The principal forms of business organization in Czech republic are:

- sole trader;

- joint-stock company;

- limited liability company;

- public trading company;

- limited partnership;

- cooperative.

The most common structure is the limited liability company.

There is a range of requirements to the company name in Czech Republic:

- a company name shall not be identical with or resemble too nearly to the name of an existing company;

- it must comprise the words "společnost s ručením omezeným" (Limited Liability Company), or at least one of the admissible abbreviations, "spol. s r.o." or "s.r.o.";

- it cannot be deceptive;

- it should not contain the following words:“Bank”, “Trustee Company”, “Assurance”, “Building Society”, “Trust Company”, “Royal” etc.

The following steps are required to incorporate a Limited liability company in Czech Republic:

- Check for uniqueness of company's name online: The uniqueness of the company name can be verified by accessing a database on the Ministry of Justice's Web site (www.justice.cz).

- Obtain extracts of criminal record and real estate at Czechpoint Offices: Real estate extract can be obtained from so-called Czechpoints, which are usually located at the post offices, municipal and district offices. Since 2013, it is possible to obtain necessary documents online with a hard copy delivery, but only for companies with an address in the Czech Republic.

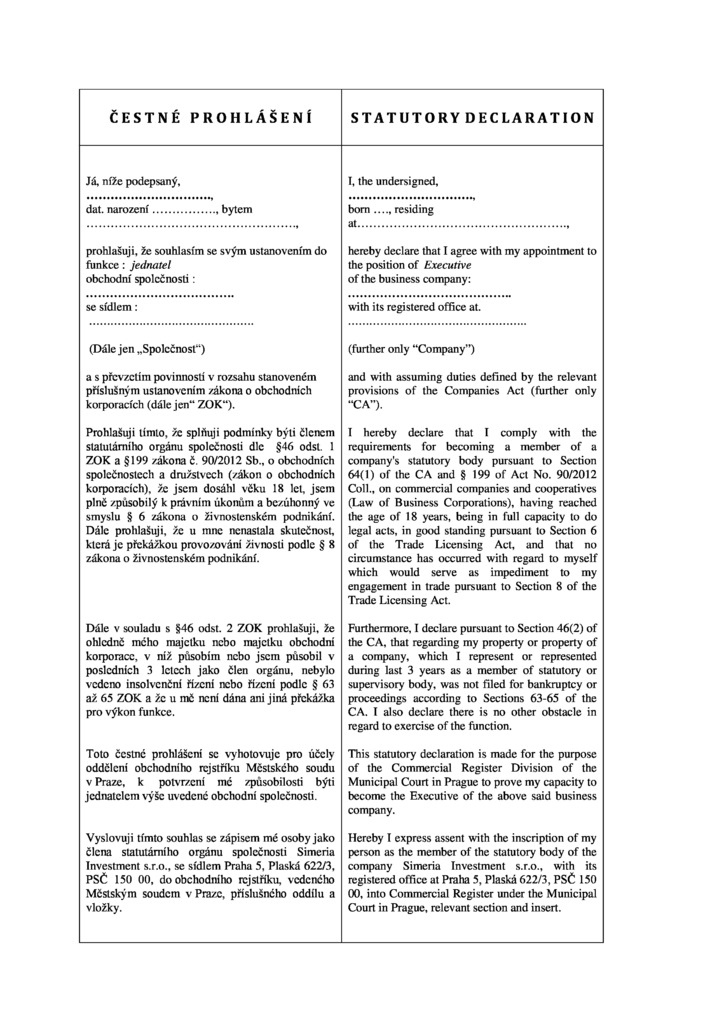

- Notarize articles of association: Fees to notarize the articles of association depend on the amount of the company’s registered capital and on the number of copies of the notarial record required by the company's founders. The minimum fee is about CZK 4,000, and the maximum is about CZK 113,000, including 21% VAT. The notary public is responsible for the compliance of the contents of the company’s articles of association with Czech law. The notary prepares the articles of association according to the founders' requirements. Certain notaries public require the following documents before executing the articles of association: an affidavit from the company managers; confirmation from the owner of premises where the seat will be located that the company is entitled to have its seat on those premises, along with an extract for the premises from the Real Estate Register. The founders must comply with the requirements stipulated by the Czech Commercial Code. They must confirm their compliance in an affidavit submitted to the City Court. Since January 2012, it is no longer required to submit the founders' signatures to the City Court.

- Obtain confirmation of the administrator of the capital contribution of the company, along with the confirmation of the bank that the capital contribution is held in the company’s special bank account: Until the company is registered, the registered capital is usually blocked in the special bank account. Opening a special bank account usually costs about CZK 5,000. However, some banks open special accounts for nothing on condition that the company will open a bank account after its incorporation.

- Register with the Trade Licensing Office and obtain extract of the trade license: The company has to register its business activities with the Trade License Office to be able to obtain an extract of its trade license. The required documents are memorandum of association if the company has been founded but not yet established (i.e. registered with the Commercial Register); if the company has already been registered with the Commercial Register, an excerpt thereof that cannot be older than 3 months will be required; proof of legal use of premises (i.e. a notarized copy of the (sub)lease agreement or the excerpt of the Real Estate Cadastre); and proof of payment of the administrative fee. The Trade License Office must complete the registration process within 5 days from the day when all required documents were submitted. After the completion of the registration process, the Trade License Office issues the excerpt of the trade license register which must be delivered to the applicant, either picked-up personally by the applicant at the Trade License Office or delivered by mail. The first issue of the trade license is free of charge. It is also possible to file the application online; however, the applicant must have a certified signature, otherwise such application will not be considered effective.

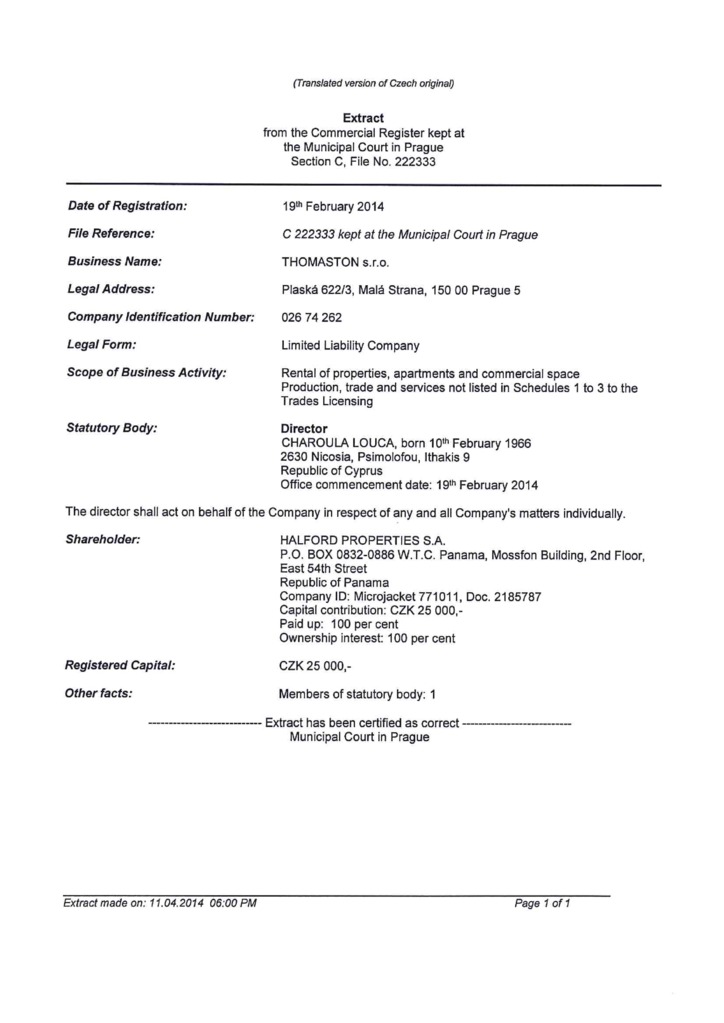

- Register in the Business Registry of the Regional Commercial Court: The Czech Commercial Code and the Czech Civil Procedure Act were amended to comply with European Community law (effective July 1, 2005) and to simplify and speed up registering in the Commercial Register. The amendment introduced standard forms for applications, reduced the number of participants to the proceedings, introduced a simplified procedure for registration, stated the exact time limits for decisions and their issuance and entries, introduced the "silence-is-consent" rule, and set limits for implementing the full electronic administration of the Commercial Register. Since July 1, 2006, the time limit for the court to decide on registration is 5 working days. To register a newly founded company in the Commercial Register, an application must be submitted to the relevant court administering the register. This application must be completed on a standard form and signed by all first directors of the company (or their proxy, if applicable) before a notary. The following documents must be enclosed with the application for company registration in the Commercial Register: (a) the company’s articles (memorandum) of association in the form of a notary deed; (b) documents proving the company's title to the premises in which its seat is located; (c) a confirmation from the administrator of the contributions into the company's registered capital confirming that each founder paid up at least 30% of his or her monetary capital contribution; (d) a confirmation from the relevant bank that the capital contributions are held in the company's special bank account for the registered capital; (e) documents on the company managers/executive.

- Register for taxes: According to the new resolution on January 1, 2013, the deadlines for registering with the Tax Office changed: income tax and general registration: 30 days from the registration of the Company by the Commercial Register; withholding tax and payroll tax registration: 8 days; VAT obligatory registration: within 15 days following the end of month in which the conditions are met or in certain cases within 15 days following the date when the company automatically becomes a VAT payer; VAT voluntary registration: submit the registration at any time. Upon submitting the application for income tax registration, the company receives a tax identification number (same number as for the VAT and the income tax).

- Register for social security (simultaneous with previous procedure): The company must register within 8 days as of the date when the first employee enters into work (the employee's and employer's registration are in practice be made at the same time). An 8-day notification deadline applies in case of certain changes occur.

- Register for health insurance (simultaneous with previous procedure): The same rules apply as for social security registration.

The formation of a new company in Czech Republic takes about 2 weeks.

As a rule, a Czech Limited Liability Company must have a registered office in the Czech Republic and in the course of the registration process it must prove its legal title to the office, for example rental agreement, or a consent of the owner. The registered office should not be a temporary address only for the purpose of company registration. The company does not have to keep records in Czech Republic. If the company chooses to keep records they can be kept anywhere in the world.

There are no statutory requirements for a company in Czech Republic to have a seal.

The redomiciliation of companies to or from Czech Republic is permitted.

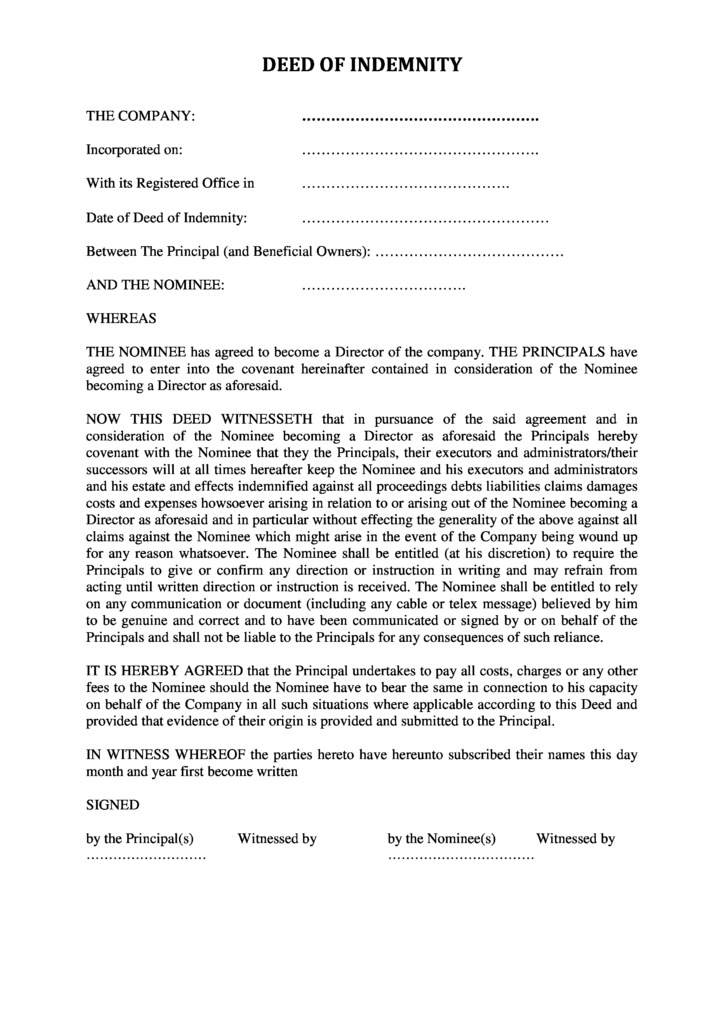

A Czech limited liability company does not have a board of directors. Its statutory body is made up of one or more executive officers. The law does not restrict their number. The executive officer is appointed by the general meeting, the supreme body of the company, or by the sole shareholder exercising powers of the general meeting. Each executive officer acts on behalf of the company independently unless the founder`s deed or the articles of association (if adopted) stipulate otherwise.

A director can be of any nationality. However, an non-EU national needs to comply with some visa requirements in order to be appointed as a director. A non-EU/EEA resident or citizen needs a criminal record check document from the country of citizenship and from the Czech Republic. (even though the client has probably never lived in the Czech Republic).

The names of directors do appear in public records.

Czech limited liability companies are not required to appoint a company secretary.

Each Czech company must have at least one shareholder. There is no restriction on the nationality or residency of the shareholders. The shareholders can be individuals and/or legal persons.

Shareholders’ meetings should take place at least once year.

The names of shareholders do appear on public records.

In 2021 a new provision concerning the ultimate beneficiaries (UBO) came into force in the Czech Republic: the registration of a company in the jurisdiction implies that the ultimate beneficiary of the legal entity will be identified and information about it will be publicly available.

All persons falling within the definition of ultimate beneficiary, or having the greatest influence, are considered beneficiaries. Similarly, any person who receives 25% or more of the profits or has influence over voting rights directly or indirectly can be considered a beneficiary.

Failure to provide information about the ultimate beneficiary when establishing a Czech company may result in a fine of up to CZK 500,000.

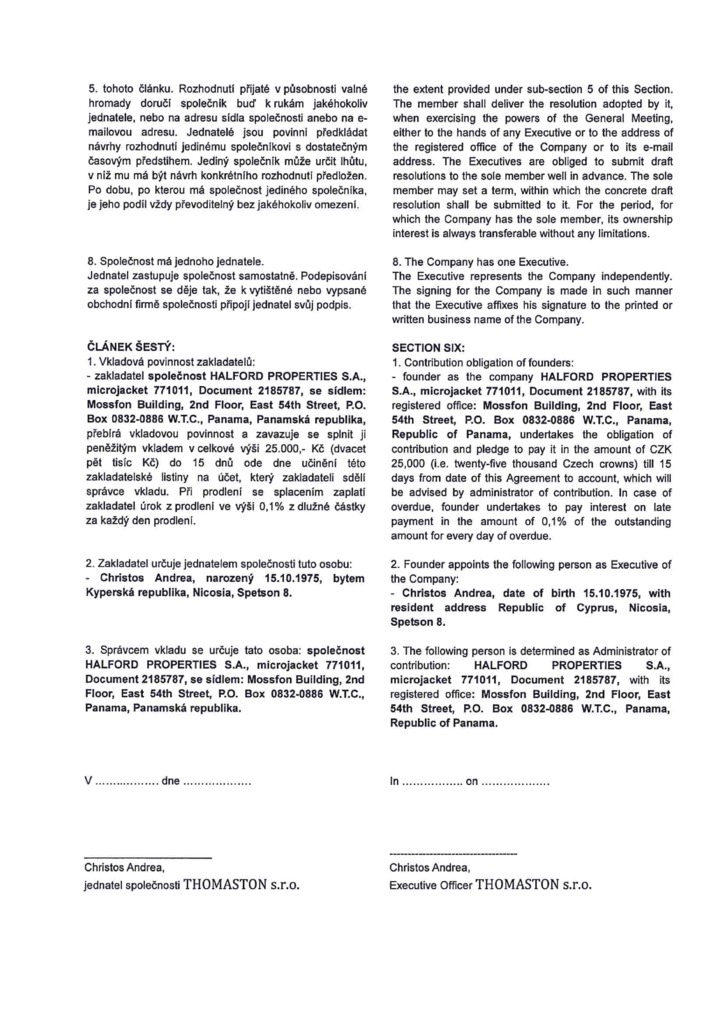

The minimum registered capital for an LLC is CZK 25,000 (approx. 1.000 EUR) and may consist of non-monetary (in-kind) and/or monetary contributions. The founding document must specify the non-monetary contribution and its value, which is assessed by an expert appraiser appointed by the court. The standard amount of share capital is CZK 25.000. The standard par value of shares is CZK 1 (0.04 EUR).

Bearer shares and shares with no par value are not permitted.

How much does it cost to open a company in Czech Republic?

The cost of opening a company in Czech Republic depends on the type of company to be registered and the type of activity you will be engaged in. The minimum package of services costs USD 8150 and includes: registration of the company on a turnkey basis, lease of the registered office for a year and secretarial services, payment of all necessary duties and fees, as well as apostilled translation of the constituent documents.

Can a foreigner open a company in Czech Republic?

Yes, a foreigner can open a company in the Czech Republic. The process of setting up a company in the Czech Republic is similar to the process in other countries and involves several steps, including choosing a company name, preparing the articles of association, registering the company with the Commercial Register, and obtaining the necessary licenses and permits.

What does SRO mean in Czech?

In the Czech Republic, the acronym "SRO" stands for "Společnost s ručením omezeným," which translates to "Limited Liability Company" in English. This type of company is a popular form of business organization in the Czech Republic and offers several advantages, including limited liability for the owners, ease of formation and management, and flexibility in terms of ownership and structure. The limited liability company is similar to the limited liability company in other countries, where the owners' personal liability is limited to the amount of their capital contribution. This type of company is well-suited for small and medium-sized businesses, and it can be owned by one or more individuals or companies. In the Czech Republic, limited liability companies must be registered with the Commercial Register and must comply with the laws and regulations that apply to companies in the country, including the Companies Act and the Accounting Act. The company must also have a registered office in the Czech Republic and must appoint a statutory representative, who is responsible for representing the company in its dealings with the authorities and with third parties.

How long does it take to set up a company in Czech Republic?

The process of setting up a new company in Czech Republic, from applying for registration to receiving a set of documents, is 4-5 weeks.