The Czech Republic emerged as a sovereign state in 1993 following the Velvet Revolution, peacefully dissolving its federation with Slovakia. Upon gaining independence and transitioning to a market economy, the country immediately pursued integration into the European community as an equal partner. This strategic vision led to Czechia's accession to NATO in 1999 and its subsequent EU membership in 2004.

Strategically positioned at the heart of Europe, the Czech Republic serves as an ideal logistics hub. This was demonstrated several years ago when Amazon established a regional distribution center in eastern Bohemia to service Czechia, Slovakia, and Austria simultaneously.

The country maintains robust industrial foundations dating back to the Austro-Hungarian era. Major taxpayers contributing significantly to the state budget include global players such as Škoda Auto, a.s., Avast Software s.r.o., and the renowned brewer Plzeňský Prazdroj, a.s. The defense industry also represents a strong economic sector, primarily export-oriented.

After joining the European Economic Area (EEA), Czechia - like most Eastern European countries transitioning to market economies - successfully completed its transformation and integrated into the pan-European market.

Czech corporate law derives from several key legislative instruments governing the establishment and operation of business entities. The primary regulatory document is the Act on Business Corporations (No. 90/2012 Coll.), which entered into force in 2014 and unified the legal framework for legal entities. This comprehensive statute regulates all corporate matters - from incorporation and governance to restructuring and dissolution.

The Commercial Code (No. 513/1991 Coll.) continues to play a significant role, maintaining jurisdiction over certain commercial matters including entrepreneurial obligations and specific contract types, despite partial supersession by the Corporations Act. For joint-stock companies, the Securities Act (No. 256/2004 Coll.) provides additional regulation governing share issuance, securities trading, and corporate governance requirements for public companies.

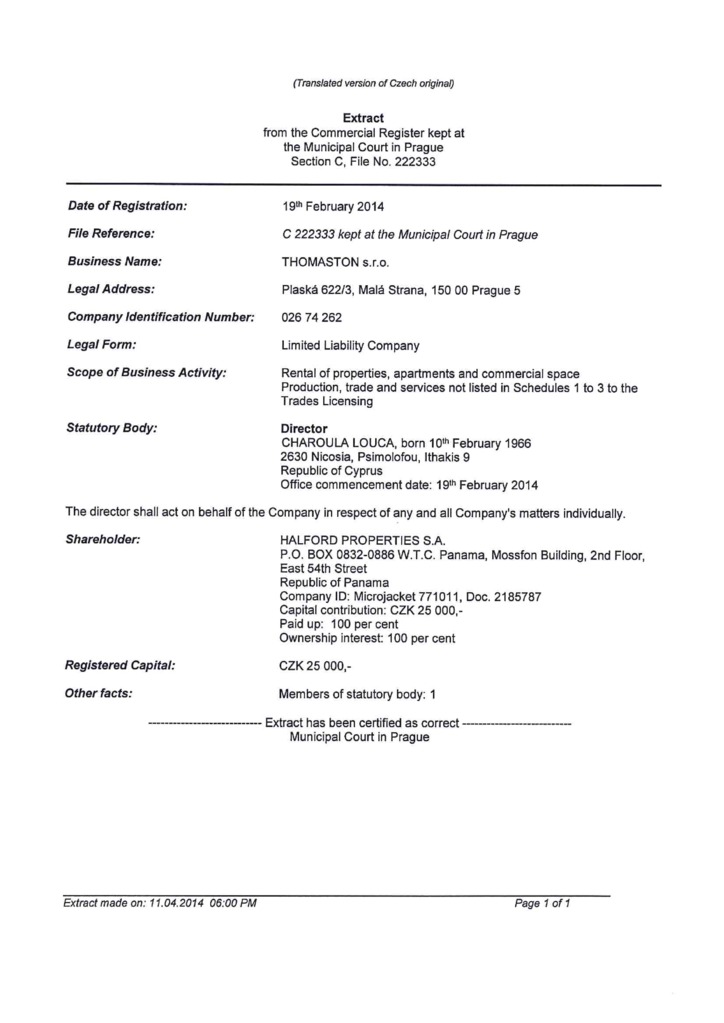

Entity registration follows the Public Registers Act (No. 304/2013 Coll.), which establishes procedures for maintaining the Commercial Register - the centralized database containing all registered entities. This official record includes essential corporate details such as founding members, management structure, registered capital, and ownership changes.

Taxation matters are governed by the Income Tax Act (No. 586/1992 Coll.) and VAT Act (No. 235/2004 Coll.). The former imposes a 19% corporate tax rate and establishes taxation rules for both resident and non-resident entities. The latter regulates value-added tax collection at the standard 21% rate, with reduced rates available for certain goods and services.

Investor and shareholder protections are ensured through the Capital Markets Act (No. 256/2004 Coll.) and Competition Protection Act (No. 143/2001 Coll.), which prevent financial market abuses and prohibit anti-competitive practices respectively.

The Czech corporate legal framework demonstrates exceptional transparency and full compliance with European standards, making the jurisdiction particularly attractive for business operations. However, when establishing a company, practitioners must consider not only primary legislation but also numerous implementing regulations governing specific aspects of commercial activity.

The Czech Republic cannot be classified as a low-tax jurisdiction. The country's tax burden aligns with standard European levels, though this wasn't always the case. Following the dissolution of Czechoslovakia in the 1990s, the corporate income tax rate (DPPO) initially ranged between 45% and 31%, eventually stabilizing at its current 19% rate in 2010.

The economic crisis triggered by the COVID-19 pandemic in 2020, later exacerbated by military conflict in Eastern Europe, has particularly impacted Central European nations including Czechia. For the second consecutive year, the country maintains the EU's highest food inflation rate. In response, Petr Fiala's (ODS) government has implemented stringent measures to reduce the state budget deficit, including plans to increase the corporate tax rate to 21% in 2024.

The Czech VAT system applies three distinct rates:

Taxable persons must apply the standard VAT rate to all transactions unless expressly authorized by law to use reduced rates. The application of reduced rates is strictly limited to specific goods and services enumerated in legislation.

The progressive taxation system features:

The principal forms of business organization in Czech republic are:

Registering a business in the Czech Republic requires careful consideration when choosing the legal form, as this determines the tax burden, level of liability, and growth prospects of the company. Entrepreneurs considering the Czech jurisdiction have several options available, each with its own characteristics.

The simplest and most popular form for small businesses. Suitable for freelancers, consultants, and small business owners.

Key advantages:

Key disadvantages:

Taxation:

Registration process:

Best for: Freelancers, small businesses, consultants

Often the optimal solution for more serious projects. Combines asset protection (founders are liable only up to the registered capital) with relatively simple management requirements.

Key advantages:

Key disadvantages:

Taxation:

Registration process:

Best for: Small and medium-sized businesses, startups, local enterprises

Requires significant capital (from CZK 2 000 000) and is more complex to administer but allows issuing shares and listing on the stock exchange. Suitable for large-scale projects with long-term prospects.

Key advantages:

Key disadvantages:

Taxation:

Registration process:

Best for: Large businesses, international companies, investment projects

The optimal legal form depends on the scale of the business, growth plans, and willingness to handle administrative requirements. The Czech Republic offers flexible conditions, including moderate taxes and access to EU markets, making it attractive for entrepreneurs. The right company structure helps minimize risks and optimize costs.

The most popular and widely used form is the limited liability company (S.R.O.).

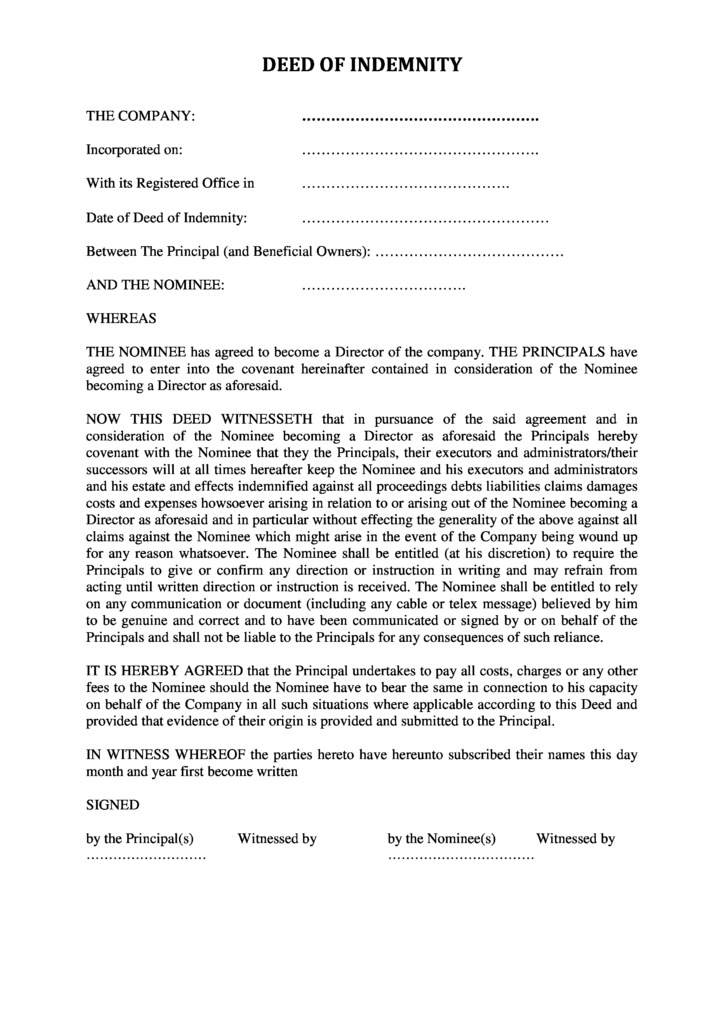

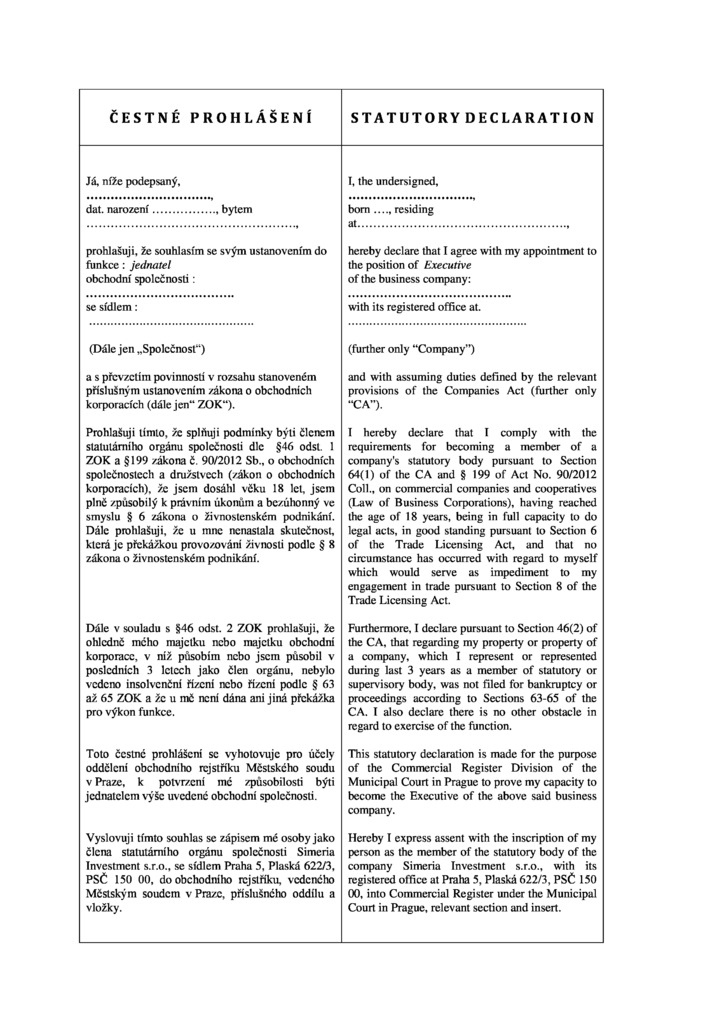

A Czech limited liability company does not have a board of directors. Its statutory body is made up of one or more executive officers. The law does not restrict their number. The executive officer is appointed by the general meeting, the supreme body of the company, or by the sole shareholder exercising powers of the general meeting. Each executive officer acts on behalf of the company independently unless the founder`s deed or the articles of association (if adopted) stipulate otherwise.

A director can be of any nationality. However, an non-EU national needs to comply with some visa requirements in order to be appointed as a director. A non-EU/EEA resident or citizen needs a criminal record check document from the country of citizenship and from the Czech Republic. (even though the client has probably never lived in the Czech Republic).

The names of directors do appear in public records.

Czech limited liability companies are not required to appoint a company secretary.

Each Czech company must have at least one shareholder. There is no restriction on the nationality or residency of the shareholders. The shareholders can be individuals and/or legal persons.

Shareholders’ meetings should take place at least once year.

The names of shareholders do appear on public records.

In 2021 a new provision concerning the ultimate beneficiaries (UBO) came into force in the Czech Republic: the registration of a company in the jurisdiction implies that the ultimate beneficiary of the legal entity will be identified and information about it will be publicly available.

All persons falling within the definition of ultimate beneficiary, or having the greatest influence, are considered beneficiaries. Similarly, any person who receives 25% or more of the profits or has influence over voting rights directly or indirectly can be considered a beneficiary.

Failure to provide information about the ultimate beneficiary when establishing a Czech company may result in a fine of up to CZK 500 000.

The minimum registered capital for an LLC is CZK 25 000 (~ EUR 1 000) and may consist of non-monetary (in-kind) and/or monetary contributions. The founding document must specify the non-monetary contribution and its value, which is assessed by an expert appraiser appointed by the court. The standard amount of share capital is CZK 25 000. The standard par value of shares is CZK 1 (EUR 0.04).

Bearer shares and shares with no par value are not permitted.

There are no statutory requirements for a company in Czech Republic to have a seal.

There is a range of requirements to the company name in Czech Republic:

The following steps are required to incorporate a Limited liability company in Czech Republic:

The formation of a new company in Czech Republic takes about 2 weeks. It is possible to purchase a ready-made Czech company.

The redomiciliation of companies to or from Czech Republic is permitted.

As a rule, a Czech Limited Liability Company must have a registered office in the Czech Republic and in the course of the registration process it must prove its legal title to the office, for example rental agreement, or a consent of the owner. The registered office should not be a temporary address only for the purpose of company registration. The company does not have to keep records in Czech Republic. If the company chooses to keep records they can be kept anywhere in the world.

For a company to operate in the Czech Republic, opening a corporate bank account is required to deposit the company's registered capital. The minimum registered capital amounts to CZK 1. An amount of up to CZK 20 000 may be deposited in cash during the company's registration before a notary public, thereby expediting the registration process while postponing the opening of a bank account to a later date.

To open an account, the company's articles of association or notarized foundation agreement must be submitted to the bank. After depositing the registered capital, the bank will issue a confirmation of payment. This document subsequently serves as one of the company's founding documents and must be submitted when filing the application for company registration with the Commercial Register.

In the Czech Republic, conducting many types of commercial activities requires obtaining special permits and licenses. The Czech licensing system is characterized by transparency and clear regulations, though requirements vary significantly depending on the specific type of activity.

The primary regulatory body for licensing is the Ministry of Industry and Trade of the Czech Republic. However, for certain sectors (financial services, healthcare, education), licensing is handled by specialized ministries and authorities. The licensing process typically involves submitting an application with supporting documentation, verification of the applicant's compliance with established requirements, and issuance of the permit.

Most business licenses are granted indefinitely, though some sectors (such as gambling or pharmaceuticals) require periodic renewals. Key factors in the application review process include professional qualifications of founders and employees, availability of necessary infrastructure, and compliance with sanitary, environmental and other special requirements.

Particular attention should be paid to financial sector licensing. Banking operations, insurance, and investment fund management require licenses from the Czech National Bank - the country's primary financial regulator. Obtaining such licenses may take six months to a year and requires submission of detailed business plans, proof of capital adequacy, and information about beneficial owners.

Businesses in food service, alcohol or tobacco retail must obtain a "živnostenský list" (trade license) from local trade licensing authorities, typically processed within 30 days.

Construction companies face additional requirements - beyond general business licenses, they need specific construction work permits from the Ministry of Regional Development. Similar specialized permits are required for medical practice, education, transportation and other business activities.

It's important to note that some activities (like alcohol production or private education) may require additional local government approvals beyond the basic license. Businesses must also maintain regular reporting to licensing authorities and promptly notify them of any operational changes.

Given the complexity and diversity of licensing requirements, thorough analysis of necessary permits is strongly recommended before starting business operations in the Czech Republic. Professional legal consultants can not only identify required licenses but also prepare complete documentation packages, significantly speeding up the approval process and minimizing rejection risks.

Czech legislation establishes clear requirements for accounting and tax reporting by all registered companies. Unlike offshore jurisdictions, Czech businesses must regularly submit financial statements and pay taxes on time, requiring understanding of local tax laws and corporate regulations.

The primary tax obligation for resident companies is corporate income tax, calculated at 21% of net profit. The tax base equals total annual income minus documented business expenses. Czech tax residents pay tax on worldwide income, while non-residents pay only on Czech-source income. The tax period generally follows the calendar year, though individual schedules may be established under certain conditions. Tax returns must be filed within three months after the reporting period ends, with payment due upon filing. The system also requires advance payments (2 or 4 annually) based on prior year tax liabilities.

Special attention should be given to financial reporting requirements. Czech companies meeting certain criteria must undergo mandatory audits. These thresholds include: assets exceeding CZK 40 000 000, annual turnover over CZK 80 000 000, or average employment exceeding 50 staff. These requirements apply to joint-stock companies and other legal entities alike. Audited financial statements must be submitted to the Commercial Register by March 31 and become publicly available. Reports contain comprehensive company information: registration details, management and governance changes, capital and shareholder data, plus share issuance/transfer records.

VAT registration becomes mandatory when: annual turnover exceeds CZK 1 000 000 (~ EUR 40 000), or EU purchases exceed CZK 326 000 annually. Some operations require registration regardless of turnover. The standard VAT rate is 21%, with monthly or quarterly reporting periods depending on business scale. Returns must be filed within 25 days after each period. Notably, voluntary VAT registration is permitted even without meeting thresholds, which may benefit certain business models.

Given the complexity and multifaceted nature of Czech tax law coupled with strict corporate reporting requirements, obtaining qualified professional advice during business planning is essential.

PriceEUR 6 750

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Business Registry incorporation fee

PriceEUR 4 580

including registered address and registered agent, NOT including Compliance fee

PriceEUR 275

DHL or TNT, at cost of a Courier Service

PriceEUR 2 120

Paid-up “nominee director” set includes the following documents

PriceEUR 1 090

Paid-up “nominee shareholder” set includes the following documents

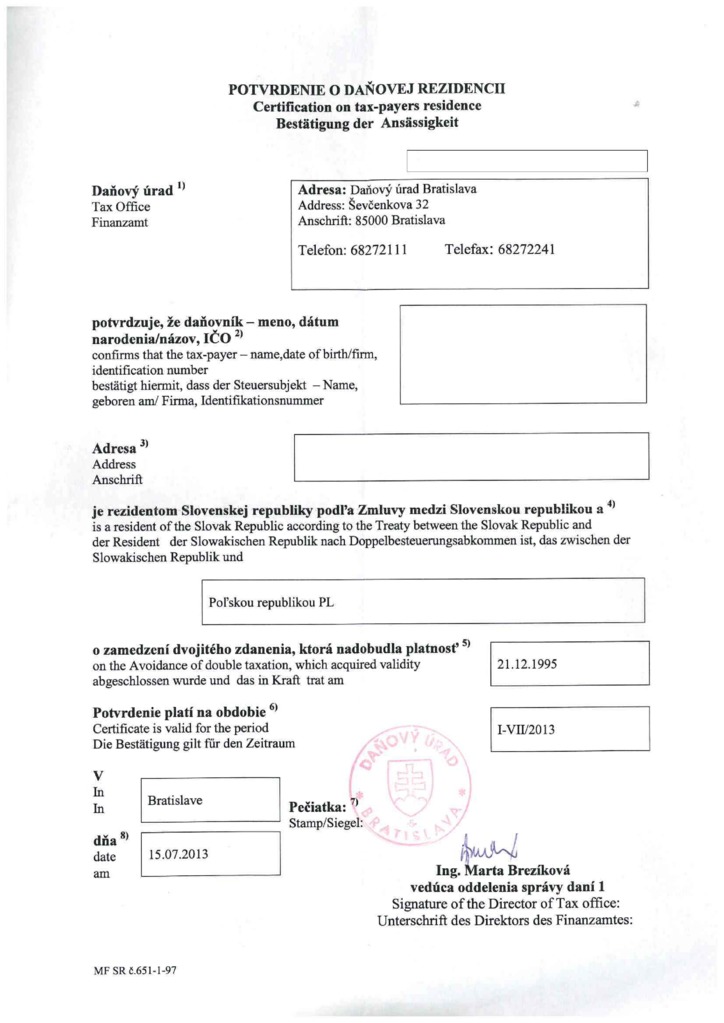

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

PriceEUR 385

simple company structure with only 1 physical person

PriceEUR 165

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

PriceEUR 220

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

PriceEUR 495

PriceEUR 110