The legal system of Canada is English common law for all matters within federal jurisdiction and in all provinces and territories except Quebec, which is based on the civil law, based on the Custom of Paris in pre-revolutionary France as set out in the Civil Code of Quebec.

In Ontario, the legal system is based on English common law.

The principal forms of business organization in Ontario are:

The most common structure in British Columbia is the corporation.

Corporation is a limited liability company with transferable ownership, continuous existence and separate legal entity. It can be formed in one of two ways: provincially and federally. This means that choosing to register your business in Canada as a corporation creates a separate legal entity under the laws of the federal government or one of the provinces or territories. Each jurisdiction has its own laws, but many corporations that operate in more than one province are incorporated federally.

Federal incorporation lets you do business under the same name in all provinces and territories, but it's more expensive and a little more work to setup and maintain.

Provincial incorporation is likely sufficient for most ecommerce business owners operating out of Canada.

If you register a company in British Columbia, according to the Business Corporations Act for the Province of British Columbia, there is no requirement for corporations to appoint local Canadian directors. As such, non-Canadian residents can incorporate Canadian corporations in this province.

Every corporation in Canada must have a name; it may be a corporate name or a numbered name.

Company name must be distinct from the names of all other corporations in British Columbia.

A corporate name should contain three elements:

A company name should not contain any prohibited words or phrases, such as “Parliament Hill”, “RCMP”, “Cooperative”, “United Nations”, “government”, “ministry”, “bureau”, “secretariat”, “commission”, “certified”, “British Columbia” or “BC”, “bank”, “trust”, “insurance”, “trust”, “stock exchange”, as well as well-known names, special characters, words suggesting connection with government, crown or royal family.

Company name should not be obscene or too general.

Numerals may be used in company names as the distinctive element. The incorporation number may be used as the name of a British Columbia company. The accepted format is “345678 B.C. Ltd.”.

In order to have the exclusive use of a corporate name in Canada, you must provide two things to Corporations Canada:

An approved federal corporate name offers an extra degree of protection of your rights to that name. Specifically, federal incorporation allows your business to operate using its corporate name right across Canada, which is important if you decide to expand your business to other provinces or territories.

Every incorporating jurisdiction in Canada screens proposed corporate names. However, if you incorporate under the legislation of one province or territory and later want to expand your business to another province or territory, you could find that another corporation is already using a name similar to yours in that other location.

Please note that the Province of Quebec does not currently provide corporate name data to NUANS. It is your responsibility to verify with the Registraire des entreprises, Quebec that the chosen corporate name is not used in Quebec by another business.

Instead of asking Corporations Canada to approve a name for your corporation, you can also choose to have a number name assigned (e.g., 1234567 Canada Ltd.). In such cases, Corporations Canada simply assigns the next available number when processing the articles. You must ask for a number name when you apply for your Articles of Incorporation. A NUANS Name Search Report is not needed.

Many companies choose this option when a corporate name is not important to their business. This ensures faster processing and saves the expense of a NUANS Name Search Report.

Another option is to apply for a number name and ask for a name change later. To replace a number name by a corporate name, you must amend your Articles of Incorporation by filing Articles of Amendment and paying the CAD 200 fee. In this case, a NUANS Name Search Report is required.

Some incorporators choose this option when they want to incorporate a business but do not have enough time to obtain approval for a corporate name.

To incorporate a company in British Columbia, the following steps are required:

1. Reserve the company’s name with the Corporate Registry.

If the company intends to use a specific name, that name must be approved and reserved by the Corporate Registry. This is to ensure the company’s name can be distinguished from the names of other incorporated companies and that the name meets specific guidelines established by the registrar of companies. The name reservation is for a period of 56 days.

If you choose to use the incorporation number as the company’s name, you do not need a name approval and reservation. The incorporation number is assigned by the Corporate Registry at the time the Incorporation Application is electronically filed with the Corporate Registry.

The fee to submit online is CAD 30 and a BC OnLine service fee of CAD 1.50 plus GST.

2. Enter into an incorporation agreement.

Before a company can be formed there must be an incorporation agreement signed by each incorporator. This is required even if there is only one incorporator. Usually the incorporator(s) will also be the shareholder(s) and director(s) once the company is incorporated. The Business Corporations Act specifies

that this incorporation agreement must contain:

The incorporation agreement must be kept by the company as part of the company’s records.

3. Establish the company’s articles.

Every company must have a set of articles. The company’s articles are the rules that govern the conduct of the company and its shareholders, directors and officers.

The articles must be kept by the company as part of the company’s records.

4. File an Incorporation Application with the Corporate Registry.

The Incorporation Application must be submitted electronically over the Internet by visiting Corporate Online.

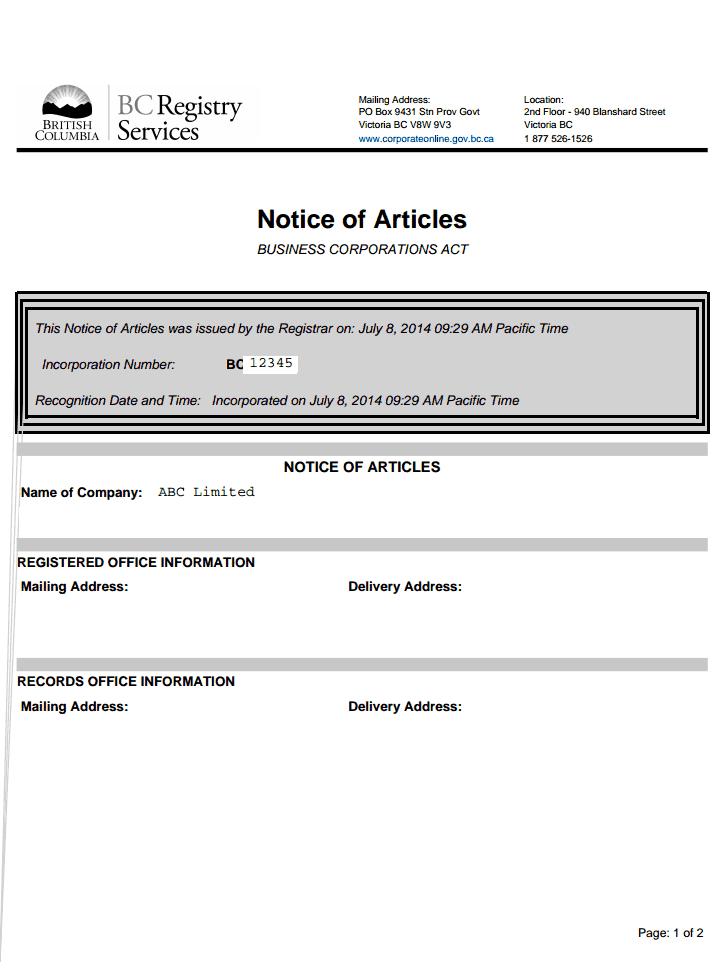

The Incorporation Application must be submitted electronically over the Internet by visiting Corporate Online at www.corporateonline.gov.bc.ca. When the filing is completed, the company is incorporated and you will be assigned an incorporation number at that time.

After you have filed the Incorporation Application electronically and the company is incorporated, the Corporate Registry will send you the original Certificate of Incorporation, a certified copy of the Incorporation Application and a certified copy of the Notice of Articles. These documents must be kept by the company as part of the company’s records.

An incorporation number for the company is displayed in the upper right hand corner of the Certificate of Incorporation and on the cover sheet accompanying the documents. You will need the incorporation number of the company when filing other documents with the Corporate Registry.

The cover sheet also includes the Business Number issued by Canada Revenue Agency.

The fee to incorporate a company by filing an Incorporation Application using Corporate Online is CAD 350 and a BC OnLine service fee of CAD 1.50 plus GST.

Two to three business days to incorporate (by regular processing). Certificate of Incorporation available from the British Columbia Registry Office in five to seven business days.

A company must maintain a registered office and a records office in British Columbia. The registered office and the records office may be located at the same place. An agent may be authorized by the company to maintain the records office of the company.

A company must keep the following records at its records office:

The above-mentioned records may, after 7 years from the date on which they were received for deposit at the records office, be kept by the company at a location other than the records office so long as those records can be produced from that other location by the person who maintains the records office for the company on 48 hours' notice, not including Saturdays and holidays.

A Canadian corporation is not required to have a seal. If you want to have a corporate seal for your corporation, you may purchase one from a legal stationery store or commercial supplier.

The redomiciliation of companies to or from British Columbia is permitted.

Subject to section 310 of the Business Corporations Act, a company in British Columbia may, if it is authorized by the shareholders and by the registrar, make an application to the appropriate official or public body of another jurisdiction requesting that the company be continued into that other jurisdiction as if the company had been incorporated under the laws of that other jurisdiction.

Before the registrar will authorize the continuation out of a company, the registrar requires the company to be in good standing. Good standing means the company has complied with section 51 (up to date on annual report filings) and section 120 (required number of directors) of the Business Corporations Act.

The fee to file an Application for Authorization to Continue Out (Form 45) is CAD 350. If you wish the continuation out to be processed on a priority basis, an additional CAD 100 will be required.

A company seeking to be continued into a foreign jurisdiction must, before applying to that foreign jurisdiction for continuation into that jurisdiction, apply to the registrar for an authorization. The registrar must authorize the company to continue into the foreign jurisdiction if the registrar is satisfied that the company has filed with the registrar all of the records that the company is required to file with the registrar under this Act. The authorization given by the registrar expires 6 months after the date on which that authorization was given.

Promptly after the date on which a company is continued into another jurisdiction, the continued corporation must file with the registrar a copy of any record issued to it by the other jurisdiction to effect or confirm the continuation. After a record is filed, the registrar must publish in the prescribed manner a notice that the company in respect of which the record was filed has been continued into that other jurisdiction.

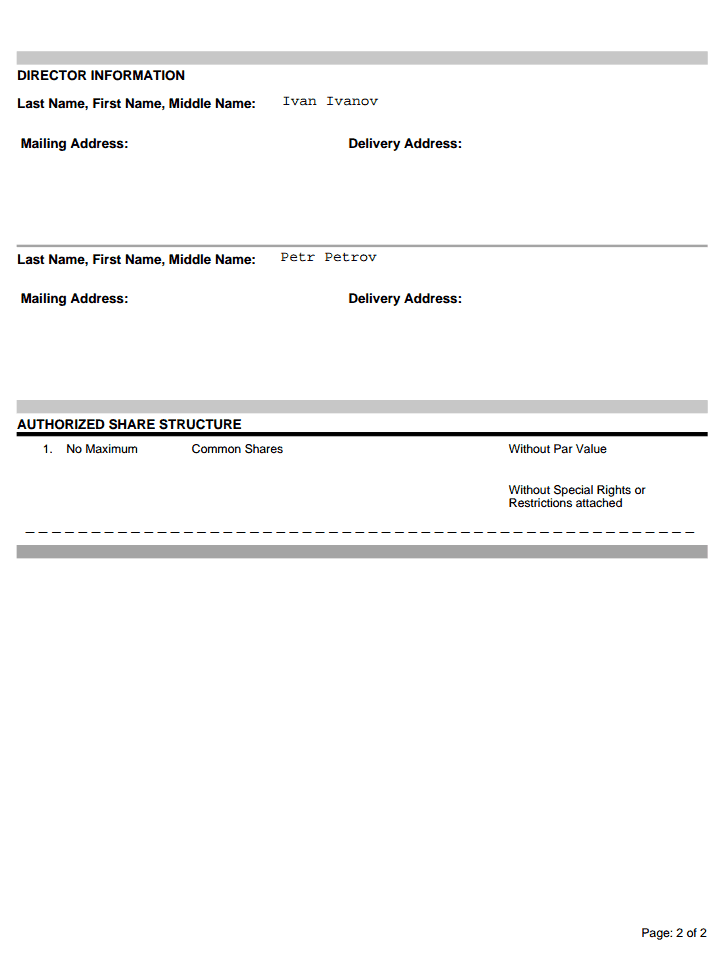

A company in British Columbia should at least have one director, as well as a Canadian federal company. A director must be:

While at least 25 percent of the directors of a federal corporation must be resident Canadians, or if a corporation has fewer than four directors, then at least one of them must be a resident Canadian, resident Canadian directors are not required in accordance with the British Columbia Business Corporations Act.

Directors’ details are searchable only if corporate name is known.

Most boards of directors meet on a regular basis to oversee the business operations of the corporation. Such meetings may be held monthly, quarterly or annually, depending on the needs of the corporation. Directors may also need to meet occasionally to conduct special business.

Meetings of the board can be held whenever and wherever the board wishes, unless the corporation’s by-laws or Articles say otherwise. In all cases, however, a quorum of directors must be present.

Directors may conduct business through signed resolutions instead of meetings. Note, however, that in such situations the signatures of all directors are required. These signed resolutions have the same value as they would have if they were adopted at a meeting of the board of directors. This way of conducting the business of the corporation can be very useful for small companies with only one or a few directors.

Note that it is also possible for one or more directors to participate in a meeting by telephone or electronically, as long as the corporation’s by-laws permit it and as long as all participants in the meeting can communicate fully.

Corporate Secretary is not required. An individual may hold more than one of the positions in a corporation. For example, the same individual may be a shareholder, a director and a secretary, or even the sole shareholder, sole director and sole secretary.

In British Columbia, one or more individuals 18 years of age or older who are of sound mind and not in a state of bankruptcy may form a corporation. Similarly, one or more corporations or bodies corporate may incorporate a business.

A person becomes a shareholder by buying shares, either from the corporation or from an existing shareholder. A person ceases to be a shareholder once his or her shares are sold either to a third party or back to the corporation (in accordance with the terms of the Articles of Incorporation) or when the corporation is dissolved.

After paying for their shares, shareholders have the right to:

The shareholders’ liability in a corporation is limited to the amount they paid for their shares; shareholders are usually not liable for the corporation’s debts. At the same time, shareholders usually do not actively run the corporation.

Shareholders who are entitled to vote can attend an annual shareholders’ meeting. A notice of this meeting is sent not more than 60 days and not less than 21 days before the meeting date. For example, if the meeting is to take place on May 20, the notice should be sent no sooner than March 22 and no later than April 30.

The directors of a corporation must call the first shareholders’ meeting within 18 months of the corporation’s date of incorporation. This meeting is usually held after the first organizational meeting of the directors.

A corporation must hold a shareholders’ meeting on a date that is no later than 15 months after holding the last preceding annual meeting, but no later than six months after the end of its preceding financial year.

In a small business where one or two people act as directors, officers and shareholders, meetings are not necessary. Shareholders in these corporations often prefer to act through written resolutions. If every shareholder signs a written record that sets out the terms of the necessary resolutions, then a shareholders’ meeting is not needed.

The annual meeting must be held in British Columbia. An annual meeting may be held outside British Columbia only in cases where the corporation’s articles permit it or if all voting shareholders agree.

Also, where the corporation’s by-laws permit it, the directors of a corporation may decide that a meeting of shareholders will be held entirely by means of a telephonic, electronic or other communication means that will permit all participants to communicate adequately with each other during the meeting. In such cases, it is the responsibility of the corporation to make these facilities available.

British Columbia was one of the first Canadian provinces to pass legislation in 2019 requiring the disclosure of information about the beneficiaries of local companies.

Such information includes: full name; date of birth; citizenship; last known address.

The register is not public, but the information will be available to employees of the Ministry of Finance involved in inspections and compliance, as well as law enforcement agencies. If necessary, information may also be transferred to the Canadian Revenue Agency.

There is no minimum share capital in British Columbia. Capital can be denominated in any currency. The standard currency is Canadian dollar.

One of a corporation’s first activities following incorporation is to issue shares.

The corporation cannot issue a share until it actually receives full consideration (payment) for that share. This consideration is generally in the form of money, although it can also be in the form of services or property given to the corporation. A person’s payment for the share(s), in a form agreed upon by the directors, represents that person’s investment in the corporation.

Once a share has been issued, the shareholder is entitled to a share certificate. This certificate must state:

Shares are issued without nominal or share value. A share certificate does not carry a monetary value.

A company may apply to be dissolved if:

In order to apply for voluntary dissolution, a company must

The Application for Dissolution must be submitted electronically over the Internet by visiting Corporate Online.

The fee to file an Application for Dissolution is CAD 21.50 plus GST.

A company may liquidate if it has been authorized to do so by a special resolution. At the time that the special resolution is passed, the company, by an ordinary resolution, must appoint as liquidator one or more persons, and may set, or may authorize the directors to set, each liquidator's remuneration. An appointment of a liquidator takes effect on the commencement of the liquidation.

In a voluntary liquidation, the company, by an ordinary resolution, may direct the liquidator not to do certain specified things without the approval of a general meeting of the company or without the written consent of certain specified shareholders, or of a certain specified number of shareholders.

Promptly after the resolutions are passed, a company must file a statement of intent to liquidate with the registrar. After a statement of intent to liquidate is filed with the registrar, the registrar must furnish to the company a certified copy of the statement of intent to liquidate.

The court may order that the company be liquidated and dissolved if:

An application to the court in respect of a company in liquidation may be made by the company, a shareholder of the company or a beneficial owner of a share of the company, a director of the company or any other person, including a creditor or liquidator of the company, whom the court considers to be an appropriate person to make the application.

PriceUSD 3 000

including incorporation tax, state registry fee, NOT including Compliance fee

Priceincluded

Stamp Duty and Corporate Registry incorporation fee

PriceUSD 2 750

including registered address and registered agent, NOT including Compliance fee

PriceUSD 275

DHL or TNT, at cost of a Courier Service

PriceUSD 1 325

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

PriceUSD 385

simple company structure with only 1 physical person

PriceUSD 165

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

PriceUSD 220

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

PriceUSD 495

PriceUSD 110