Belgium law is a part of the civil law tradition of continental European legal systems.

The apex of the legal system is the Constitution of 1831, as well as five French codes, which are the basis of Belgian legislation since promulgation of independence in 1831 and were adopted in 1804-1910 when the territory was under the rule of Napoleon. They are the Civil Code, the Commercial Code, the Penal Code, the Civil Procedure Code, and the Criminal Procedure Code. The all underwent big changes. For example,

Companies Act was added to the Commercial Code as an independent part in 1935.

Under the legislation of Belgium, the following types of commercial entities may be established in Belgium to carry on business:

The most common form of business vehicles for foreign companies in Belgium wishing to carry on business is private limited liability company - SPRL/BVBA). The most important features of BVBA are liability of shareholders according to their capital contributions and limited transfer of shares.

To register an Belgiian company, the following steps are required:

Thanks to access to notarial system www.e-notariat.be, notaries are able to register articles of incorporation electronically with the Central Enterprise Databank (BCE/KBO), the commercial court and the Belgian Official Gazette (Moniteur belge/Belgisch Staatsblad) in a single operation.

The name of an associate, the corporate purpose or any other name can be chosen as a company name. It should also contain a legal name either in full – société privée à responsabilité limitée/besloten vennootschap met beperkte aansprakelijkheid, or in shortened form SPRL/BVBA.

In order to avoid confusion or unfair competition (so that one company is not mistaken for another), you must ensure that you choose a name which is not already used by another company or which would resemble another company’s name. Similarly, it is also important to verify that the name is not a registered trademark or is not already the name of an organization or association.

In general, a notary public will verify these aspects before the company’s incorporation. Among others, you can search for active registered companies via the Enterprise Crossroads Bank or check the section of the Belgian Official Gazette website which is reserved for commercial companies.

In Belgium additional licensing is required for trust, insurance and banking services. In the meantime BVBA are not allowed to distribute funds and carry on insurance activities. There are also some restrictions for foreign investors in such fields as post, energetics, broadcasting, public transport and telecommunications.

Belgian companies must maintain a registered office in Belgium. It should be a real address, not a PO Box.

Accounting books, minutes of Board meetings and Shareholders meetings should be kept at the registered office.

A new Belgian company developing activities can rent (lease), buy or build premises. Most small and medium sized businesses start by renting space according to their particular needs. Local authorities can assist in finding appropriate premises. For example, in Flanders it would be Flanders Investment & Trade, in co-operation with local development authorities and/or real estate advisers who will prepare an overview of potential locations in the different areas of Flanders, according to the specifications of the potential investor.

One of the typical features of a so-called commercial lease is that the lease is contracted for a nine-year period but can, under certain conditions, be terminated by either party after any three-year period, albeit it under specific conditions for the lessor.

Leases must be registered for tax purposes only and therefore must be in writing, stipulating the duties and obligations of the respective parties. Under Belgian Law, registering a lease also gives more protection to the tenant when the premises are sold by the landlord to a new owner during the execution of the lease.

Generally, a landlord will require a deposit which usually equals three to six months rent. This can be provided by a deposit in cash with a bank or by a bank guarantee. In the latter case, the bank will charge the tenant a small fee.

It is not required from Belgian companies to have a seal.

The redomiciliation of companies either to or from Belgium is not permitted.

A Belgian company is required to have a minimum of one director. Director should be properly qualified what should be confirmed by educational diploma or certificate on practical experience. Directors can be residents and non-residents, individuals and corporates. Directors are not bound to be shareholders.

Board of Directors can pass its powers to the managing director. Board meetings are held according to the procedure adopted in the Articles of Association.

Secretary is not required in Belgian companies.

Belgian companies may have at least one shareholder. Shareholders can be individuals and corporates, residents and non-residents. Nominee shareholders are permitted.

General Meetings are to be held annually according to the Articles of Association following the end of each accounting. Place of meeting should be at the registered office or at another place specified in the minutes of the meeting.

Information on the company shareholders is disclosed to the local agent and filed on public record.

Since 2018, Belgium has introduced a Registry of Beneficiaries, which includes information on the ultimate owners and beneficiaries of companies, foundations, non-profit organizations, trusts and other similar structures.

Companies are required to keep reliable, accurate and up-to-date information about their beneficiaries and submit it to the electronic registry within a month.

In November 2022, Belgium suspended public access to the register of beneficiaries pursuant to the Court of Justice of the EU (CJEE) decision in consolidated cases C-37/20 and C-601/20 of November 22. The Court ruled that Article 1, paragraph 15(c) of Directive (EU) 2018/843 of the European Parliament and of the Council of 30 May 2018, which provides for access to information on the beneficiaries of legal persons for any member of the public, was invalid as it constituted a serious interference with the fundamental rights to respect for privacy and to the protection of personal data enshrined in Articles 7 and 8 of the EU Charter of Fundamental Rights.

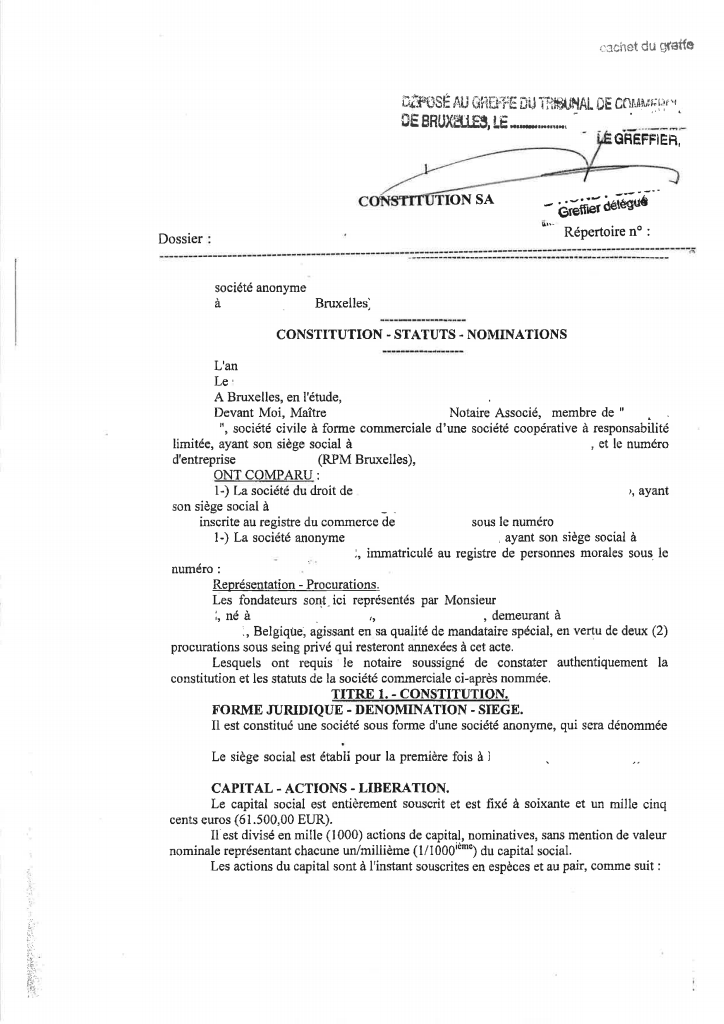

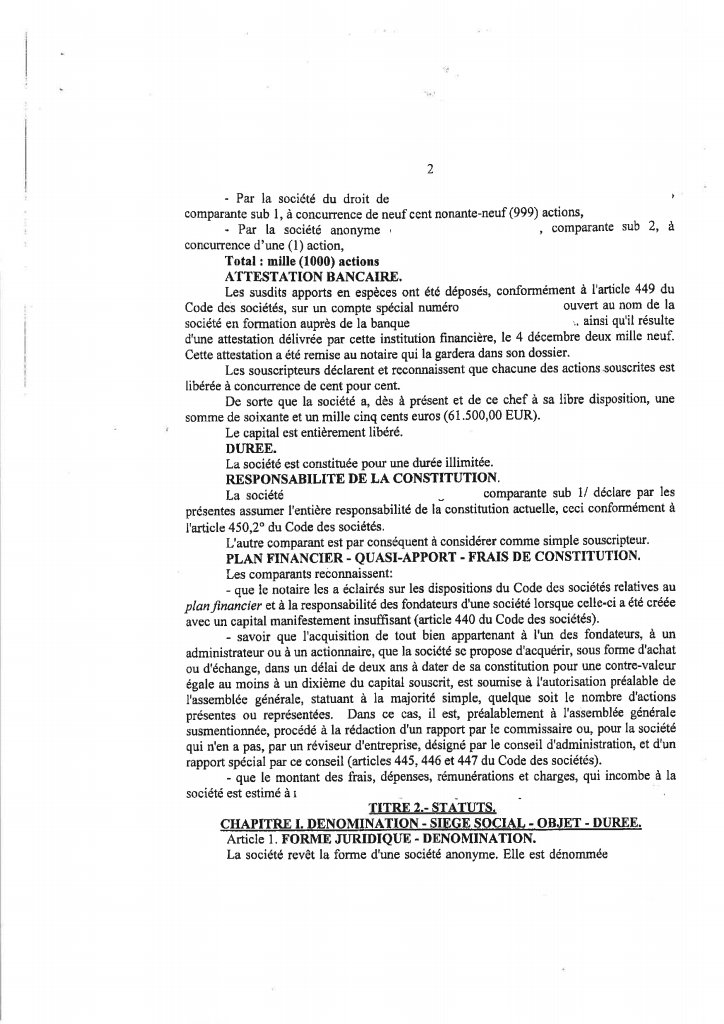

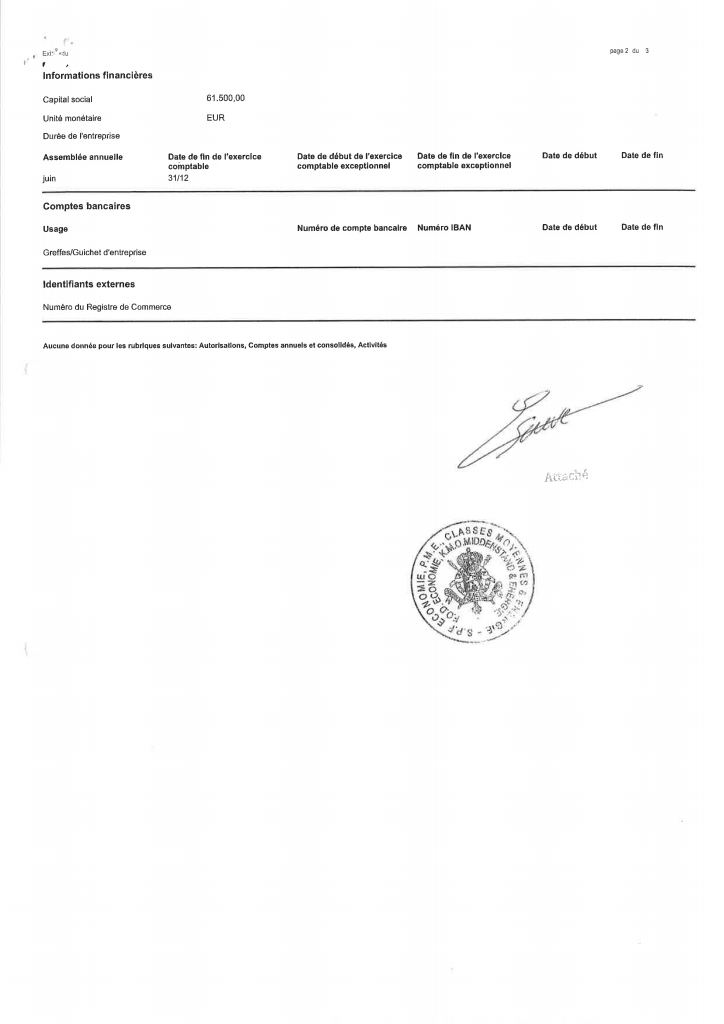

The capital must be fully subscribed at the time the company is incorporated, to the amount of €18,550.

Each share subscribed in cash must be at least one-fifth paid up. Shares corresponding to contributions in kind must be fully subscribed at the time of the incorporation. Of the total capital, a minimum of €6,200 must be paid up in the account of the SPRL/BVBA. If the company has only one founder a minimum of €12,400 needs to be paid-up.

All shares are nominative shares and have to be registered in a share register. Bearer shares cannot be subscribed. The transfer of shares takes the form of a declaration of transfer in the share register and is subject to certain transfer restrictions. The shares cannot be transferred unless the transfer is approved by a special majority of partners.

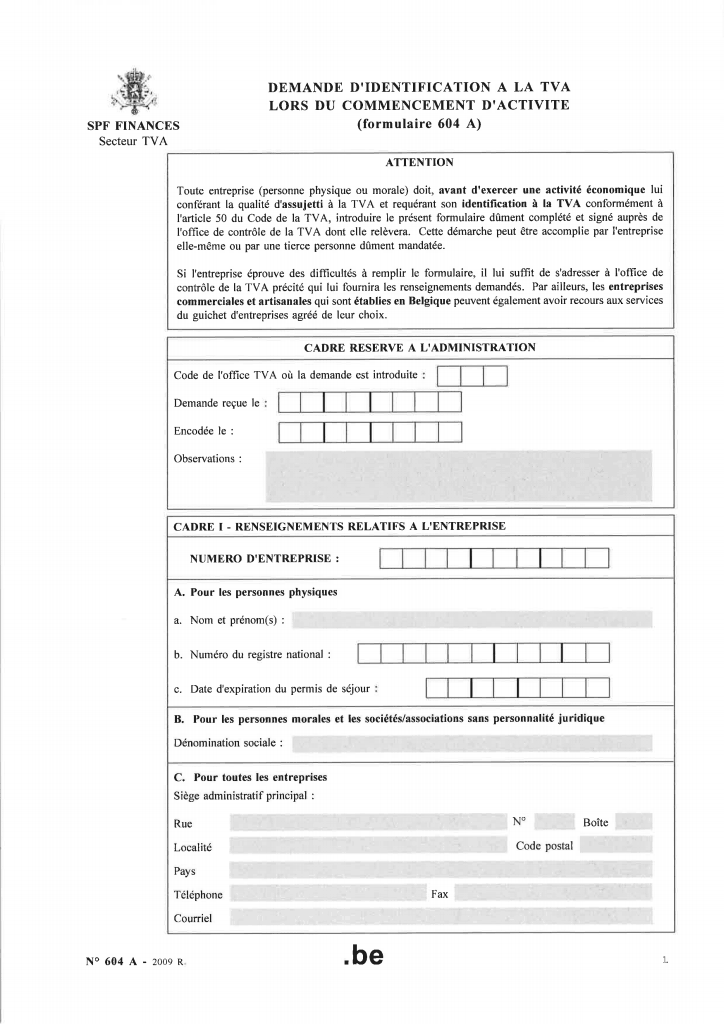

In Belgium there is an open register of companies - Crossroads Bank for Enterprises (BCE/KBO). It includes the following information on companies:

The European Union directive on data protection sets a number of requirements with which companies processing personal data in any EU country must comply. Belgian law has implemented this directive. When a company established in Belgium undertakes activities that involve (directly or indirectly) the processing of personal information about, for instance, its employees or customers as individuals, it must abide by the Belgian data protection regulations.

The processing of data includes any business operations performed upon personal data such as the collection, recording, storage, use, dissemination or destruction of data. The data protection rules apply to the manual processing of personal data (provided the personal data is, or will be, included in a filing system) and to the processing of personal data by automatic means (e.g. by computer), regardless of whether this is done routinely or only once for a specific purpose.

The processing of personal data is permitted if certain conditions are met - for example, when the individuals concerned have given their consent or when processing is necessary for a company to perform a contractual obligation towards the data subject.

The manner of processing is also subject to specific legal requirements. In particular, data can be collected only for legitimate, specific and explicit purposes. If there is further processing for other reasons, the data subjects must, in principle, give their consent to the new processing. There should also be a relevance between the data collected and the purpose of the processing. In addition, the processed data must be accurate and, where necessary, be kept up to date.

Companies are permitted to transfer personal data to third (non-EEA) countries only if the third country in question ensures an adequate level of protection. These processing operations will also have to be notified to the Commission for the Protection of Privacy, except in case of exemptions based on the applicable rules regarding notifications.

Price18 700 EUR

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and Registrar Office incorporation fee

Price5 500 EUR

including registered address and registered agent, NOT including Compliance fee

Price250 EUR

DHL or TNT, at cost of a Courier Service

Pricefrom 600 EUR

Upon registration, a company publishes an apostilled Articles of Association, also called "Status".

Paid-up “nominee director” set includes the following documents

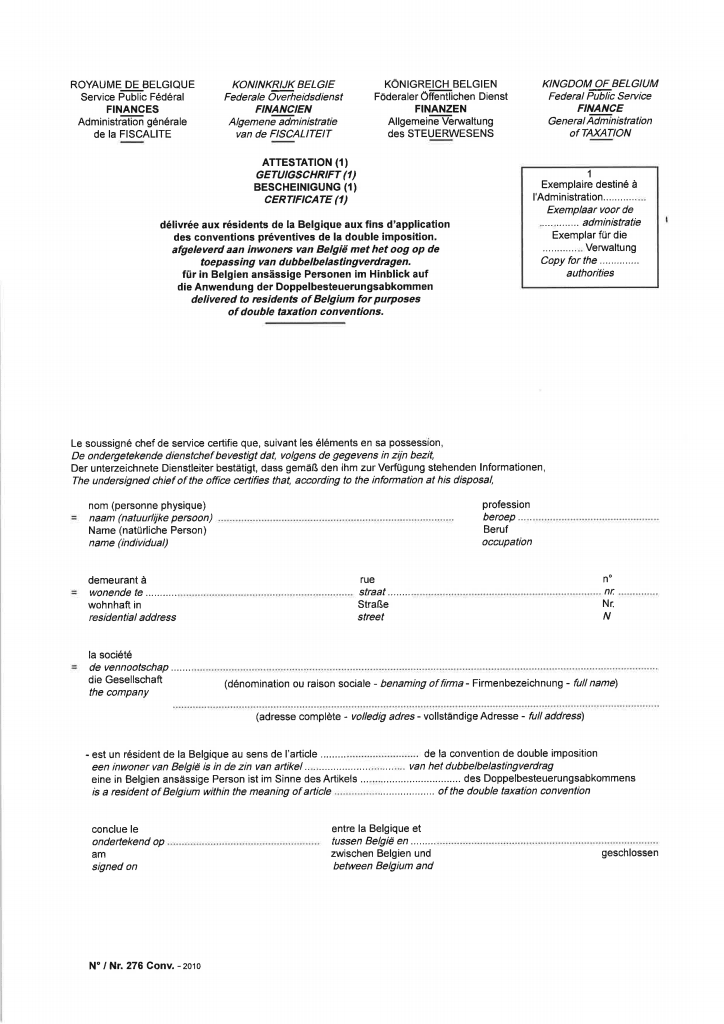

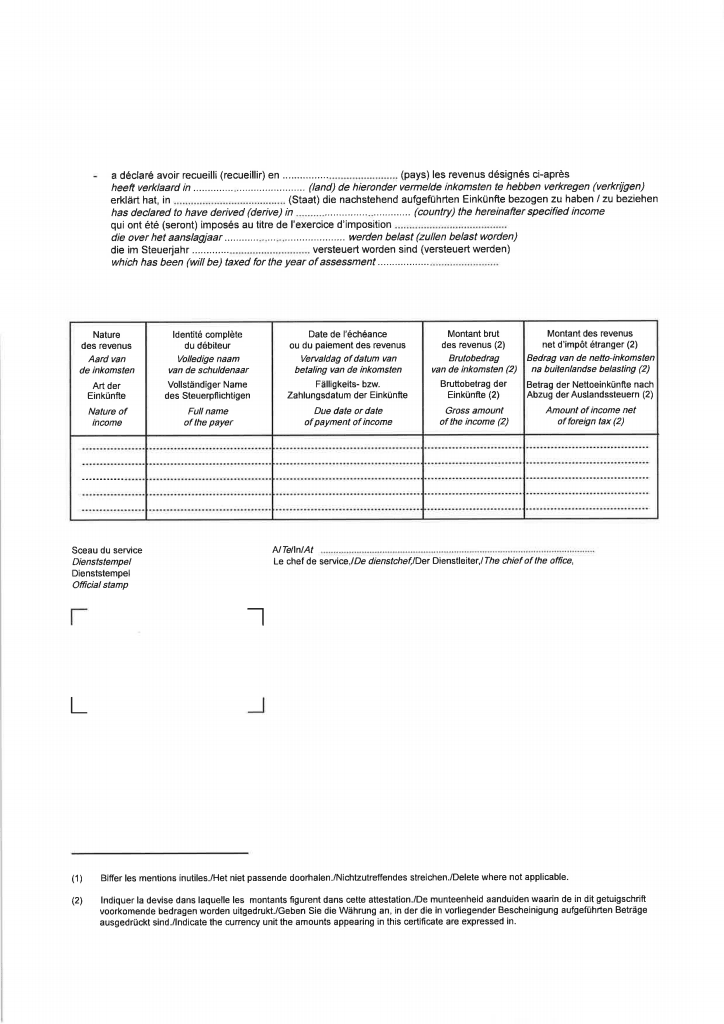

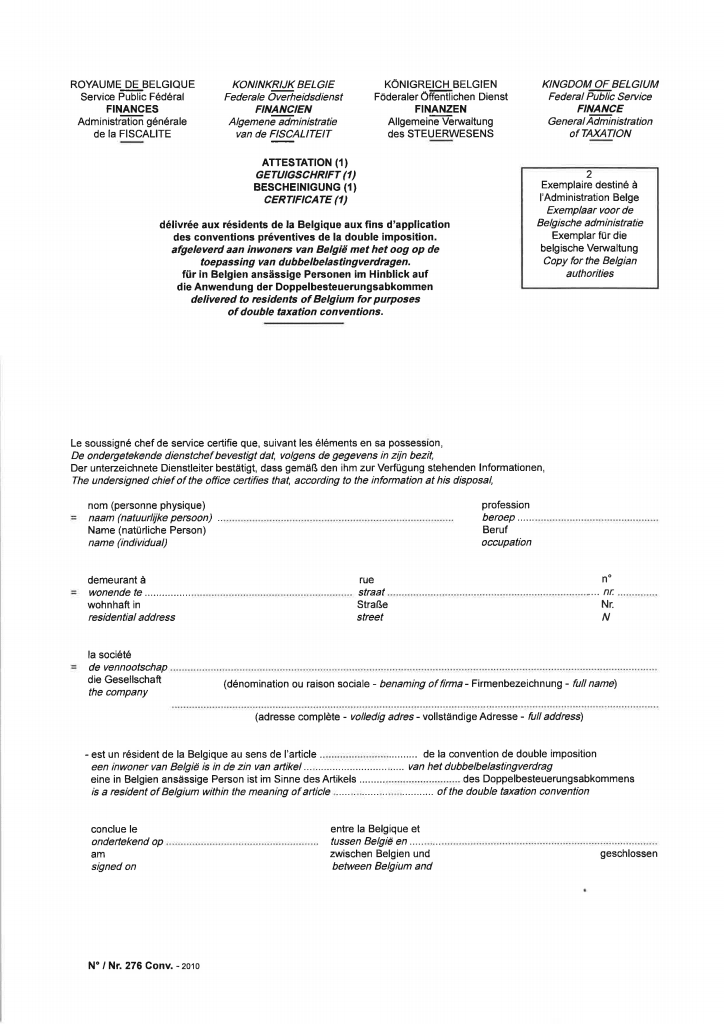

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR