Ireland is a common law jurisdiction based on English common law.

The basic law of Ireland is Constitution of 1937.

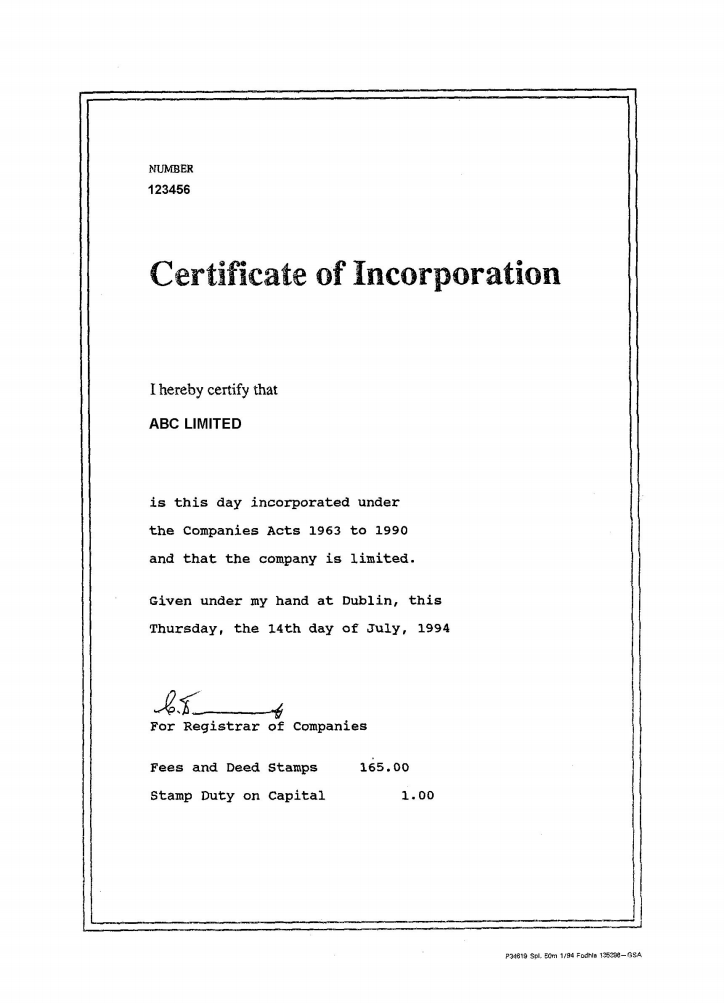

Companies in Ireland are regulated by Companies Act, 1963.

The principal forms of business organization in Ireland are:

The most common structure is the private company limited by shares.

There is a range of requirements to the company name in Ireland:

The following steps are required to incorporate a Limited liability company in Ireland:

Check and reserve a company name online: you may check and reserve a company name with the Companies Registration Office in electronic form. A company name can be reserved for a period up to 28 days.

File necessary materials with the Companies Registration Office (CRO): A founder may register a company at the Companies Registration Office (CRO) by three methods:

To access the first two systems, to the company founder must apply to the CRO for an access number and have the memorandum and articles of association approved in advance. Usually only professional agencies use the expedited systems.

Necessary documents for limited companies:

Forms can be downloaded from the CRO Web site. For all methods, a CRO Form A1 must be submitted with details of the company name, the first election of directors and secretary, and the subscribers to the memorandum and articles of association; the authorized and issued share capital; and the registered office and the details of the location in the state where the central administration and the main company activities are proposed to be undertaken. The memorandum and articles of association, signed by the subscriber shareholders, will also be submitted to the CRO.

As of April 2006 professional incorporators do not have to reregister the preapproved memorandum and articles of association. When using the CORE system only those pages that are company specific of the pre-approved memorandum and articles of association need be submitted with an application to incorporate a company.

A registration fee of EUR 100 is charged for each model memorandum and articles of association registered with the Office.

Get a company seal: In addition to getting a company seal, the company must keep the statutory registers for the directors and shareholders.

Register for corporation tax, social insurance (PAYE/PRSI) and VAT with the Revenue Commissioners: To register for corporation and VAT taxes and for social insurance (PAYE / PRSI) with the Revenue Commissioners, the company must file Form TR2. The tax identification number is needed only when the company must pay year-end taxes. Upon entering form data into the Commissioners database, the company is immediately registered for PAYE / PRSI. However, VAT registration requires an additional 5–10 working days.

The formation of a new company in Ireland takes about 10 days.

Applying for a local bank account depends on the activities to be carried on by Irish Company. Generally, if payments are to be made to the Company locally or if the Company is to make payments locally it might be best to have a local bank account. It will be necessary to provide the Bank with information for each of the company’s directors i.e. copy of passport/driving licence and a copy of a utility bill. It may be prudent to have a local bank account to facilitate Revenue Commissioner refunds and payments.

An Irish company must have a registered office in Ireland and must include its company name and registered office in all business letters, correspondence, notices, negotiable instruments and letters of credit.

The registered office of a company is that to which CRO correspondence and all formal legal notices addressed to the company will be sent. The registered office can be anywhere in the State.

It is most important that the company's registered office is kept up-to-date, so that the company will receive all correspondence. The original registered office is entered on the form A1 to incorporate the company. The registered office can be changed electronically, via the CORE website, free of charge.

All company books, including register of members, minutes of meetings, register of directors and secretaries, seal and records must be kept at the registered office.

All companies incorporated in Ireland must have a company seal. This is often referred to as the ‘common seal’ and will be a device with two opposing metal plates on which the name of the company will be engraved which, when pressed together on a sheet of paper, will leave the name of the company clearly embossed thereon. Irish law requires that every company must have its name legibly engraved on its seal. Common seal is not to be confused with a rubber stamp with the name of the company. Any contract required by law to be in writing and under seal is made by a company in writing under its common seal.

The redomiciliation of companies to or from Ireland is permitted.

Every Irish company is required by law to have at least one Director. The first Directors are nominated by the founding Members and are identified in the Form A1. They will remain in office until the first AGM and may be re-elected.

Directors can only be individuals. At least one of the directors is required to be resident in a member State of the EEA. The requirement to have at least one resident director from a member State does not apply to any company which for the time being holds a bond, in the prescribed form, in force to the value of EUR 25,394.76 and which provides that in the event of a failure by the company to pay the whole or part of -

there shall become payable under the bond a sum of money for the purpose of same being applied in discharge of the whole or part of the company's liability in respect of any such fine or penalty.

The bond must have a minimum period of validity of two years, commencing no earlier than the occurrence of the event giving rise to the requirement for the bond.

The Board must meet at least once a year and each Director must be given at least 7 days notice of the meeting. Board meetings can be held inside or outside Ireland but to establish tax residence in Ireland, regular (at least quarterly) meetings should be held in Ireland. It is possible to hold Board Meetings by telephone/electronic communication but for tax purposes it is recommended that this is not done.

Every Irish company is required by law to have a Company Secretary. The Company Secretary is appointed by the Board of Directors. The secretary may be one of the directors of the company. A body corporate may act as secretary to another company.

Companies have a statutory duty to ensure that the Company Secretary is a person who appears to them to have the requisite knowledge and experience to discharge the functions of a Company Secretary. The first secretary of the company must be named in the documents filed with the Companies Registration Office.

All Irish companies must have at least one shareholder at the time of incorporation. The maximum number of shareholders in a private limited company is ninety nine.

Corporate shareholders are allowed. There is no restriction on the nationality or residency of the shareholders.

The names of shareholders do appear on public records.

All companies must every year hold an annual general meeting. Not more than fifteen months should elapse between AGM's. General Meetings can be held inside or outside Ireland.

From 2019, Irish companies and other legal entities registered in the country must create their own internal Beneficiary Registers.

Individuals who are the beneficiaries of the companies must inform the management of the companies themselves.

The Beneficiary Registry contains the following information: Name, date of birth; nationality; address of residence; and a statement of the nature and extent of each beneficiary's ownership and control.

In addition, the Register contains the date the person was added as a beneficiary and the date the person ceased to be a beneficiary.

The information is accessible to:

Share capital of an Irish company should be denominated in Euros. If the company is to be single member the minimum can be as small as EUR 0.01, but more usually EUR 1.00. If it is a multiple member company, a private company’s minimum is EUR 0.02, but again more usually EUR 2.00.

Usually, the standard issued share capital is EUR 100 with a nominal value of EUR 1.00 each.

Bearer shares and shares with no par value are not allowed.

Price5 390 EUR

including incorporation tax, state registry fee, NOT including Compliance fee

Priceincluding

Stamp Duty and Companies Registration Office incorporation fee

Price3 490 EUR

including registered address and registered agent, NOT including Compliance fee

Price250 EUR

DHL or TNT, at cost of a Courier Service

Priceform 970 EUR

Pricefrom 3 500 USD

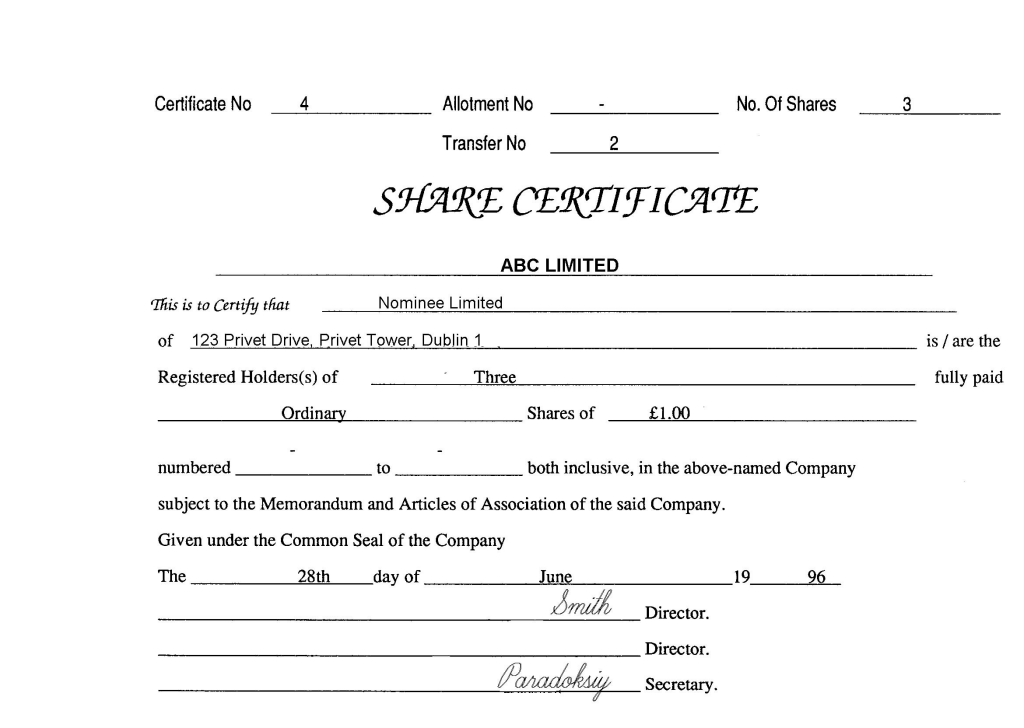

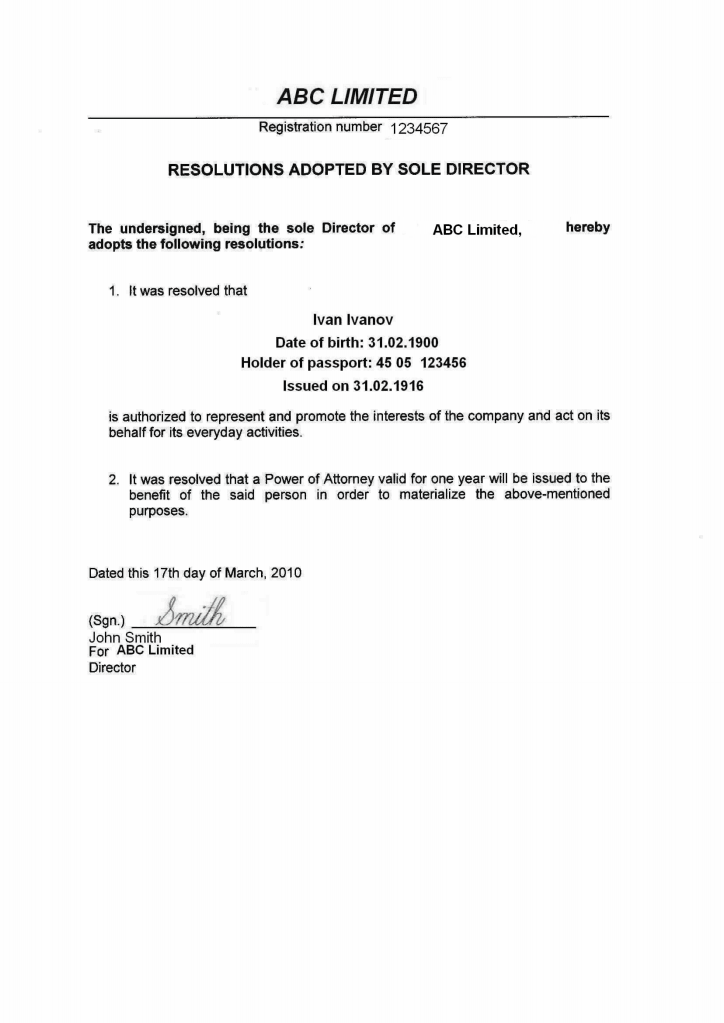

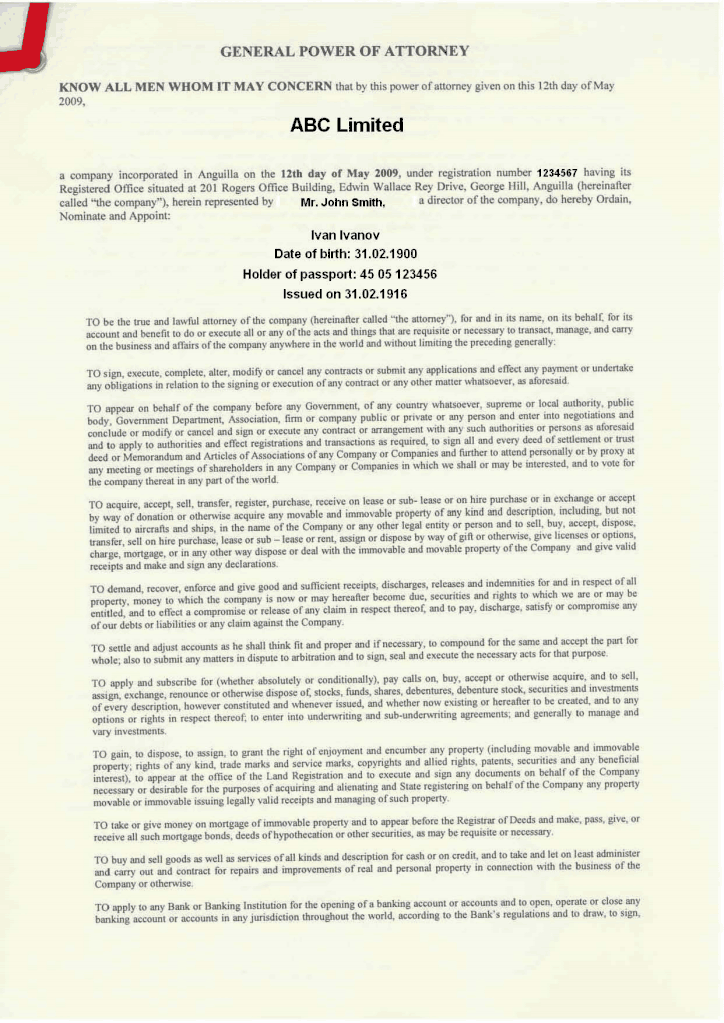

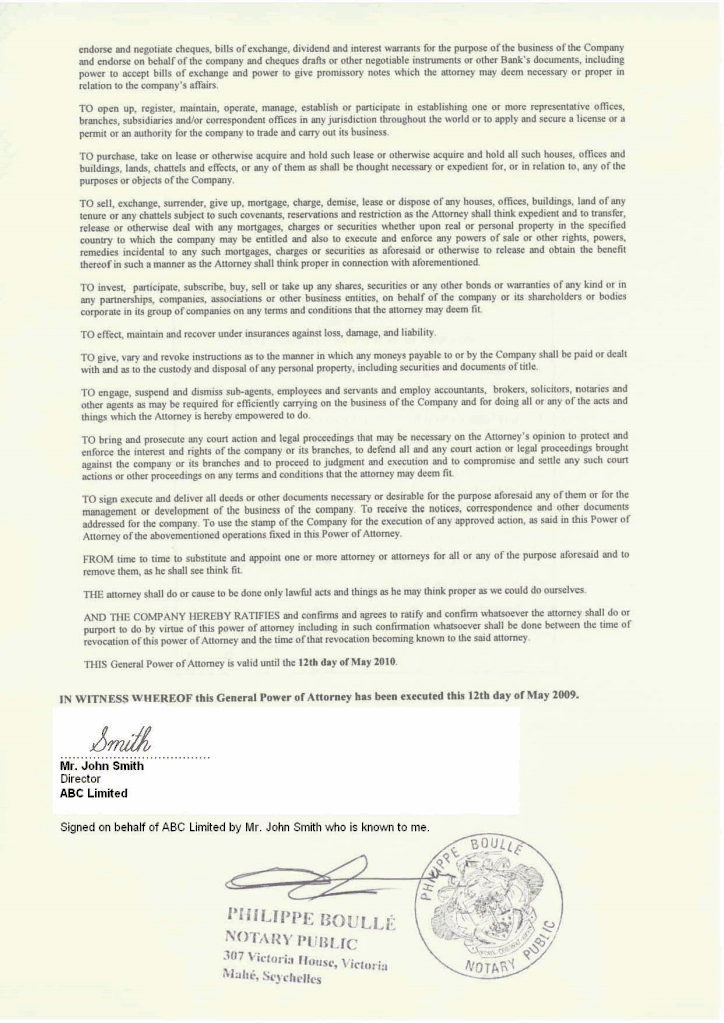

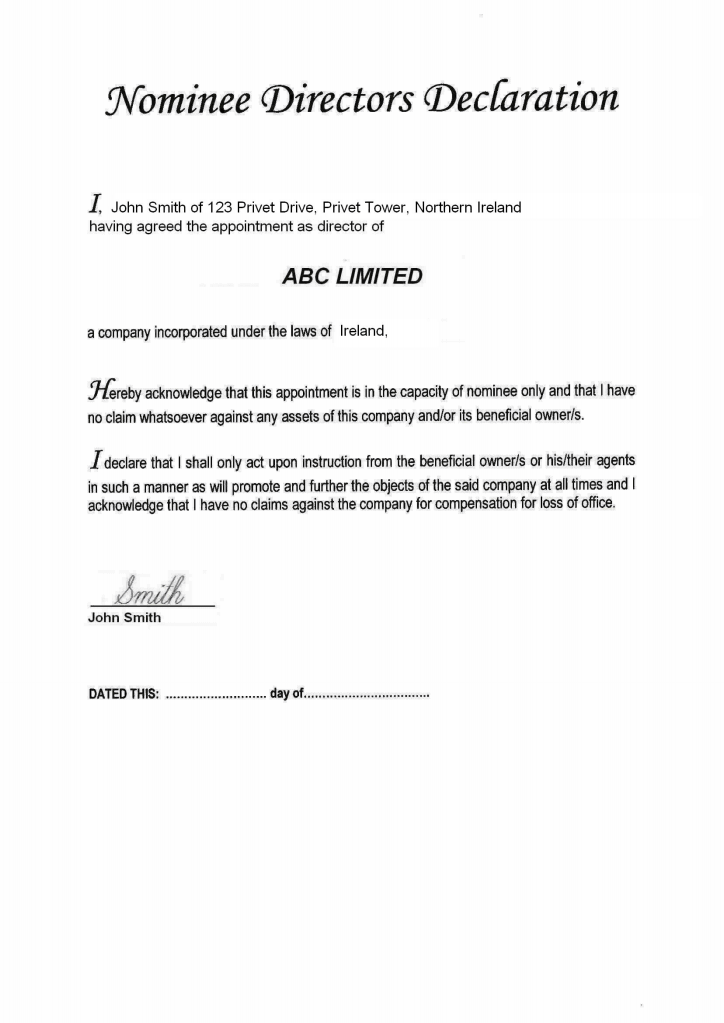

Paid-up “nominee director” set includes the following documents

Paid-up “nominee shareholder” set includes the following documents

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD