share each in the company.

Under the Companies Act 2006, the memorandum is a much shorter document because all the constitutional rules of the company are contained in the articles of association. Consequently, the memorandum serves a more limited purpose and once the company has been incorporated, it cannot be amended.

Information on capital and shareholdings is no longer part of the memorandum as it is contained in the application to register (form IN01).

The required memorandum wording is included in the 'The Companies (Registration) Regulations 2008 (2008/3014)' and you should use this format when preparing your memorandum. You can also download a proforma memorandum from Companies House website. Please note, the wording of the memorandum is prescribed and it cannot be amended in any way. If you add or change the wording your application will not be accepted.

A company's articles of association are its internal rulebook, chosen by its members. Every company is required to have articles, which are legally binding on the company and all of its members. The articles help to ensure the company's business runs as smoothly and efficiently as possible and will set out how decisions are taken by the members and directors as well as various matters connected with the shares.

On incorporation your company can adopt model articles in entirety, model articles with amendments or it can draft its own bespoke articles.

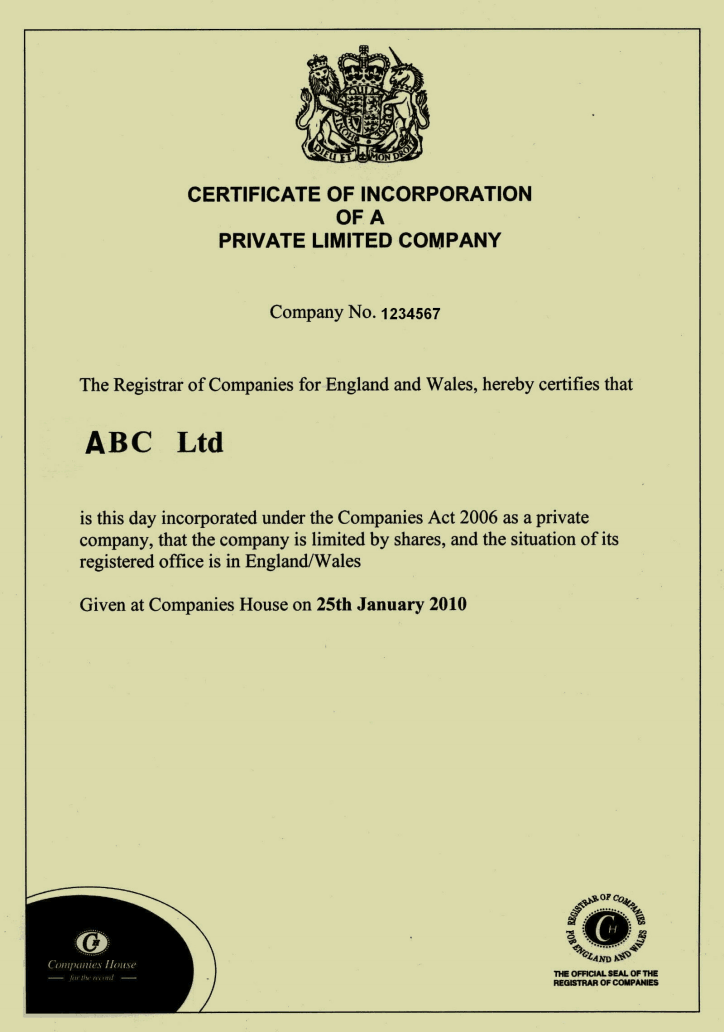

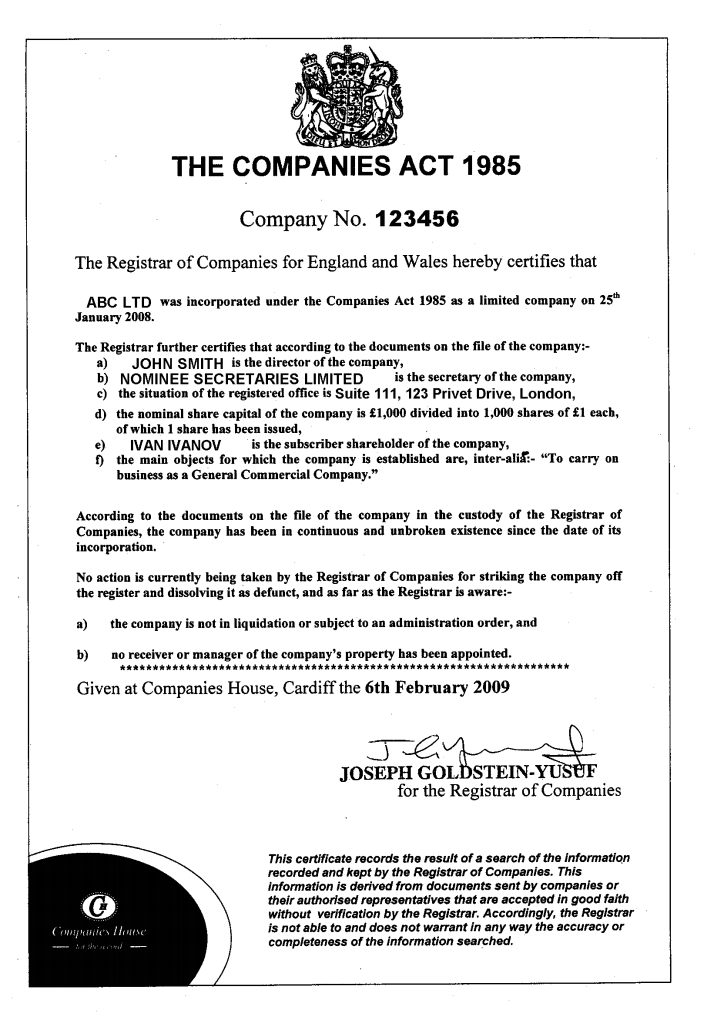

The certificate of incorporation is conclusive evidence that the requirements of the Companies Act 2006 as to registration have been complied with and that the company is duly registered under this Act. The certificate will state:

The certificate must be signed by the registrar or authenticated by the registrar's official seal.

After a new limited company is incorporated, Companies House tells HMRC when any limited company is formed and registered with them. HMRC uses the information they receive from Companies House to set up a computer record for your company and allocates it a reference number known as a Unique Taxpayer Reference (UTR). They then send form CT41G (Corporation Tax - Information for New Companies) to your company's registered office. This form includes your company's UTR.

You must tell HMRC that your company is active for Corporation Tax purposes within three months of starting business activity. The easiest way to tell HMRC that your limited company is active and has started its first accounting period is online.

You company may also need to register for other taxes such as PAYE as an employer and VAT.

Your company is an employer for its directors and staff. As an employer, you must deduct PAYE tax and National Insurance contributions (NICs) from your directors/employees' pay each pay period and pay employer's Class 1 NICs if they earn above a certain threshold.

You may need to register the company for VAT if the annual turnover is more than the VAT threshold and submit a VAT Return. You can also choose to register it for VAT voluntarily.

Every company must have a registered office. The registered office must be a physical location where notices, letters and reminders can be delivered to the company. The registered office does not need not be the place where the company carries on its day-to-day business so it could, for example, be your accountant's address. If the address is not effective for delivering documents, the company could risk being struck off the register or wound up by a creditor.

If any person you deal with in the course of your business requests in writing the address of your registered office, or the location where they can inspect your company records, or details of the records that you keep at your registered office, you must respond within five working days.

When you apply to incorporate your company you must state whether your company's registered office is to be situated in England and Wales, in Wales (a "Welsh" company), in Scotland or in Northern Ireland. The address of your registered office must also be in the same country as its situation.

If you decide to change your registered office address, you must file a 'Change of registered office address' form AD01. The change is not effective until Companies House registers the form, which can be filed electronically as well as on paper. You can change the address of your registered office but you cannot change its jurisdiction. For example, if your registered office is in Northern Ireland you cannot change it to an address in Scotland.

A company, depending on its company type, may have some or all of the following records:

- register of members

- register of directors

- directors' service contracts

- directors' indemnities

- register of secretaries

- records of resolutions and minutes of general meetings

- contracts or memoranda relating to purchase of own shares

- documents relating to redemption or purchase of own shares out of capital by a private company

- register of debenture holders

- instruments creating charges and a register of charges

You need to keep these company records available for inspection.

You may keep all or any of these records at the company's registered office. The company may choose an alternative location to make these records available for inspection. The company can only have one alternative location to the registered office at any given time.

That location must be in the same part of the UK as the registered office, e.g. a company registered in England and Wales can have an alternative inspection location in England and Wales, but not in Scotland or Northern Ireland. The company may choose to keep some records at its registered office and some at its alternative inspection location provided that all the records of a type are kept together.

If you do not keep all your records at the company's registered office, then you need to tell us the address of your alternative inspection location and which records you hold there, on Form AD02 and any change in that address, on Form AD03.You also need to tell us when you return any of the records to the registered office, on Form AD04.

A company may have a common seal, but need not have one.

A company which has a common seal shall have its name engraved in legible characters on the seal. If a company fails to comply with this requirement an offence is committed by the company, and every officer of the company who is in default.

The redomiciliation of companies to or from UK is not permitted.

The Companies Act 2006 requires a private company to have at least one director. However, a company's articles of association could impose a higher minimum requirement. At least one director must be an individual.

It is up to the members to appoint the directors who will run the company on their behalf. The only restrictions that prevent anyone becoming a director are:

Directors have a responsibility to prepare and deliver documents, on behalf of the company, to Companies House as and when required by the Companies Act. These include, in particular:

Private companies do not have to appoint a secretary unless their articles of association require them to, although they may choose to do so anyway.

The legislation does not set out the role of the company secretary; this is normally contained in their contract of employment. However, the company secretary might normally undertake the following:

The secretary is an officer of the company and may be criminally liable for defaults committed by the company.

UK private companies must have at least one shareholder. Shareholder can be a natural person or boy corporate, resident or non-resident.

Every company must keep a register of its members. There must be entered in the register —

In the case of a company having a share capital, there must be entered in the register, with the names and addresses of the members, a statement of—

There is now no statutory requirement for a private company to hold any general meetings, not even an Annual General Meeting. This change was introduced when Part 13 (sec281 - sec361) of the Companies Act 2006 came into effect on 1st. October 2007.

Some companies' articles will require them to hold an AGM and any such provision will continue to be binding on the company until the articles are amended. A company may hold an AGM even though not bound to by the Act or its articles.

At the end of 2016 Companies House and the Department for Business, Energy & Industrial Strategy published guidance explaining the procedure of keeping the Register of People with Significant Control (PSC) by companies and partnerships. The main document is called “Register of People with Significant Control. Guidance for Companies, Societates Europaeae and Limited Liability Partnerships”.

In accordance with the above, UK companies and LLPs must maintain PSC registers starting from 6 April 2017. The requirement applies to:

A person with significant control (PSC) of the company is an individual who meets (any) one or more of the following conditions:

- An individual who holds more than 25% of shares in the company

- An individual who holds more than 25% of voting rights in the company

- An individual who holds the right to appoint or remove the majority of the board of directors of the company

- An individual who has the right to exercise, or actually exercises, significant influence or control over the company

Where a trust or firm would satisfy one of the first four conditions if it were an individual. Any individual holding the right to exercise, or actually exercising, significant influence or control over the activities of that trust or firm.

Information to be entered on the PSC register:

This information must be confirmed by the PSC before entered into the register. Companies House keeps information about PSCs indefinitely.

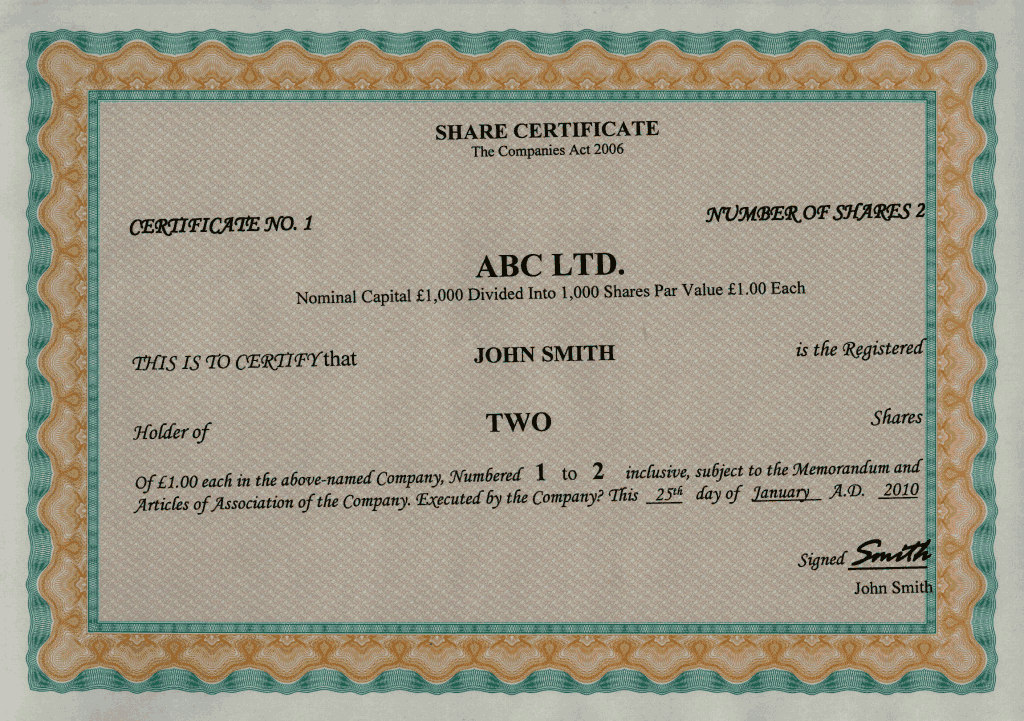

Minimum share capital for UK private companies is 1 share and there is no maximum share capital limit.

Companies incorporating with share capital must complete a statement of capital and initial shareholdings as part of the application to incorporate and as part of any annual return filing. The statement of capital must show the following details of the capital:

A company may have as many different types of shares as it wishes, all with different conditions attached to them. Typically, share types fall into the following categories:

Under the Companies Act 2006 any company limited by shares can (subject to prohibition or restriction in its articles) re-denominate its share capital, or any class of its share capital, into other currencies by passing a resolution.

A company may increase its share capital by allotting additional shares. A company cannot generally reduce its share capital otherwise than as permitted by statute and confirmed by the court. However, under the Companies Act 2006, a company can reduce its capital in the following circumstances:

- Reduction following redenomination

- Reduction supported by a solvency statement

- Reduction confirmed by a court order

In what circumstances may a company apply to be struck off the register?

A company may apply to the registrar to be struck off the register and dissolved. The company can do this if it is no longer needed. For example, the directors may wish to retire and there is no one to take over from them; or it is a subsidiary whose name is no longer needed; or it was set up to exploit an idea that turned out not to be feasible. Some companies who are dormant or non trading choose to apply for strike off. If you have decided that you no longer want to retain your company and wish to have it struck off, the registrar will not normally pursue any outstanding late filing penalties unless you restore the company to the register at a later stage.

This procedure is not an alternative to formal insolvency proceedings where these are appropriate. Even if the company is struck off and dissolved, creditors and others could apply for the company to be restored to the register.

When can I not apply to strike my company off the register?

An application for voluntary striking off can only be made by the company, and must be made on the company's behalf by its directors or a majority of them.

Sections 1004 and 1005 of the Companies Act 2006 set out the circumstances in which the company may not apply to be struck off. For example, the company may not make an application for voluntary strike off if, at any time in the last 3 months, it has:

A company cannot apply to be struck off if it is the subject, or proposed subject, of:

- any insolvency proceedings such as liquidation

- a section 895 scheme (that is a compromise or arrangement between a company and its creditors or members)

However, a company can apply for strike off if it has settled trading or business debts in the previous three months.

What should I do before applying?

There are safeguards for those who are likely to be affected by a company's dissolution. If your company has creditors, members etc, you should warn them, before applying, as any of them may object to the company being struck off. You should deal with any loose ends, such as closing the company's bank account, the transfer of any domain names - before you apply.

You may notify any other organisation or party who may have an interest in the company's affairs, otherwise they might later object to the application. Examples include His Majesty's Revenue and Customs, local authorities, training and enterprise councils and government agencies.

From the date of dissolution, any assets of a dissolved company will belong to the Crown. The company's bank account will be frozen and any credit balance in the account will pass to the Crown.

How do I apply?

You must complete a 'Striking off application by a company, Form DS01'.

The form must be signed and dated by:

- the sole director, if there is only one

- by both, if there are two

- by all, or the majority of directors, if there are more than 2

It will help Companies House if you provide the name, address, and telephone number of the person we should contact if we have any queries about the application. Please note, this information will appear on the company's public record when we register the form. Depending on where the company was registered you should then send the completed form, with the £10 fee, to Companies House, Cardiff, Edinburgh or Belfast. Cheques should not be payable from the account of the company applying for strike-off.

Who must I inform?

The directors who make the application must, within 7 days of sending the application to the registrar, send a copy to the following persons:

The company's directors must also send a copy of the application to any person who, after the application has been made, becomes a director, member, creditor or employee of the company, or a manager or trustee of any employee pension fund of the company. This must be done within 7 days of the person becoming one of these. They must also send a copy of the application to any person who becomes one of the above at any time after the day the company made the application for voluntary strike off. This obligation continues until the dissolution of the company or the withdrawal of the application.

What happens when Companies House receives the application?

Companies House will examine the form and if it is acceptable it will register the information and put it on the company's public record. Companies House will send an acknowledgement to the address shown on the form and will also notify the company at its registered office address to enable it to object if the application is bogus.

The registrar will publish notice of the proposed striking off in the Gazette to allow interested parties the opportunity to object.

A copy of this notice will be placed on the company's public record. If there is no reason to delay the registrar will strike the company off the register not less than 3 months after the date of the notice. The company will be dissolved on publication of a further notice stating this in the relevant Gazette.

What is the Gazette?

The Gazette is the official newspaper record in the United Kingdom. There are 3 of them: the London Gazette, for companies incorporated in England and Wales; the Edinburgh Gazette, for companies incorporated in Scotland; and the Belfast Gazette, for companies incorporated in Northern Ireland.

When the registrar publishes a notice to strike off or restore a company, the notice will appear in the Gazette for the part of the United Kingdom in which the company was formed. The gazettes are published weekly.

What if the company ceases to be eligible for striking-off or I change my mind and want to withdraw my application?

The directors must ensure the application is withdrawn immediately by completing the 'Withdrawal of striking off application by a company', Form DS02 if they change their mind or the company ceases to be eligible for striking-off. This may be because, after applying to be struck off, the company:

Any director may file the application to withdraw the strike off action to the registrar using our WebFiling service. Alternatively, the application can be withdrawn by submitting a paper Form DS02.

Can anyone object to dissolution?

Any interested party can object to the registrar.

Objections or complaints must be in writing and sent to the registrar with any supporting evidence, such as copies of invoices that may prove the company is trading. Reasons could include:

Offences and penalties

It is an offence:

- to apply when the company is ineligible for striking-off;

- to provide false or misleading information in, or in support of, an application;

- not to copy the application to all relevant parties within seven days;

- not to withdraw application if the company becomes ineligible.

The offences attract a fine of up to a maximum of £5,000 on summary conviction (before a magistrates' court or Sheriff Court) or an unlimited fine on indictment (before a jury). If the directors breach the requirements to give a copy of the application to relevant parties and do so with the intention of concealing the application, they are also potentially liable to not only a fine but also up to seven years imprisonment. Anyone convicted of these offences may also be disqualified from being a director for up to 15 years.

Can the registrar strike a company off the register on his own initiative?

Yes, if it is neither carrying on business nor in operation. The registrar may take this view if, for example:

Before striking a company off the register, the registrar is required to write two formal letters and send notice to the company's registered office to inquire whether it is still carrying on business or in operation. If he is satisfied that it is not, he will publish a notice in the relevant Gazette stating his intention to strike the company off the register unless he is shown reason not to do so.

A copy of the notice will be placed on the company's public record. If the registrar sees no reason to do otherwise, he will strike off the company not less than three months after the date of the notice. The company will be dissolved on publication of a further notice stating this in the relevant Gazette.

How can I avoid this action?

If you want your company to remain on the register, you must reply promptly to any formal inquiry letter from the registrar and deliver any outstanding documents. Failure to deliver the necessary documents may also result in the directors being prosecuted.

Can I object?

The registrar will take into account representations from the company and other interested parties, for example, creditors. If there is good reason not to strike the company off the register, he may suspend the action until the objection is resolved.

What happens to the assets of a dissolved company?

From the date of dissolution, any assets of a dissolved company will be 'bona vacantia'. Bona vacantia literally means “vacant goods” and is the technical name for property that passes to the Crown because it does not have a legal owner. The company's bank account will be frozen and any credit balance in the account will be passed to the Crown.

The registrar can only restore a company if he receives a court order, unless a company is administratively restored to the register. Anyone who intends to make an application to the court to restore a company is advised to obtain independent legal advice.

Any company which is restored to the register is deemed to have continued in existence as if it had not been struck off and dissolved.

Who can apply to the Court to restore a company to the register?

Generally, any of the following may make an application for restoration:

How long have I got to make an application to the Court?

For companies dissolved under Section 1000 or 1003 of the CA2006 and 652 or 652a of the 1985 Act.

As a general rule restoration by court order can be applied for up to six years from the date of dissolution, if the dissolution date is on or after 1st October 2009. If the dissolution date is on or before 30th September 2009, transitional arrangements exist to take account of the new 2006 Companies Act for restoration.

For companies dissolved under Section 201 and 205 and Para 84 of Schedule B1 of the Insolvency Act and 652 of 1985 Act or Section 1001 of the CA2006.

Companies dissolved on or before 30th September 2007 following any form of liquidation are out of time to restore the company.

Companies dissolved on or after 1st October 2007 following any form of liquidation have six years from the date of dissolution.

Why might a company be restored with a different company name?

The registrar will normally restore a company with the name it had before it was struck off and dissolved. However, if at the date of restoration the company's former name is the same as another name on the registrar's index of company names, he cannot restore the company with its former name. You can check whether the company's name is the same as another on the register by using the WebCheck service.

If the name is no longer available, the court order may state another name by which the company is to be restored. On restoration, the registrar will issue a change of name certificate as if the company had changed its name.

Alternatively, the company may be restored to the register as if its registered company number is also its name. The company then has 14 days from the date of restoration to pass a resolution to change the name of the company. You must deliver a copy of the resolution and a 'notice of change of name by resolution of directors' (Form NM05) to Companies House with the appropriate fee. The registrar will then issue a change of name certificate.

!It is an offence if the company does not change its name within 14 days of being restored with the number as its name!

Are there costs or penalties?

Yes. Where property has become bona vacantia, the Court may direct that the claimant meets costs of the Crown representative in dealing with the property during the period of dissolution or in connection with the proceedings. The Court may also direct that the claimant meets the registrar's costs in connection with the proceedings for the restoration.

The company must normally pay any statutory penalties for late filing of accounts delivered to the registrar outside the period allowed for filing. The penalties that may be due are:

The level of any late filing penalty depends on how late the accounts are when the registrar receives them. For example, a set of accounts that you should have delivered 2 months before a private company was dissolved are normally regarded as 2 months late if you deliver them on restoration and you must pay the relevant penalty. The company is not liable for late filing penalties for accounts received on restoration but which became due while the company was dissolved.

What happens when the court makes an order for restoration?

The applicant must deliver a copy of the court order to the registrar to restore the company. A company is restored when you deliver the order. When restoring a company that was registered in Scotland, the registrar in Scotland will require a copy of the order certified by the court.

What happens when the company has been restored?

When it has been restored, the general effect is that a company is deemed to have continued in existence as if it had not been dissolved or struck off the register. The Court may give directions or make provision to put the company and all other persons in the same position as they were before the company was dissolved and struck off. A notice will also be placed in the relevant Gazette.

Under certain conditions, where a company was dissolved because it appeared to be no longer carrying on business or in operation, a former director or member may apply to the registrar to have the company restored. This is called 'administrative restoration'. If the registrar restores the company it is deemed to have continued in existence as if it had not been dissolved and struck off the register.

Who can apply to have a company restored to the register?

Only a former director or former member of the company, who was a director or member at the time the company was dissolved can apply.

Can an application for administrative restoration by made in respect of any company?

No. To be eligible for administrative restoration, the company must have been:

If a company meets the above criteria, an application for restoration may be made if it meets the following conditions:

How do I apply for administrative restoration?

You must send an 'Application for administrative restoration' (Form RT01) to the registrar which includes a statement of compliance confirming that the applicant is legally entitled to make the application and that the conditions for restoration are met.

The registrar's fee for processing the application is £100.

What are the other costs or penalties involved in making an application for administrative restoration?

The applicant must meet the Crown representative's costs or expenses (if demanded). The company must pay any statutory penalties for late filing of accounts delivered to the registrar outside the period allowed for filing.

You must also pay the appropriate filing fee on submission of any outstanding documents.

The level of any late filing penalty depends on how late the accounts are when we receive them. In the case of accounts delivered on restoration, the registrar will normally disregard the period during which the company was dissolved. For example, a set of accounts that you should have delivered 2 months before a private company was dissolved are normally regarded as 2 months late if you deliver them on restoration and you must pay the relevant penalty before the restoration of the company.

The company is not liable for late filing penalties for accounts received on restoration but which became due while the company was dissolved.

What happens next?

The registrar will give notice to the person who has applied for restoration of his decision.

If the registrar decides that he will restore the company to the register the restoration will take effect from the date he sends the notice. The notice will include the company's registered number and the name of the company. If the company is restored to the register under a different name or with the company number as its name, that name and its former name will appear on the notice.

If the registrar decides not to restore the company to the register, the applicant may apply to the Court for restoration within 28 days even if the period for restoration has expired.

Why would a company be restored with a different company name?

If at the date of restoration the company's former name is the same as another name on the registrar's index of company names, it will need to choose an alternative name. The application for restoration may state another name by which the company is to be restored. You can check whether the company's name is the same as another on the register by using the WebCheck service.

Alternatively, we may restore the company to the register as if its registered number is also its name. The company then has 14 days from the date of restoration in which to change the name of the company. Alternatively, the directors can pass a resolution to change the company name. You must deliver a copy of the resolution and notice (Form NM05) of the change of name to Companies House including the appropriate fee.

It is an offence if the company does not change its name within 14 days of the company being restored with the company number as its name.

What happens when the company has been restored?

When it has been restored, the general effect is that a company is deemed to have continued in existence as if it had not been dissolved or struck off the register. An application can be made to the Court for directions or provision required to put the company and all other persons in the same position as they were before the company was dissolved and struck off. Any such application to the Court must be made within 3 years of the company being restored.

Price2 000 USD

including preparation and submission of the originals of the company's constituent documents and an apostilled copy of such documents, documents formalizing the issue of shares, as well as the seal of the company, excluding compliance fee

PriceIncluded

Stamp Duty and Companies House incorporation fee

Price970 USD

including the provision of legal addresses, excluding compliance fee and reporting services

Price250 USD

DHL or TNT, at cost of a Courier Service

Price640 USD

Price640 USD

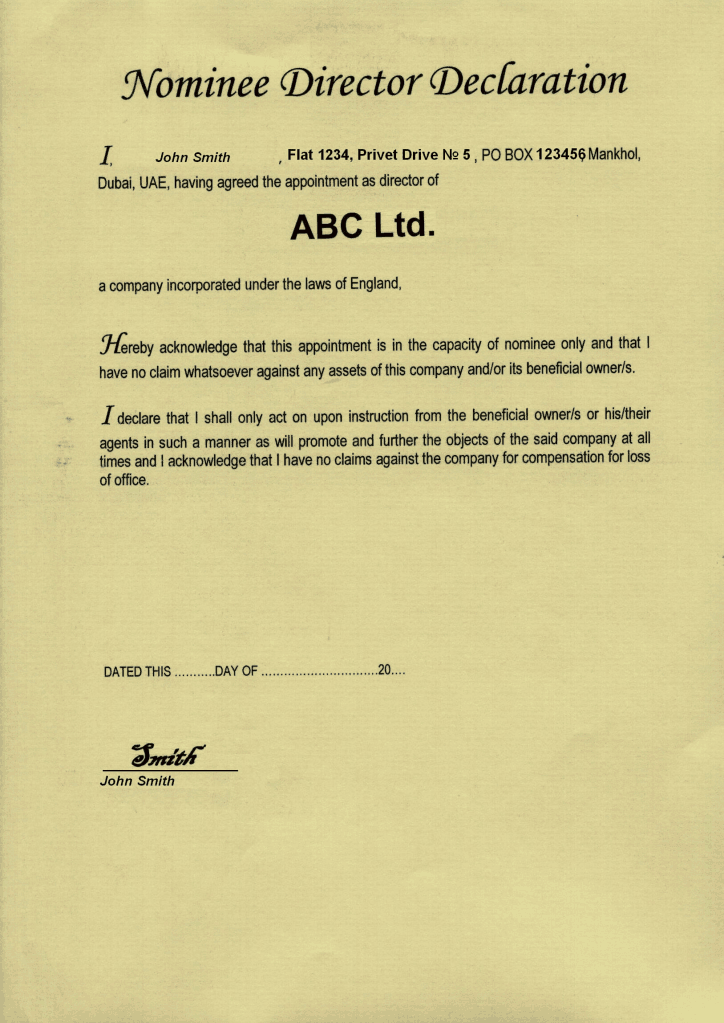

Paid-up “nominee director” set includes the following documents

Price480 USD

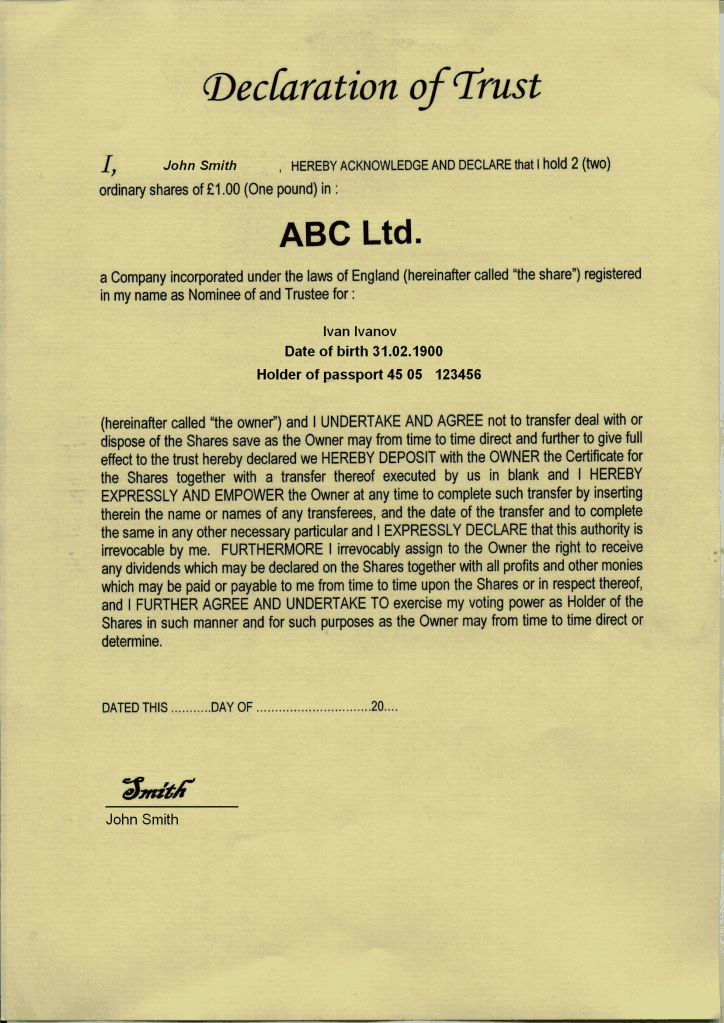

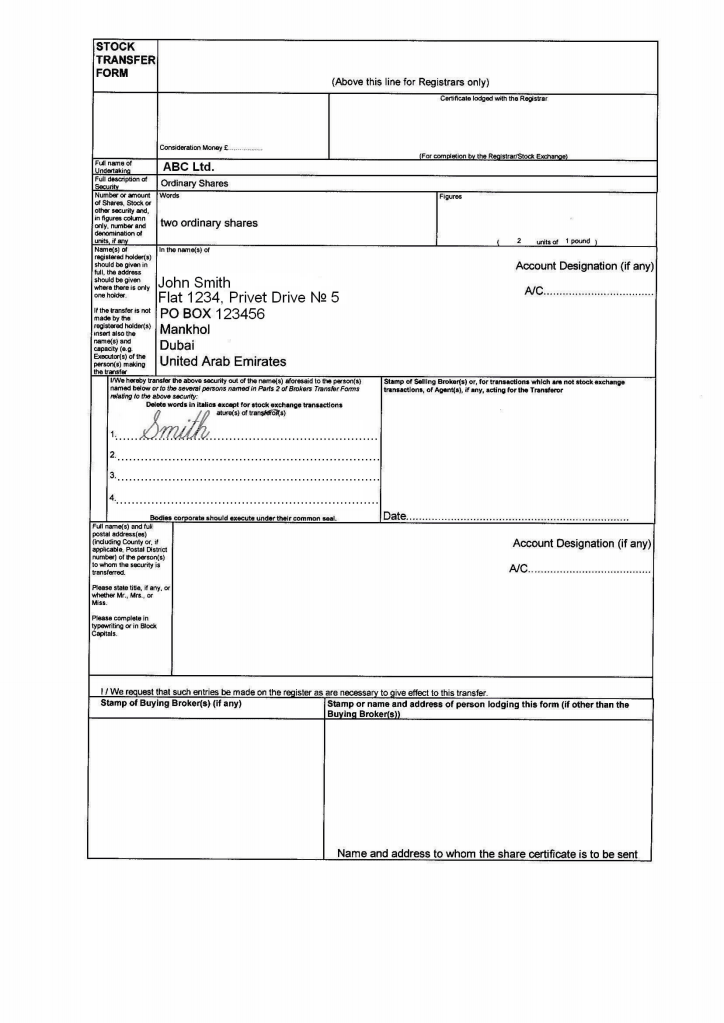

Paid-up “nominee shareholder” set includes the following documents

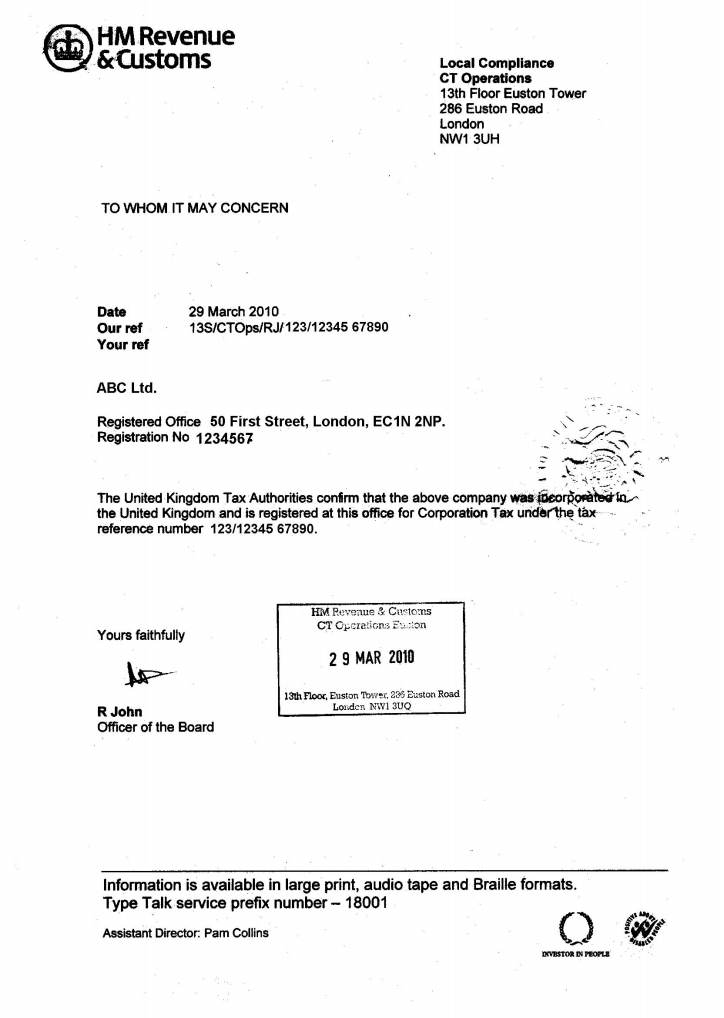

Company’s tax residence certificate for access to double tax treaties network

Price220 USD

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Price220 USD

Compliance fee is payable in the cases of: company incorporation, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD