Legal system of Belize is based on English common law, supplemented by local laws. Economic legislation is aimed at attraction of foreign investment. The country is one of the centers of offshore business.

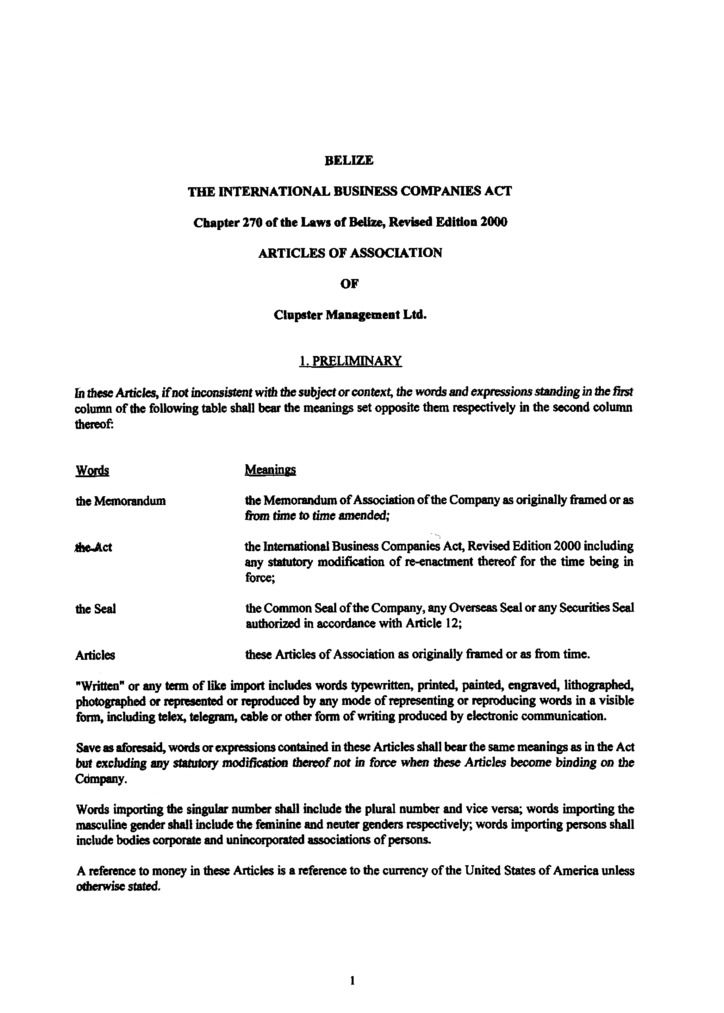

Among the main corporate laws are Companies Act, International business companies act, etc.

Under the legislation of Belize, the following types of commercial entities may be established in Belize to carry on business:

The most common structure is the International Business Company (IBC). It is possible to buy a shelf company of this type or to incorporate a new one. The Registry timescale to incorporate a new company is 24 hours. The timescale for a new turnkey entity is two weeks.

The requirements to the company names in Belize are the following:

To register an IBC company in Belize, you need to go through the following procedure:

1. Obtain an approval of a company name from the Registrar

A company has a right to reserve a name for 90 days for future adoption.

If business name is available, a Certificate of Business Name Registration will be issued.

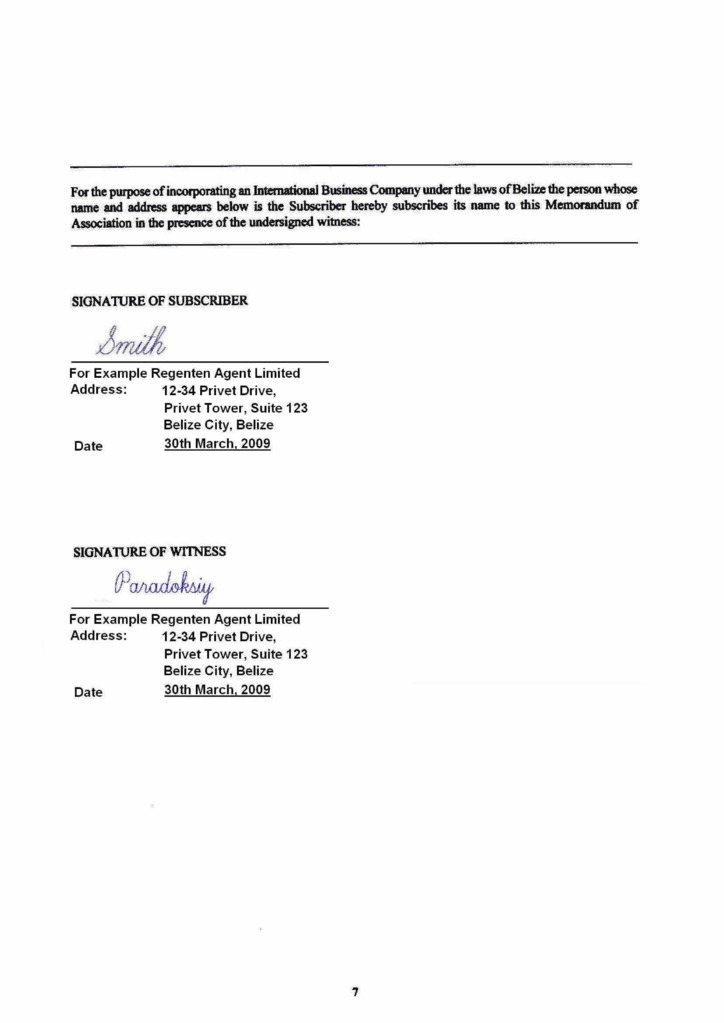

2. File Articles and Memorandum of Association to the Registrar

The Memorandum must include:

The Articles and Memorandum must be subscribed to by a person in the presence of another person who must sign his name as a witness.

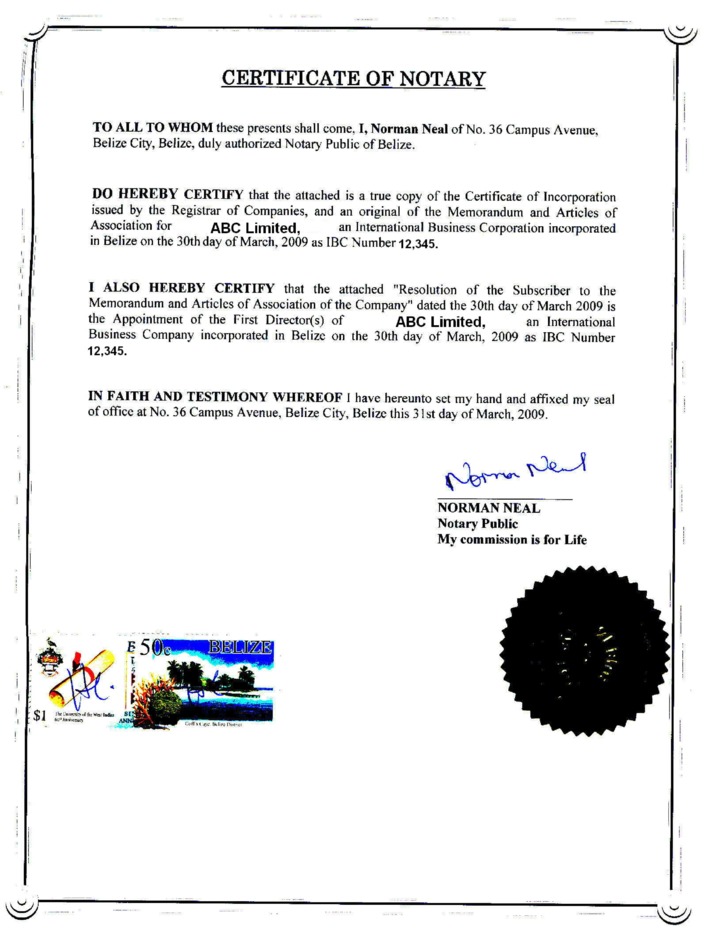

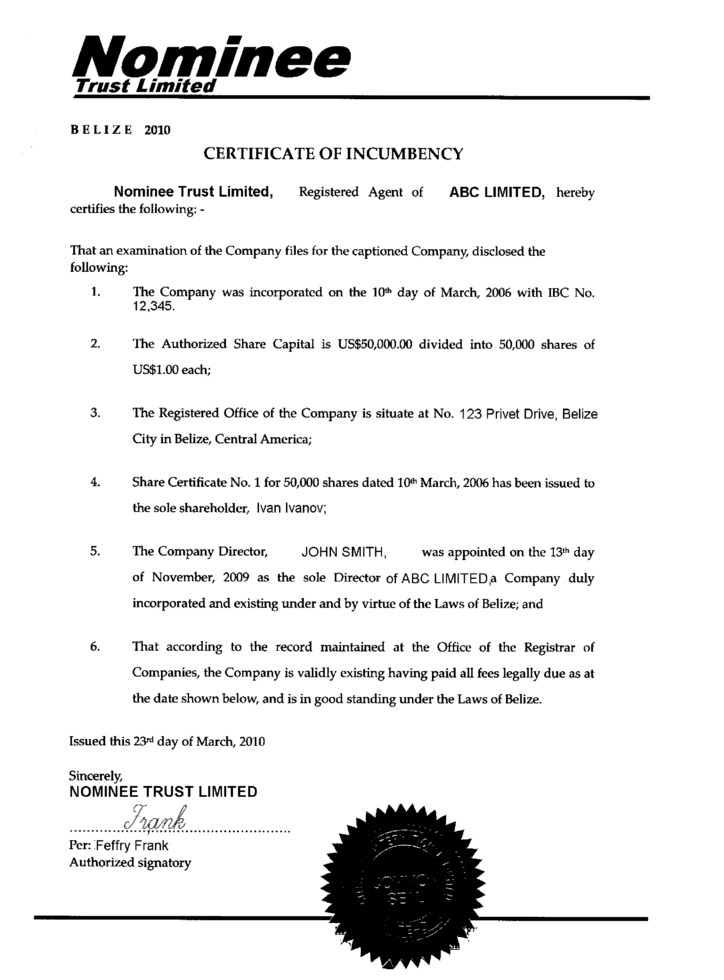

Upon registration a Certificate of Incorporation signed and sealed by Registrar is issued.

After registration a company which employs one or more persons must register for social security with the Belize Social Security Board. The application must be made within 7 days of employing an employee.

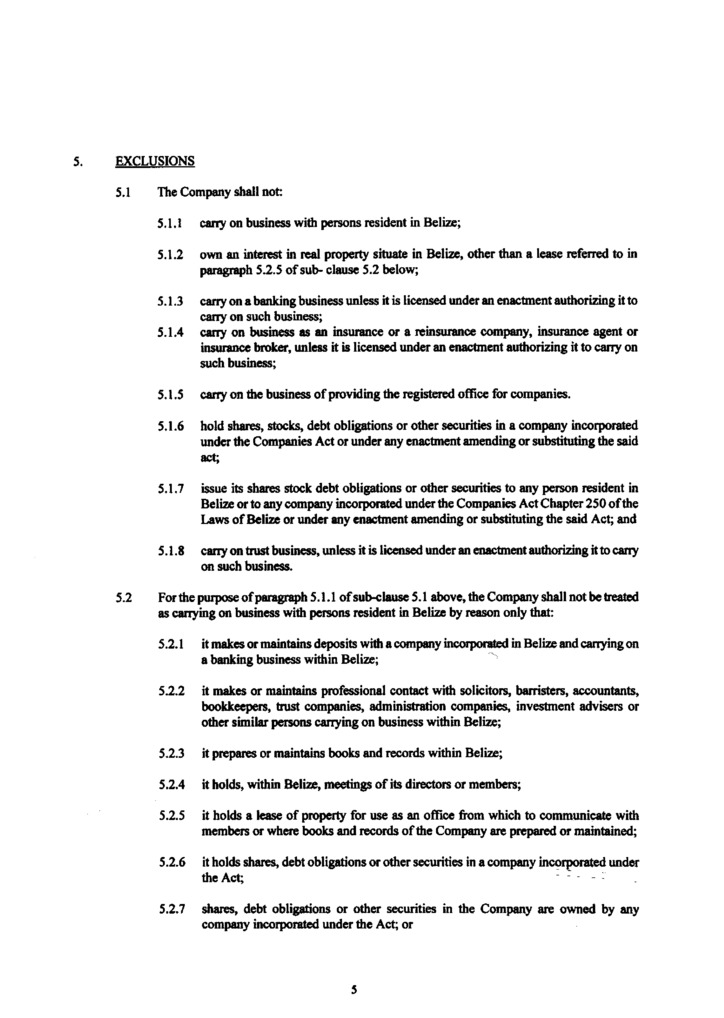

There are a number of restrictions on the activities of business companies. The IBC act prohibits an IBC from:

A company that willfully contravenes the above requirements is liable to a penalty of USD 500 for each day or part of it during which the contravention continues, and a director who knowingly permits the contravention is liable to a like penalty.

Every Belize company must maintain a registered office address in Belize. The Registrar will receive notice of the situation and any change of the registered office. Failure to comply with this requirement will subject the company to a fine not exceeding twenty-five dollars per day for each day of non-compliant business.

The following information and documents shall be kept at the registered address: Register of shareholders and directors, Register of UBO, minutes, resolutions, including resolutions consented by directors, shareholders and officers, Memorandum and Articles of association, and common seal imprint. According to the latest changes in the Belizean law, it is also required to keep accounting records at the registered office or a resolution on another place within or outside Belize.

From the date of incorporation mentioned in the certificate of incorporation the body corporate known by the name in the memorandum shall have a common seal, its imprint should be kept at the registered office. Failure to comply with this requirement will subject the company to a fine not exceeding twenty-five dollars per day for each day of non-compliant business.

The redomiciliation of companies either to or from Belize is permitted.

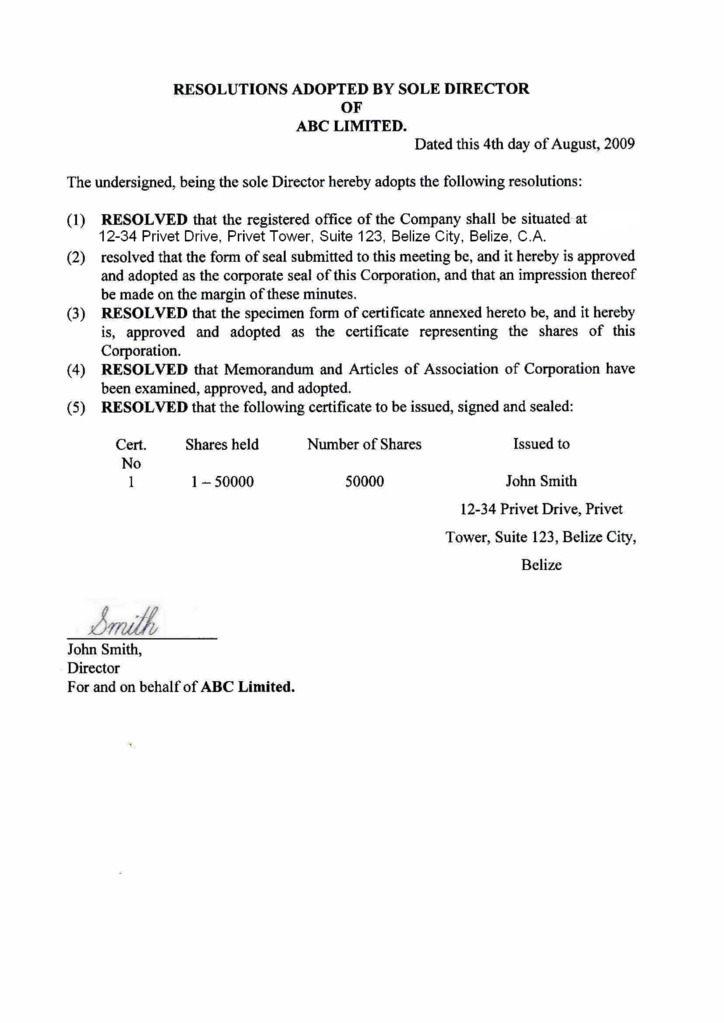

A Belize company is required to have a minimum of one director who can be a natural person or a body corporate, resident or non-resident.

There is no requirement to hold directors’ meetings in Belize or elsewhere.

Director’s details are disclosed to the local agent but do not appear on the public file.

A company secretary is not a requirement.

Belize companies may have one or more shareholders, individuals or corporations of any nationality or residence. Nominee shareholders are permitted.

The law does not require to hold Annual General meetings. If necessary, meetings of shareholders (and directors) may be held by phone or other electronic means. Shareholders (and directors) may vote by proxy.

Shareholders’ details are disclosed to the local agent but do not appear on the public file.

In 2017, Belize adopted a series of amendments to the International Business Companies Act, which introduced the Beneficiary Registry. Registration agents are required to maintain and keep the registers. And in accordance with the latest amendments to the legislation, the Register of Beneficiaries must be filed with the relevant state body.

Access to the Registry of beneficial owners of the company remains non-public and is available to the competent authorities of Belize on request.

The following information is collected about the beneficiary: full name; date on which the person became a beneficiary; address and place of residence; date of birth; position held; details of the beneficial interest.

There is a fine of USD 500 for each day of violation for failure to provide or maintain the data. For intentional submission of invalid information about the beneficiary, there is a fine of USD 50 000.

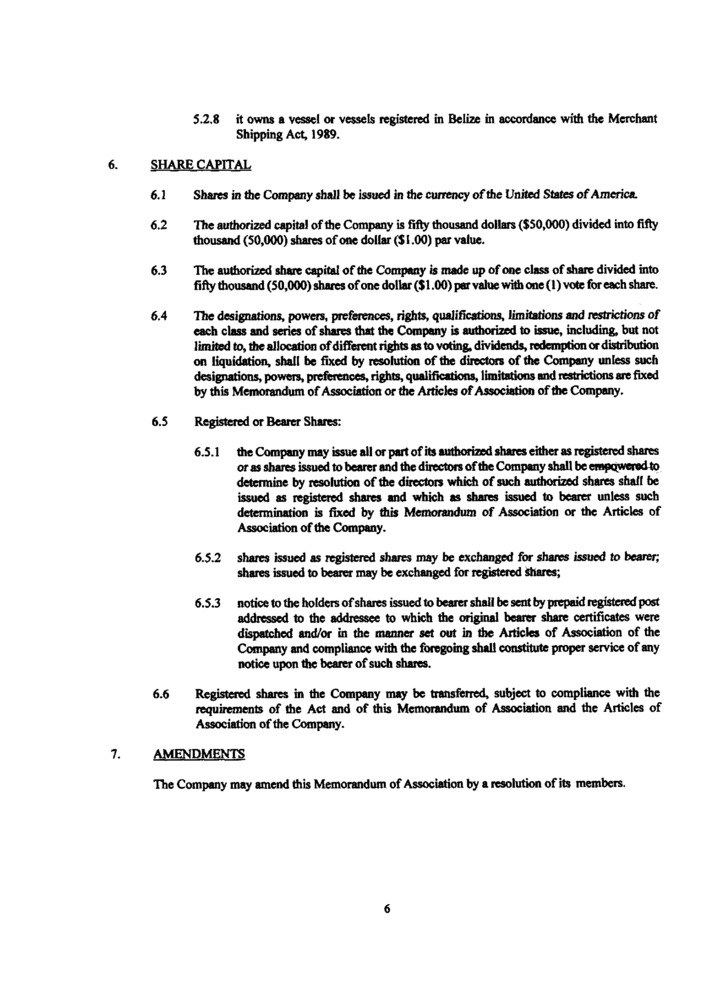

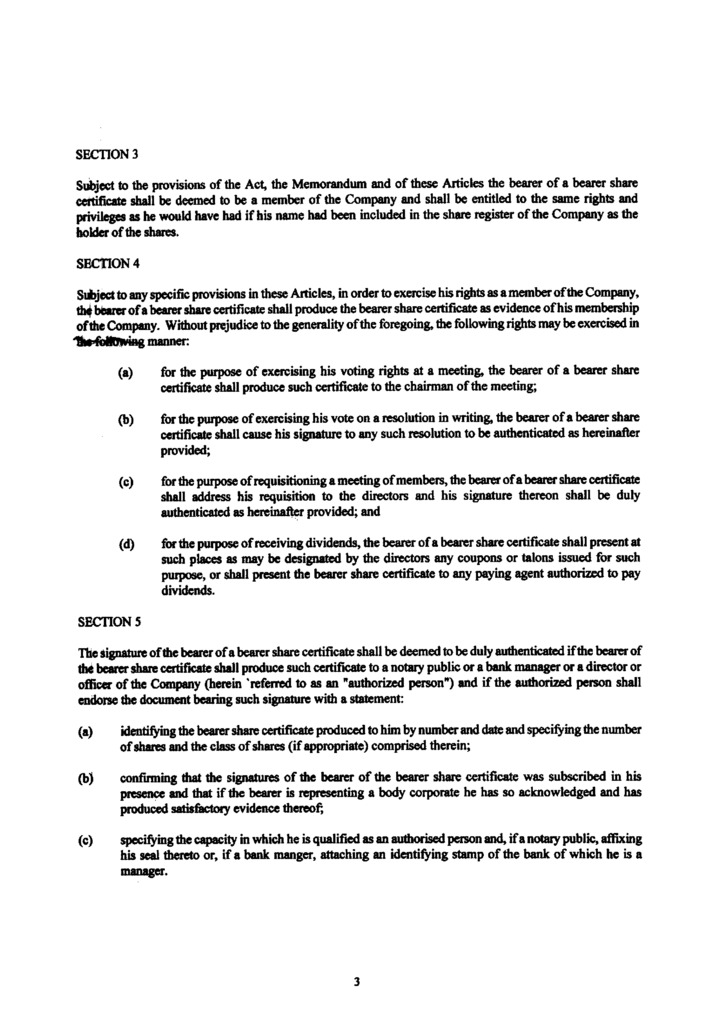

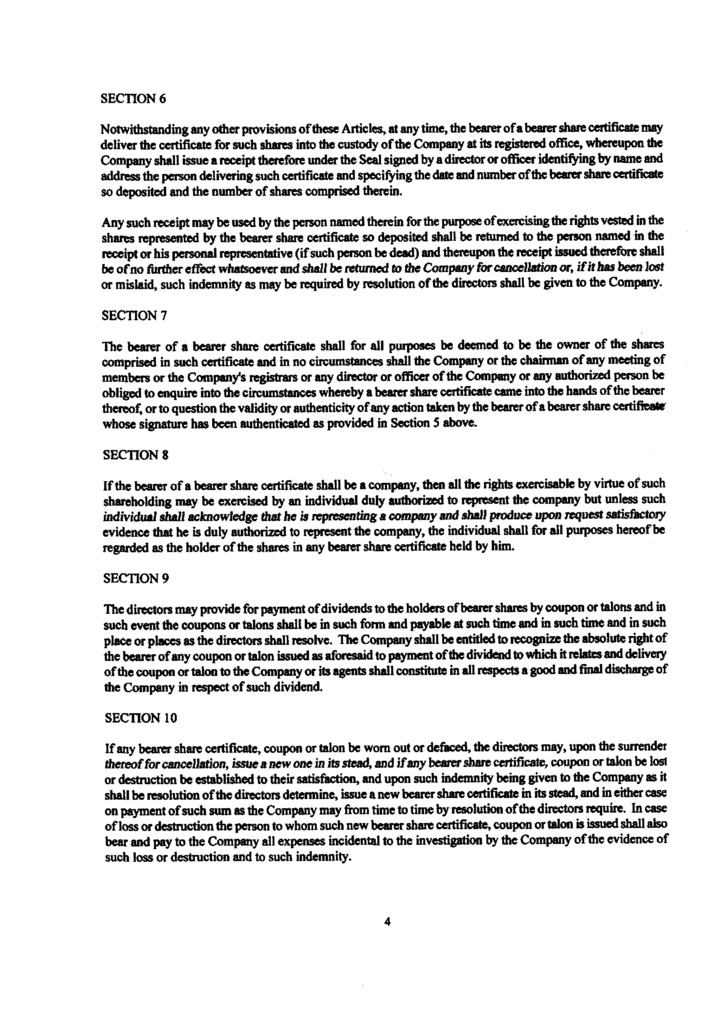

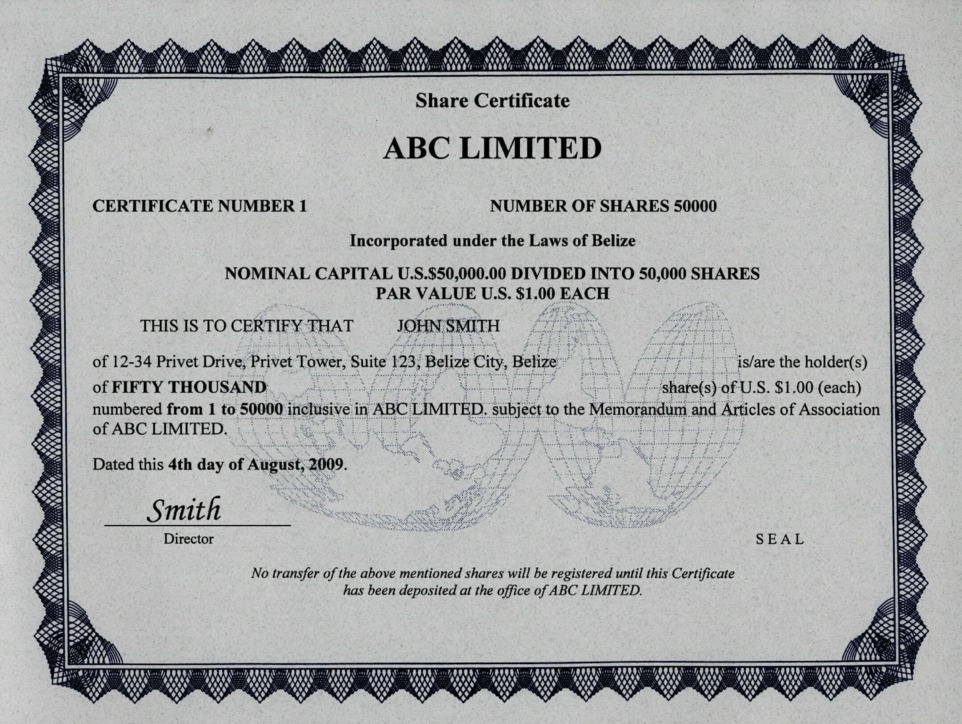

The share capital of an IBC can be denominated in any currency. There is no minimum authorized share capital and no mandatory timeframes for it to be paid up, also, there are no requirements to the size of issued share capital and paid share capital, but shares must be paid up at their issue. Usually the share capital is USD 50 000 which is divided into 50 000 shares of USD 1 each. Shares with no par value are permitted, as well as bearer shares, but the latter can only be held in custody of a local registered in Belize.

Price1 790 USD

the full cost of the Company's purchase services consists of registration services, its maintenance (paid in advance for one hour at the time of registration), the cost of a set of documents and their courier delivery to the destination

Priceвключены

Stamp Duty and Registrar incorporation fee

Price1 640 USD

government fee + payment for registered agent services (including legal addresses), excluding Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 850 USD

Price705 USD

for 1 year, not including POA

Price530 USD

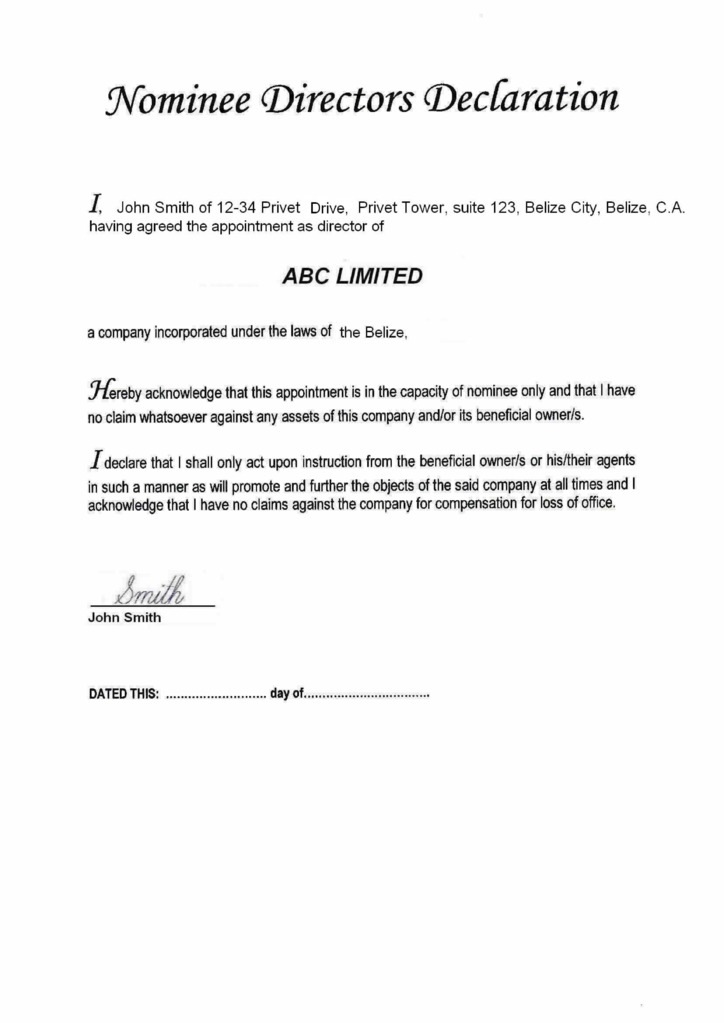

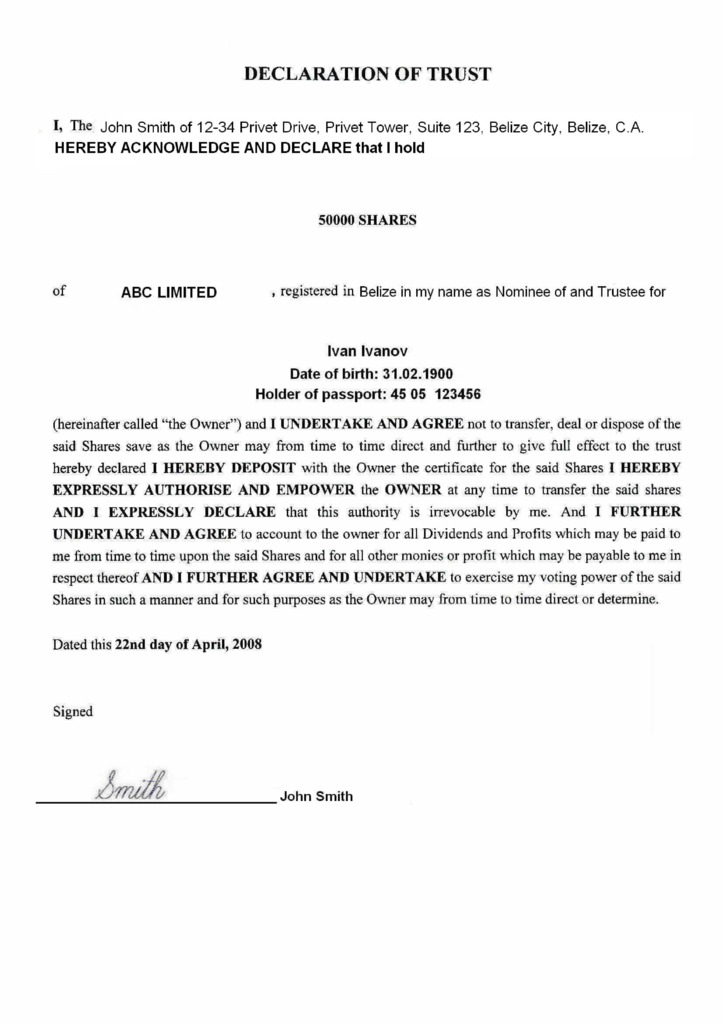

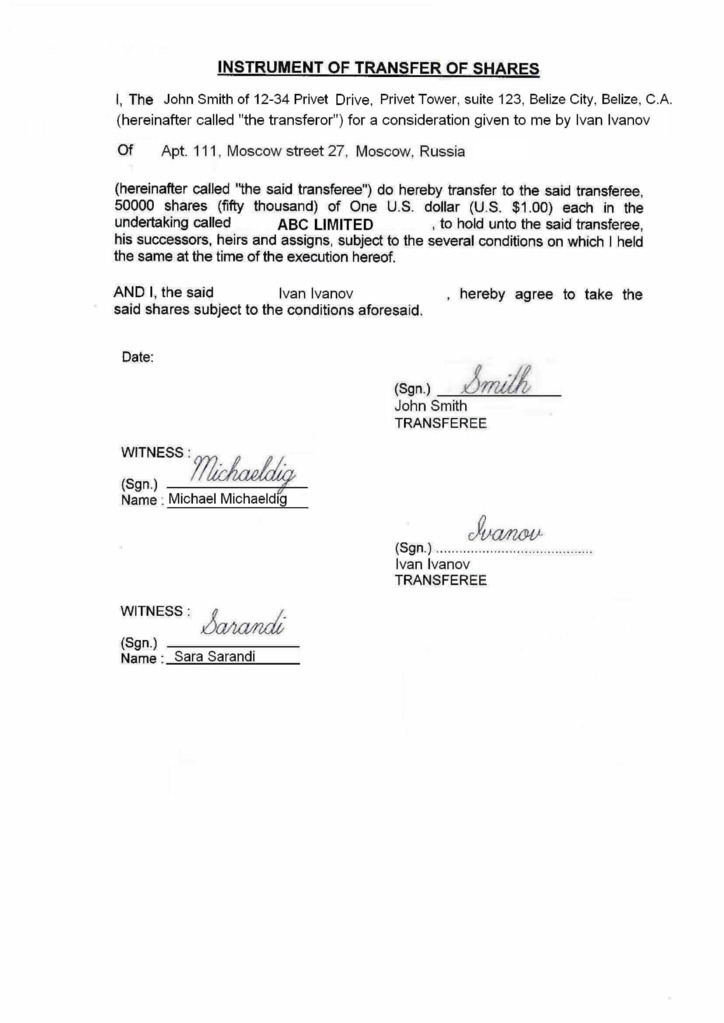

Paid-up “nominee shareholder” set includes the following documents

Price350 USD

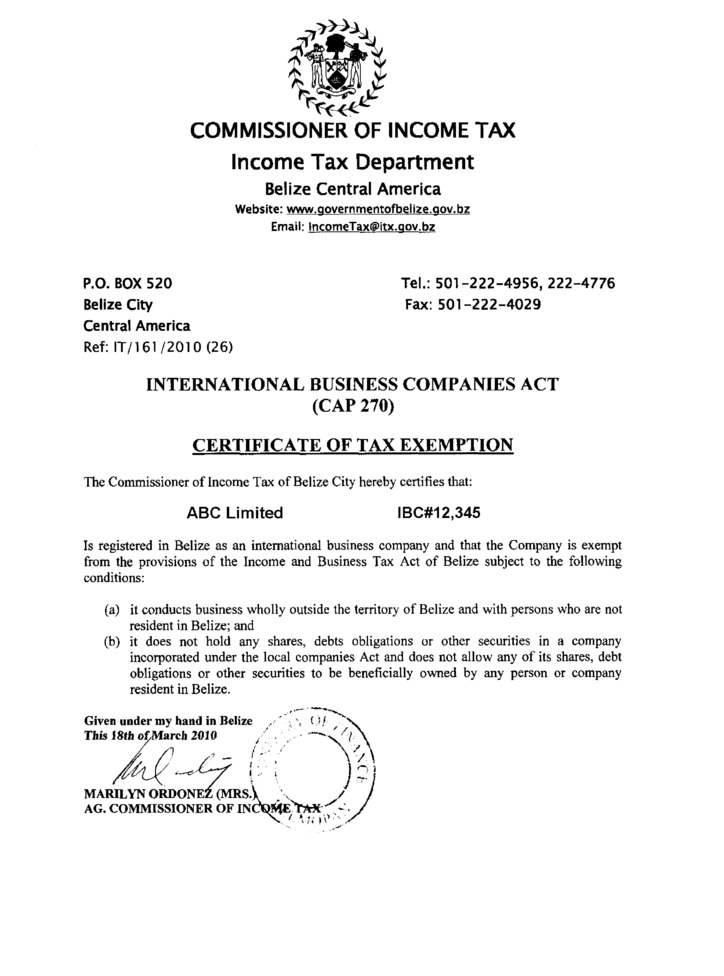

Company’s tax residence certificate for access to double tax treaties network

Price320 USD

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Price300 USD

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price250 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price350 USD

Price100 USD