There are several stages of registration of S.R.L. in Italy:

The filing procedure “Comunicazione Unica” to register the company at:

Tax Agency; Registrar of Companies at Chamber of Commerce;Social Security Authorities.

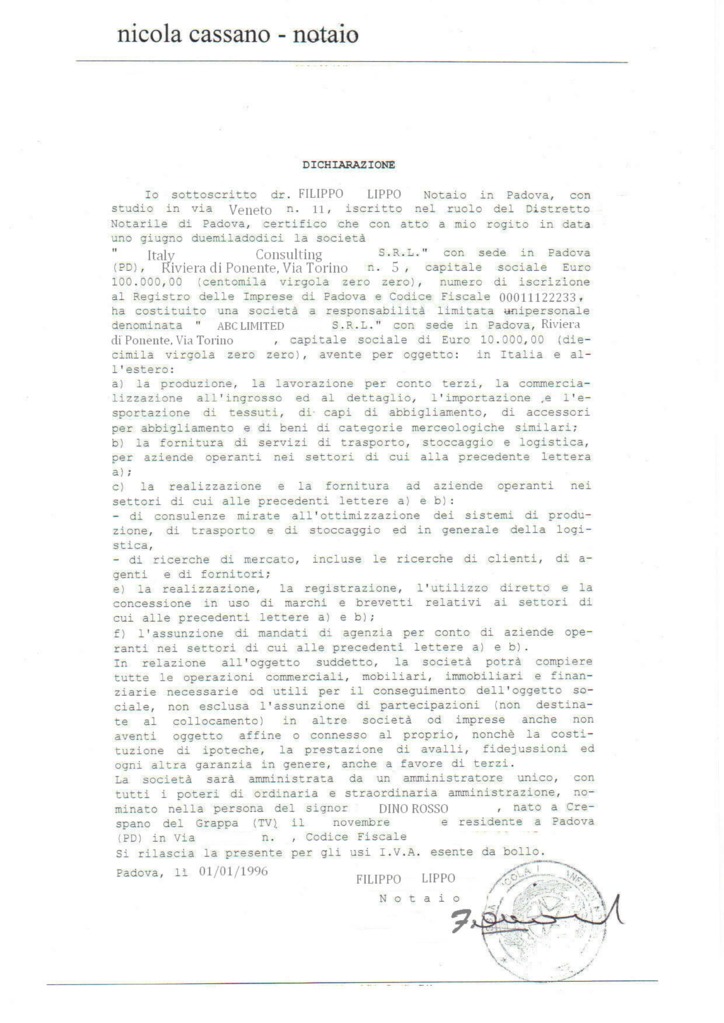

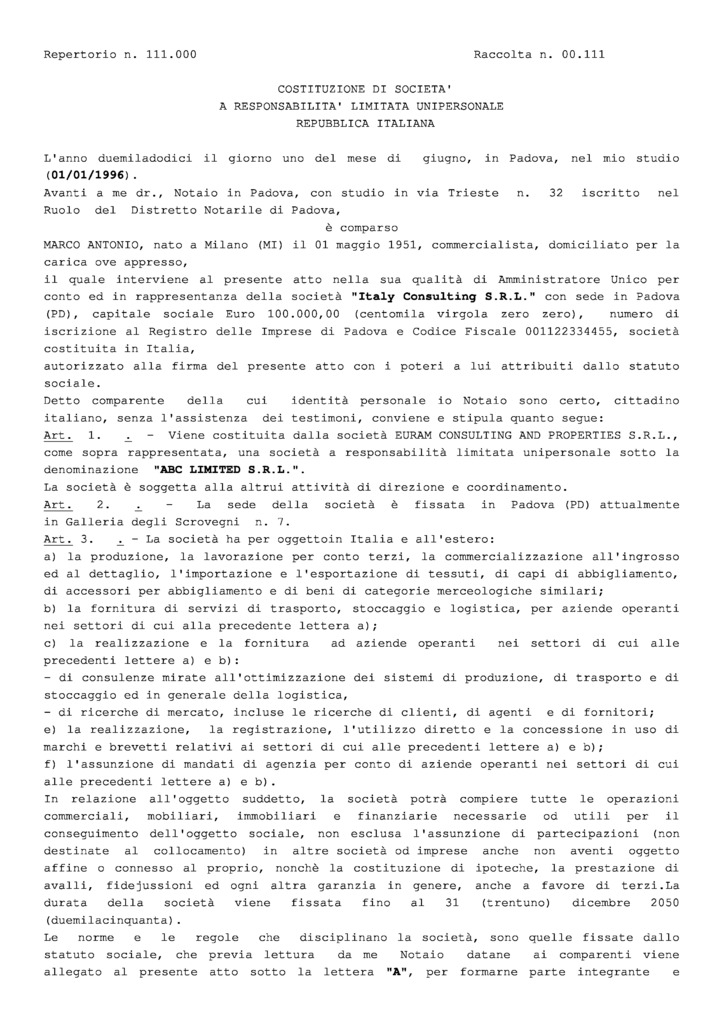

S.R.L. is incorporated through a public act with the attendance of a Notary.

Memorandum of Association should show:

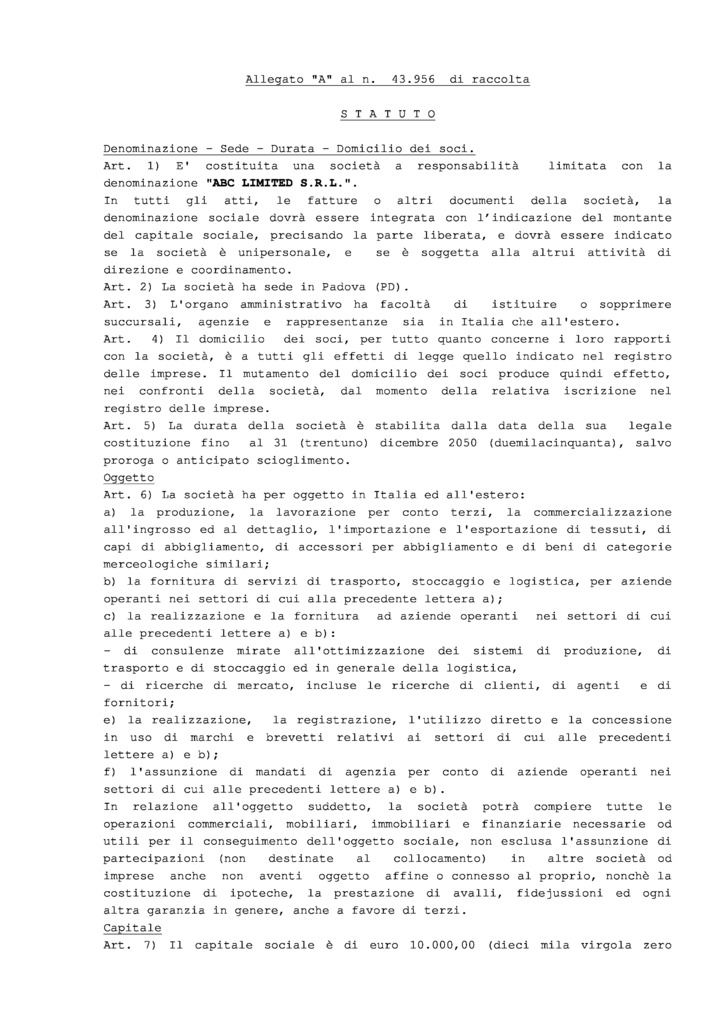

With the Memorandum of Association, Founders approve the Articles of Association (Statuto).

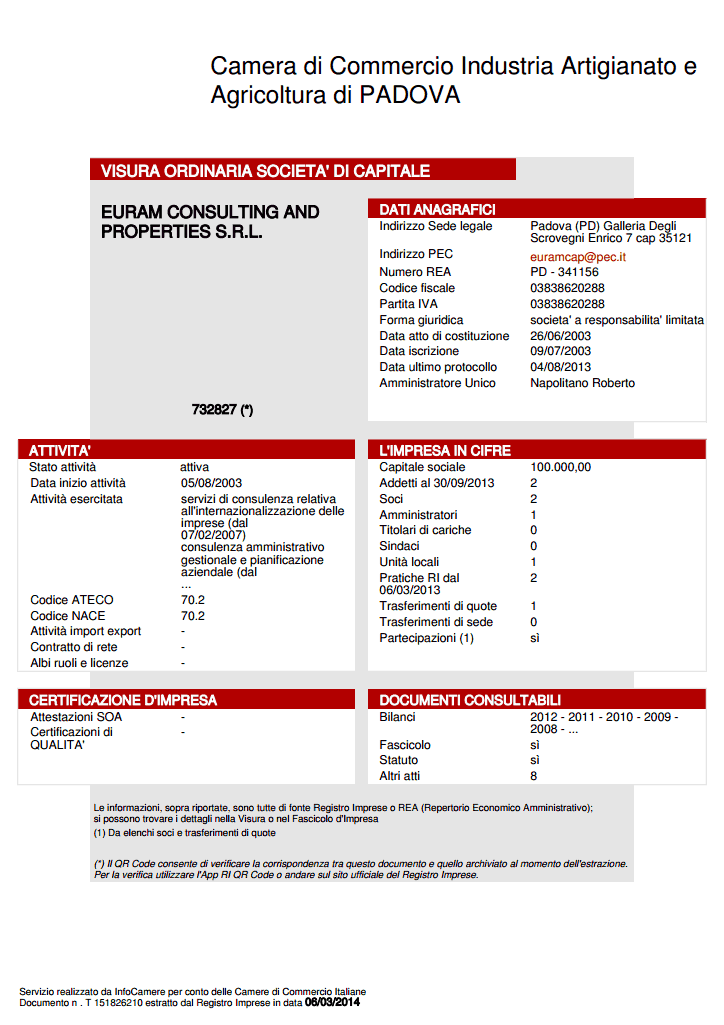

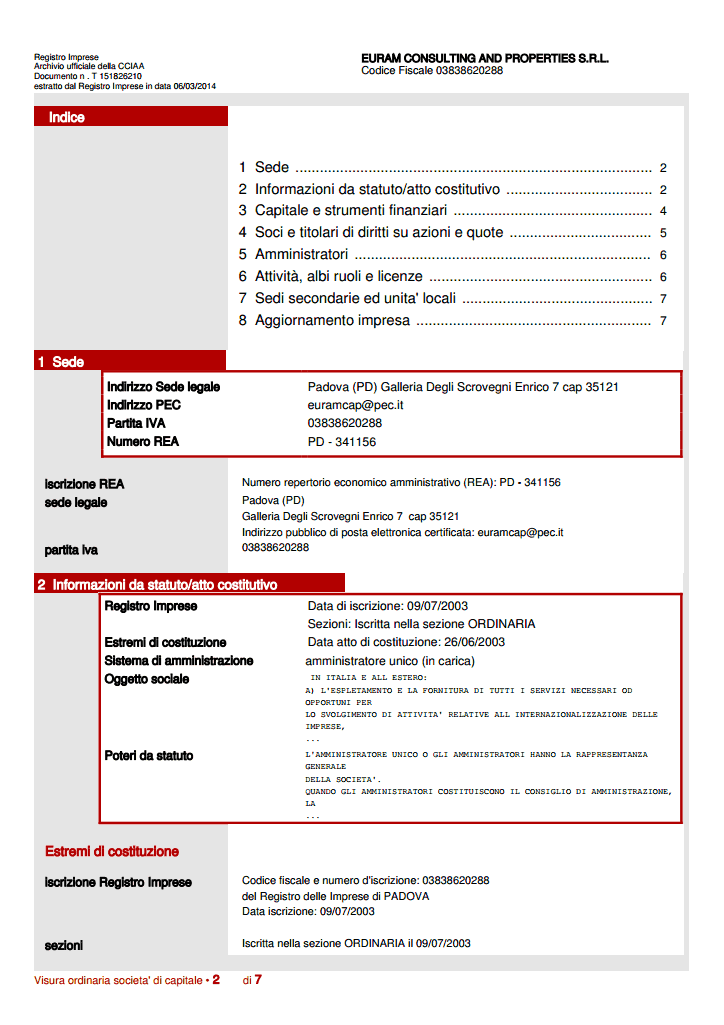

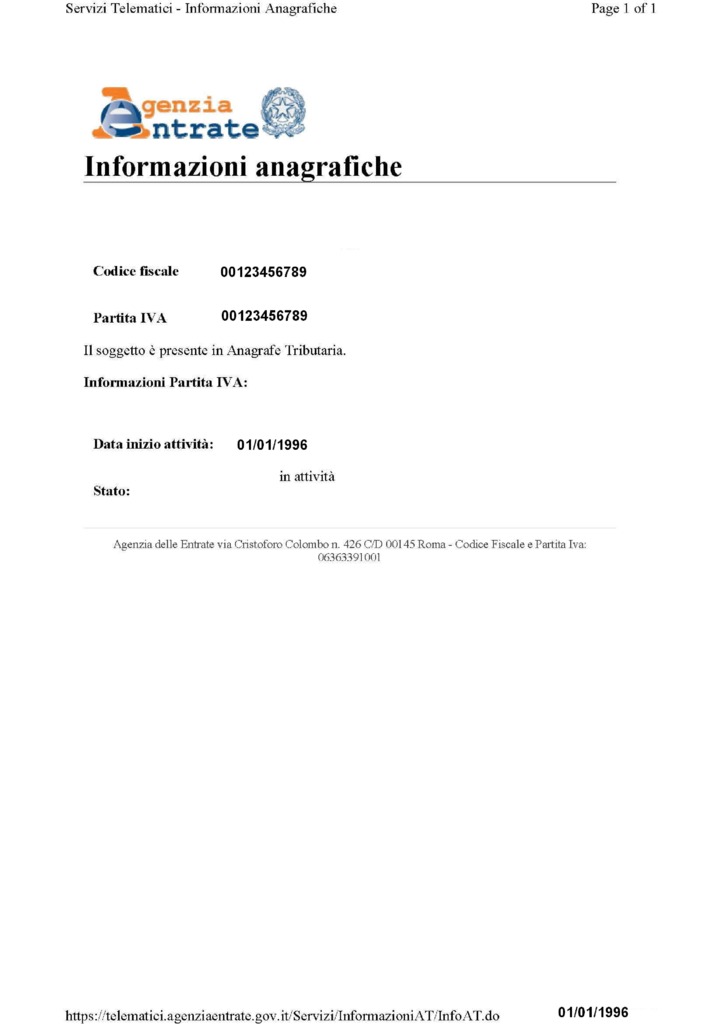

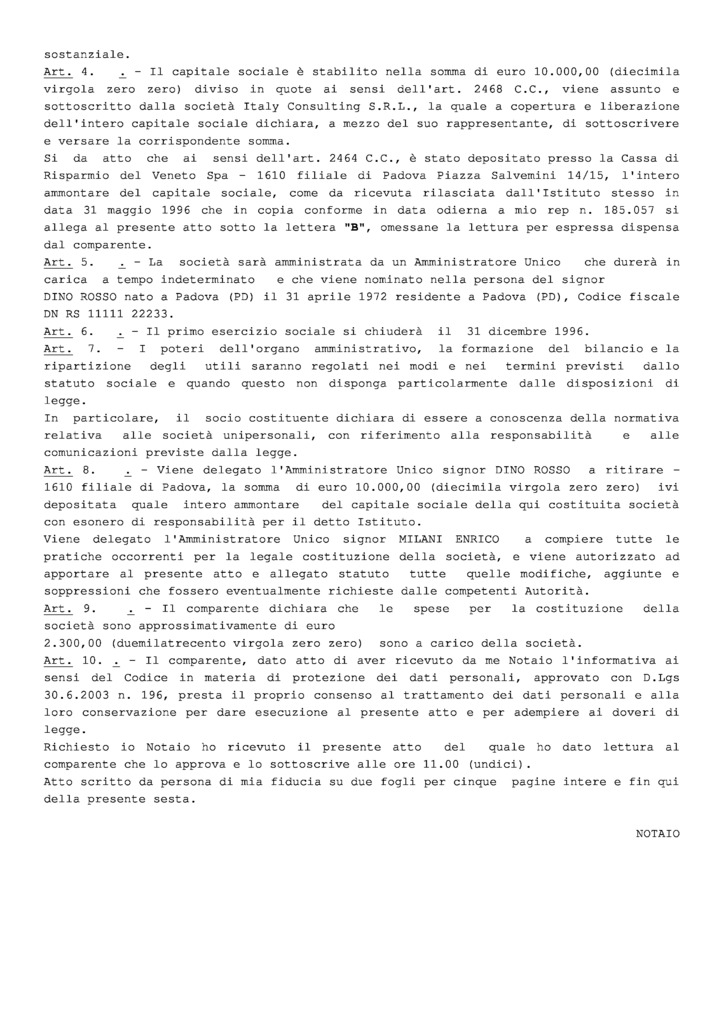

The Memorandum od Association is registered at the Chamber of Commerce and Tax Agency. Registration of Company normally takes from one week up to ten days. Company then receives a VAT number that corresponds to its Tax Code as well.

Before Incorporation, 25% of share capital should be deposited at a bank in a special account. This money is available after registration at Chamber of Commerce is achieved.

Certain rules are applied for company name in Italy:

Company suffix may be as following: Srl.

In Italy there are following variants of leasing of an office for S.R.L:

To register S.R.L. it is enough to have a virtual office in Italy.

Leased Offices

Leasing is a traditional method of acquiring office space in Italy.

Serviced Offices

Apart from the standard lease this service may include: inclusive servicing:

The volume of services depends on the needs of a client.

Virtual Offices

«Virtual office» is a term used to describe shared office services in Italy, which typically includes:

To establish a virtual office, all participants must have an internet-ready computer or laptop, which meets software needs and has access to the necessary professional/industry requirements.

There are no requirements for the Companies of Italy to have a seal.

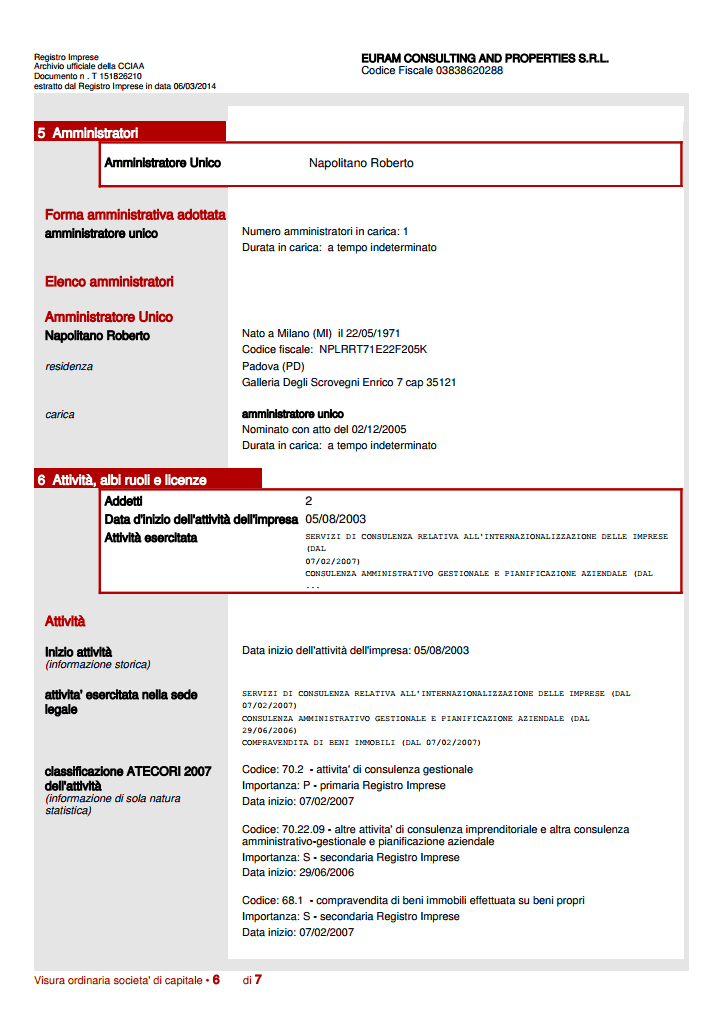

The minimum number of Directors in SRL is one. Corporate directors are permissible.

There is no residency requirements, but it is recommended to appoint at least one Member of the Board of Directors with residence in Italy.

There are no rules for frequency of meetings of the Board of Directors. However the accounts should be yearly approved by the Board. For the validity of the resolutions of the Board of Directors, during the meetings is required the majority of the Directors, unless Articles of Association (Statuto) requires a qualified majority.

Powers of directors:

The Directors have the ordinary and extraordinary powers for company management.

First of all, Directors are responsible for company management.

Shareholders may appoint:

Company secretary is not required; thereby there are no special requirements for secretary's residency, and qualification.

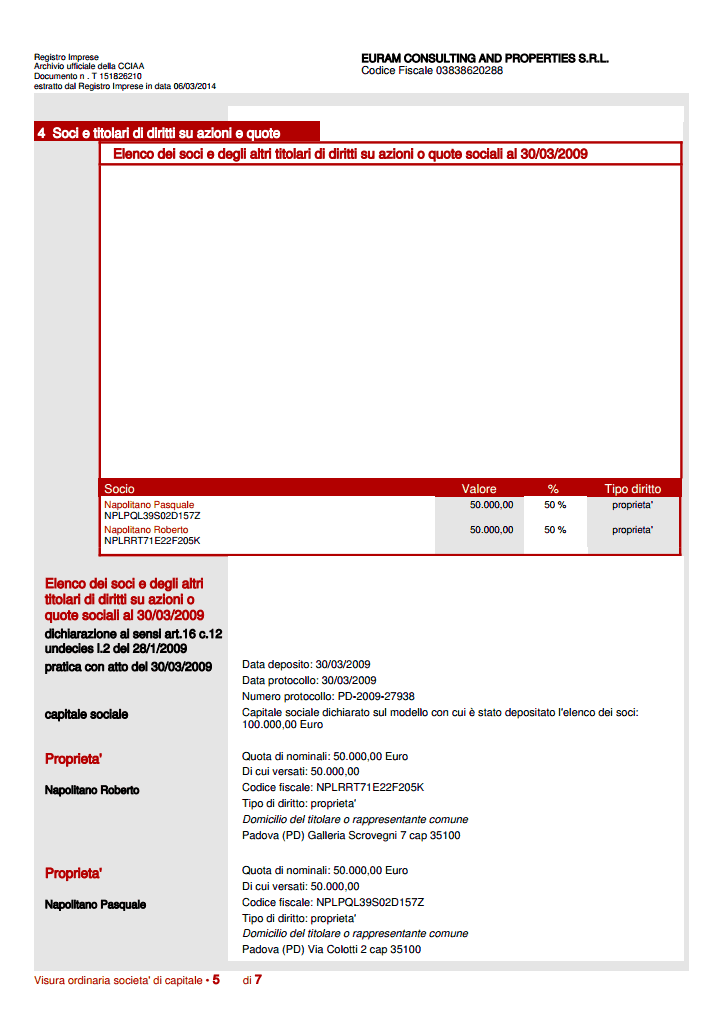

The minimum number of Shareholders in Italian companies is one, which can be either a person or a company.

Corporate shareholders are permissible. It is an advantage that there are no residency requirements for shareholders.

The records of Shareholders are publicly accessible.

There are two different kinds of meetings of Shareholders in Italy:

1. Ordinary Meetings;

2. Extraordinary Meetings.

Ordinary Meetings should take place at least once a year, for accounts approval, not later than 120 days after the closing of business year.

Decisions are taken with the majority of the votes of the attendants. Another condition for validity of decision is the attendance of shareholders representing at least 50 % of share capital.

Meetings take place at legal address unless M.o.A. allows to call the Meeting in another place or to establish other procedures (mailing, videoconference, etc.).

Ordinary Meetings are called by Directors. Secretary of the Meeting is appointed by Meeting.

The following matters can be discussed at the Ordinary Meeting:

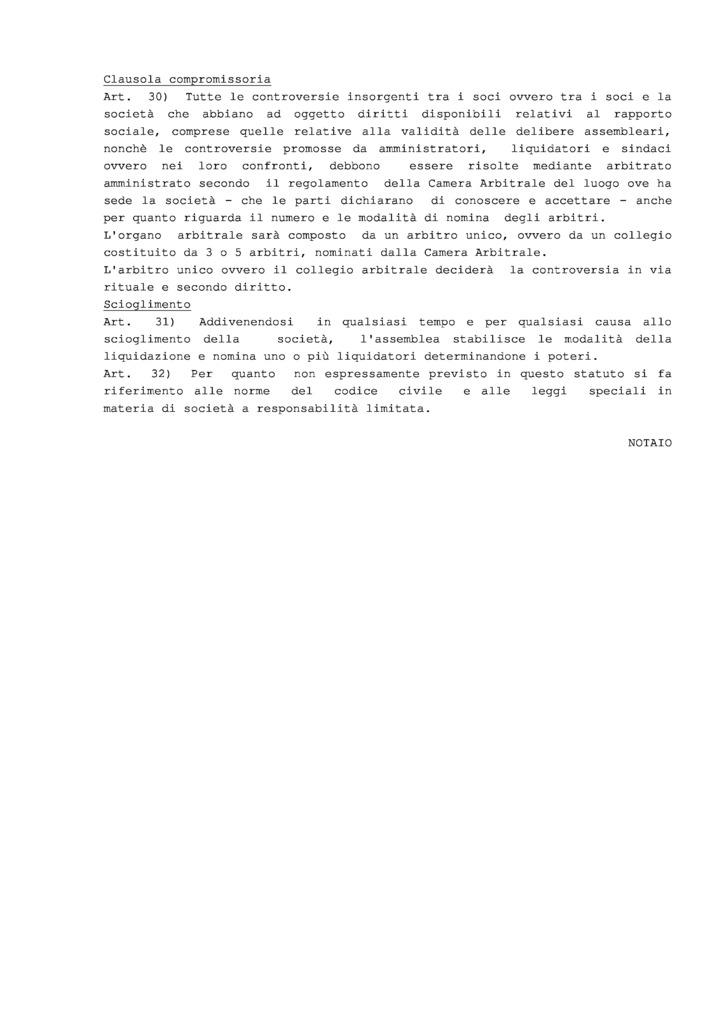

Extraordinary Meetings take place with the attendance of Notary and are obligatory whenever the agenda involves changes of the Memorandum of Association.

Extraordinary Meetings are called by Directors.

Extraordinary meeting is obligatory by law for following decisions:

The list of shareholders of each S.r.l. is registered in the register of the Chamber of Commerce and is public. However, shares may be held through a Fiduciary Company. In this case Fiduciary company will appear as shareholder in the extract (Visura) of Chamber of Commerce. Fiduciary agreement is neutral for tax purposes and may be disclosed to State authorities in case of investigations.

The beneficial owner of a company in Italy is disclosed to accountants (auditors) and banks.

Italy has approved the introduction of the Beneficiary Register in 2019. And the first information was submitted to the Registry in spring 2021.

Any changes to the information must also be submitted within 30 days.

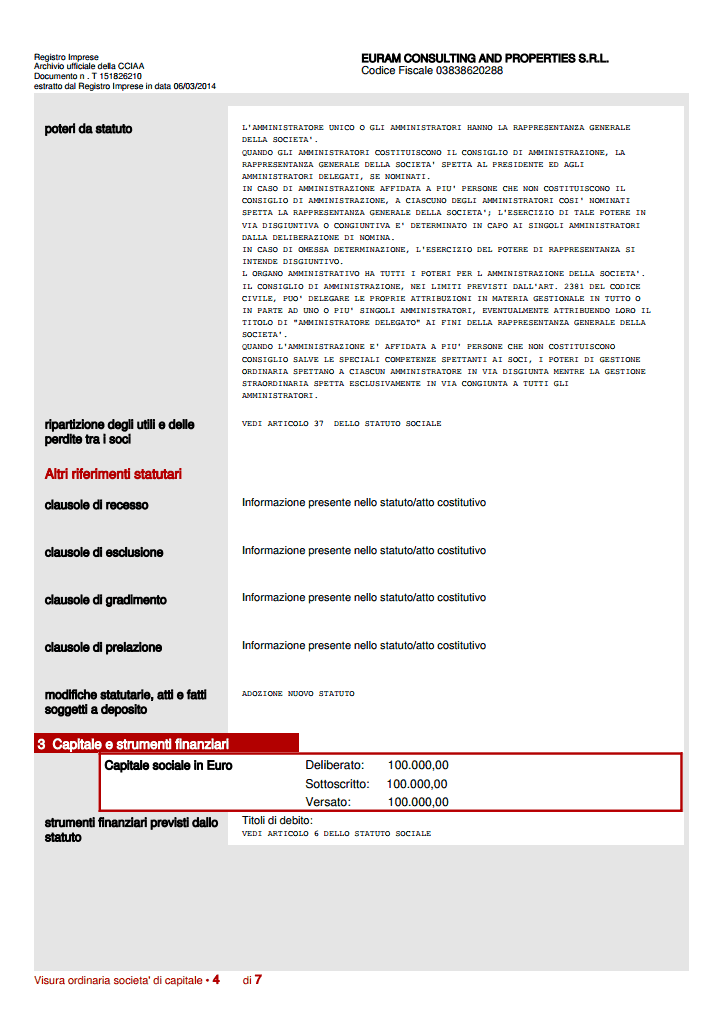

The standard currency of Shares and Share Capital is Euro (EUR).

The minimum authorized share capital is 1 EUR, the minimum issued share capital is 1 EUR for S.r.l.s., while the limit for the formation of “standard” S.r.l. remains € 10.000. Nevertheless, the amount of share capital could decrease under the aforementioned limit, without any consequences in the end, the only difference between “ordinary” S.r.l. and S.r.l.s is the fact that S.r.l., even with share capital < € 10.000, has to set aside in reserve the 5% of € 10.000.

Shares of no par value and bearer shares are not allowed.

Collegio Sindacale performs surveillance activity which is mainly focused on the control of company activity and of its consistency with law and includes also a check of accounts. In accordance with the article 2403 of the Italian Civil Code the Board of Controllers performs the following functions:

In accordance with the article 2403, the appointment of the Board is obligatory for S.R.L. in following cases:

- total assets: 4,400,000 EUR;

- revenues: 8,800,000 EUR;

- average number of employees: 50.

A recent reform, introduced by law 183/2011, provided companies of smaller size, with the opportunity to appoint a “Single Controller” (Sindaco Unico) instead of a Board.

Single Controller may be appointed only by S.r.l. For this type of company a Single Controller is to be considered as the general rule: if the M.o.a. does not establish the obligation to appoint a Board, then a Single Controller may be appointed.

First scheme

1. Management Board and Supervisory Board

2. Management Board has same functions of Board of Directors.

Supervisory Board absorbs functions of Collegio Sindacale and some functions of Meeting of Shareholders:

Second scheme

1. Board of Directors and Internal Committee.

The cost for incorporation of the company (S.R.L.) in Italy, including the corporate legal service for the second year

Price7 650 EUR

including Annual Duties for Chamber of Commerce for first year, NOT including Compliance fee

Priceincluded

Price1 210 EUR

including registered address and registered agent, NOT including Compliance fee

Pricefrom 1 200 EUR

Price3 850 EUR

(depends on the volume of duties)

(depends on the volume)

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR