India has a variety of forms of business organization, which include:

The main piece of legislation governing companies is the Companies Act 1956. The most common type of company is the Private Limited Company, which will be described in more detail below.

The incorporation of a company includes the following steps:

India has the following requirements for the company name:

2.1. for directors and shareholders:

a) proof of identity:

b) proof of address:

c) photos of directors (passport-like format – 3.5 x 4.5, against a white background);

d) CVs of directors.

If one of the founders is a legal entity, then a full set of constitutive documents is required, including a certificate of good standing (or its equivalent) for companies older than 1 year. The documents must also disclose the ownership structure up to the ultimate beneficial owner.

2.2. lease agreement for the future office.

It is next necessary to register with the local municipality for VAT, for profession tax and for import-export operations.

In accordance with the new requirements of Indian legislation.

India has two levels of taxation:

At the central level there are:

At the state level there are:

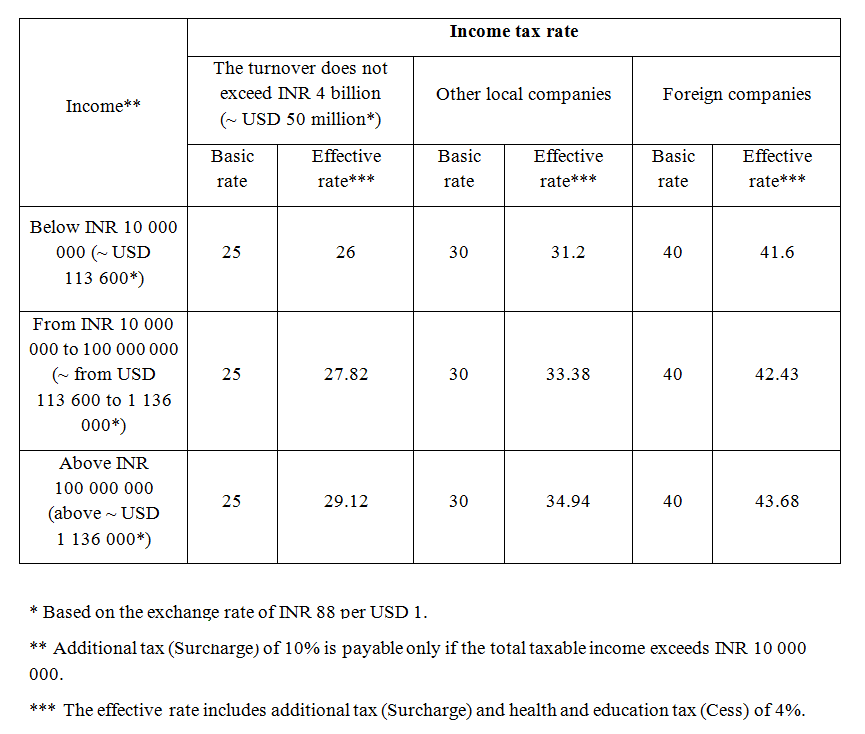

A resident company is taxed on its worldwide income, whereas a non-resident company is only taxed on income that is derived in India or that accrues or arises (is deemed to accrue or arise) in India.

Starting from 2019, local manufacturing companies incorporated on or after 1 October 2019 that commence operations before 31 March 2023 are eligible, subject to certain conditions, for a reduced income tax rate of 15% (plus 10% surcharge and 4% health and education cess).

Goods and services tax (GST) is an indirect tax that has been in force in India since 1 July 2017. It is levied on the production, sale and consumption of goods and services.

Since India is a federal republic, goods and services tax is levied at both the central (CGST) and state (SGST) levels.

The rate of goods and services tax varies depending on the type of goods and services and can be 0%, 5%, 12%, 18% or 28%.

All suppliers whose aggregate turnover in a financial year exceeds the established threshold are required to register for GST.

The GST registration threshold is INR 2 000 000 (~ USD 22 700) of aggregate turnover in a financial year (INR 1 000 000 (~ USD 11 360) for some special category states such as the north eastern states). For the purposes of the threshold, the aggregate turnover is calculated on all India basis. For certain specific categories of supplies and suppliers, the registration for GST is mandatory.

Small traders with a turnover below INR 10 000 000 (~ USD 113 600) have an option to use the composition scheme. Under this scheme, GST will be applied at a lower rate (1% of the taxable turnover for manufacturers/traders and 5% for restaurants). The composition scheme is not applicable to services other than restaurant services.

All Indian companies are required to prepare annual financial statements. The first financial statements of a new company must be made not more than 9 months before the Annual General Meeting (AGM). After that, the annual financial statements must be prepared not more than 6 months before the AGM.

Annual financial statements are required to be filed with the Registrar within 30 days of the date of AGM, or, if the meeting was not held, within 30 days of the date on which the AGM should have been held.

Financial statements must cover the financial year (12 months), but not more than 15 months. It is possible to apply to the Registrar for extension of the financial period to 18 months.

In the case of a limited company, its balance sheet is publicly available, but its profit and loss account is not.

In addition, every Indian company is required to prepare and file an Annual Return with the Registrar within 60 days of the date of AGM or the deadline for AGM, if such was not held.

|

Services

|

Fees (USD)

|

|

Total cost of incorporation

Includes: - preparation and provision of original constitutive documents - payment of government fees (except stamp duty on payment of share capital) - registration for tax (PAN, TAN, VAT) and at the RBI - assistance with opening a local bank account for depositing the share capital Does not include: - translation, notarization and apostille of documents - payment of share capital, - office lease - basic Compliance fee |

from 9 600

|

|

Subsequent annual maintenance (starting from the second year), including the registered agent services for a year, but not including Compliance fee

|

from 5 085

|

|

Renting a physical office is necessary for registration of a company in India.

Our fees for finding an office and preparing a lease agreement for a year – 825 |

|

Local director (for 1 year)

(services such as signing, visits to banks, etc. are to be paid for additionally and to be agreed with the director in advance) |

13 200

|

|

Local secretary (for 1 year)

(if necessary) |

8 250

|

|

Preparation and submission of non-dormant financial statements

|

100 – 400 / hour

(based on time spent) |

|

Shipment of documents

|

275

|

|

Compliance fee

Payable in the cases of: - incorporation of a company, - renewal of a company, - liquidation of a company, - transfer out of a company, - issue of a power of attorney to a new attorney, - change of director / shareholder / beneficial owner, except the change to a nominee director / shareholder, - signing of documents. |

385 (standard rate, includes the check of 1 individual)

+ 165 for each additional individual (director, shareholder, or beneficial owner) or legal entity (director or shareholder) if such legal entity is administered by GSL + 220 for each additional legal entity (director or shareholder) if such legal entity is not administered by GSL 495 (rate for high-risk companies, includes the check of 1 individual) 110 (signing of documents) |

*The digital signature is valid for two years, after which it is subject to renewal.

**The fees are valid as at September 2025.