There are two forms of Limited Liability Company in Sweden:

The advantage of the Limited Liability Company in Sweden is that it provides the best financial protection for a private person. There is a clear dividing line between the business enterprise and its owners.

The influence of the Shareholders in a Limited Liability Company is in relation to their shares.

It is also one of the most favorable forms from the point of view of taxation. A Limited Liability Company may have a split financial year, which can facilitate financial planning with regard of taxes, credits, salaries and interest.

The vast majority of international companies choose to set up a Private Limited Liability Company. Private LLC cannot offer its shares to the public on the stock exchange or any other organized market.

Minimum share capital is 50,000 SEK (approx. 6,110 EUR).

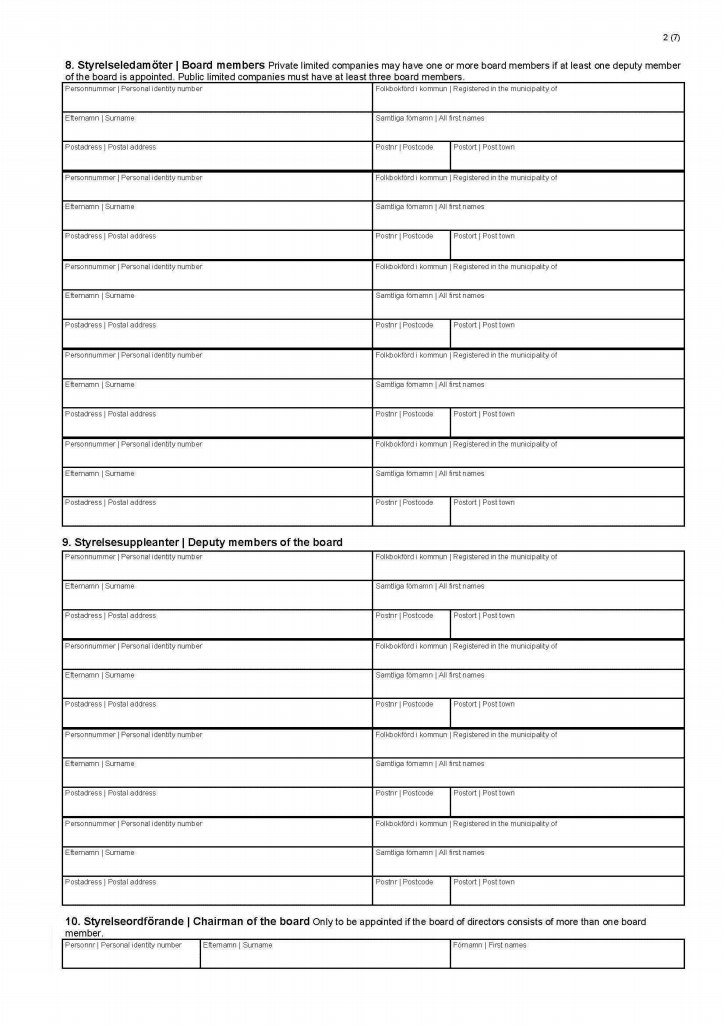

The Board of Directors of a Private Limited Liability Company must have at least one Director + one Deputy Director. If there are three Directors or more, it is not necessary to appoint a Deputy Director. The number of Directors and Deputy Directors must be stated in the Articles of Association (Bolagsordning).

|

|

Private LLC

|

Public LLC

|

|

Company name

|

AB

|

AB (publ.)

|

|

Purpose

|

Suitable for even the smallest companies

|

Standard format for large companies

|

|

Minimum Share Capital

|

The minimum share capital required is 50,000 SEK (approx. 6,110 EUR)

|

The minimum share capital required is 500,000 SEK (approx. 61,100 EUR)

|

|

Shares

|

The shares cannot be sold on the stock market; cannot be offered to public

|

The shares can be issued on the stock market; can be offered to public

|

|

Board of Directors

|

one Director plus one Deputy Director

|

At least three members; optional amount of Deputy members

|

|

Chairman of the Board

|

Can be appointed if the Board consists of more than one member

|

Compulsory

|

|

Managing Director

|

Optional (may be the same person as Chairman of the Board)|

|

Compulsory (not the same person as Chairman of the Board)

|

There are several stages of registration of a Private Limited Liability Company in Sweden:

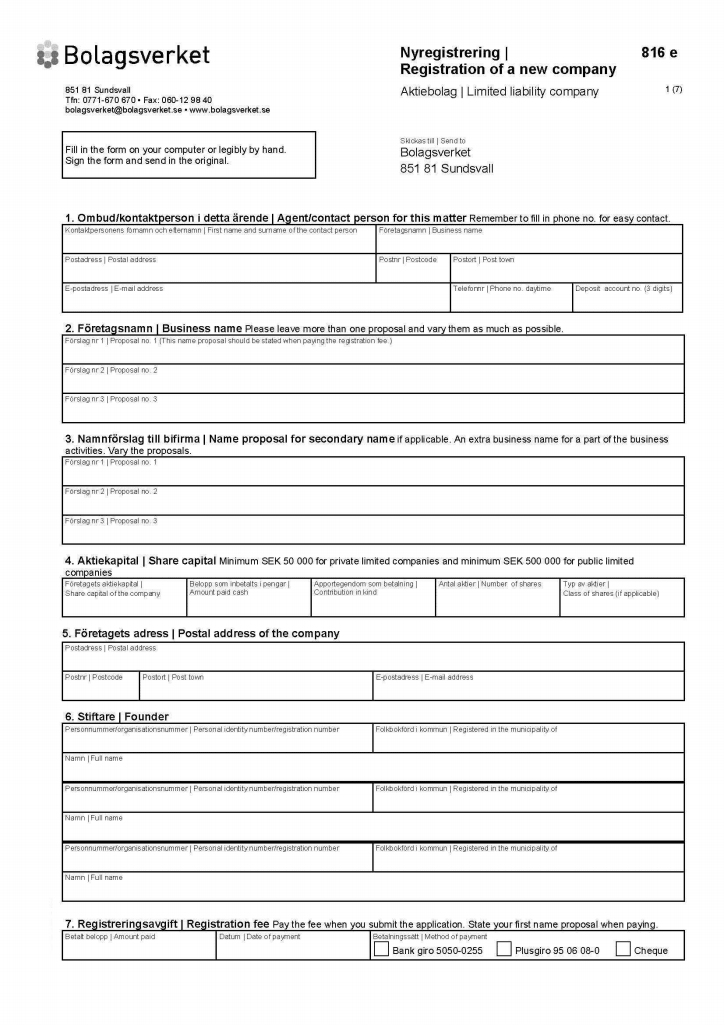

A Limited Liability Company must be registered with the Swedish Companies Registration Office. A Limited Liability Company only becomes a legal person when it has been registered with the Swedish Companies Registration Office. Registration provides nationwide protection of the company name.

When starting a Limited Liability Company, you will need to apply for F-tax and VAT registration and register as an employer.

First of all, it is necessary to fill the Application form for registration to the Swedish Companies Registration Office (Bolagsverket) to form your Private LLC in Sweden with the enclosed set of documents. The document must be in Swedish.

Thereby to form your LLC in Sweden the following documents are required:

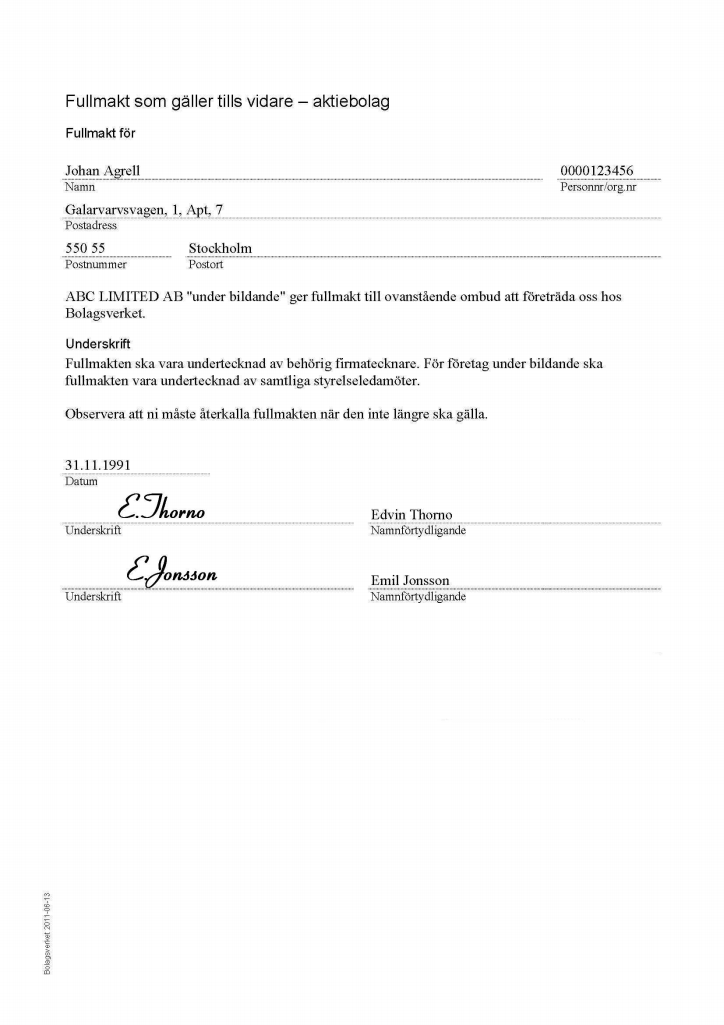

The registration procedure of a Company can be performed by a legal representative appointed by Power of Attorney without visit of the Client to Sweden.

In the case when a non-resident company be the Shareholder of the Company to be incorporated it is also required:

All documents are to be provided in the original or as copies duly authenticated and certified by a Lawyer or a Public Notary using his/her seal or stamp.

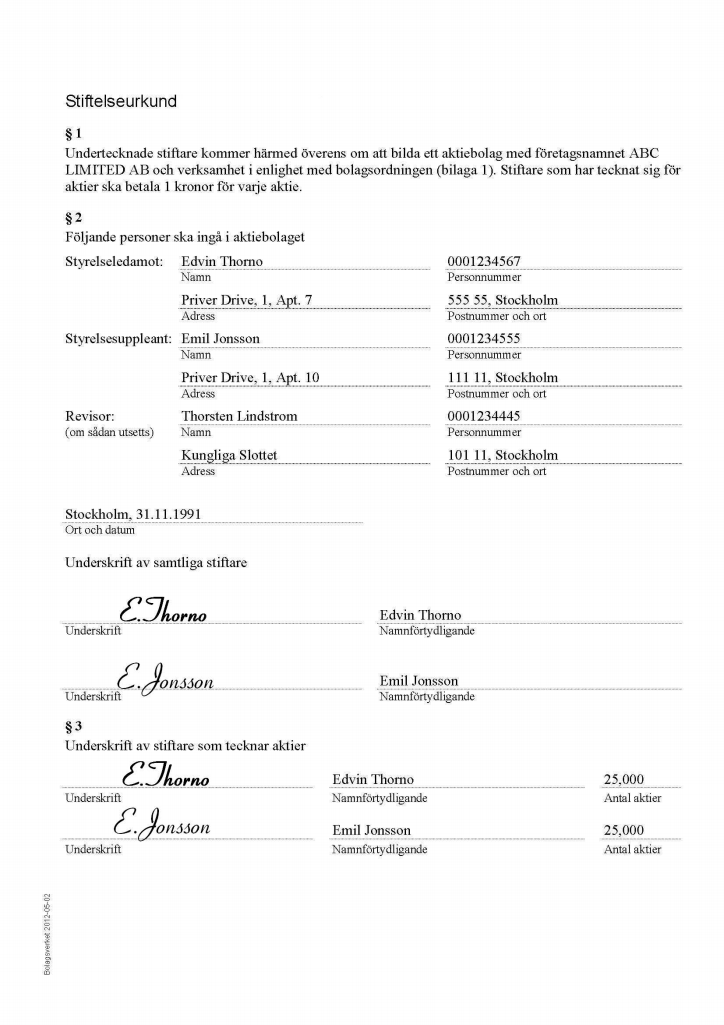

The founders draw up and sign a Memorandum of Association. Only the founders are permitted to subscribe to the shares. Private LLC may not offer its shares to the public.

The Memorandum of Association must contain the following information:

The company is formed when the Memorandum of Association has been signed by all founders; however the Limited Liability Company becomes a legal entity on the date on which it is registered at the Swedish Companies Registration Office.

The Articles of Association of Private LLC must contain the following information:

After the registration with the Swedish Companies Registration Office it is necessary to register with the Swedish Tax Agency (Skatteverket) before starting a business:

The registration procedure of a Company can be performed by a legal representative appointed by Power of Attorney.

Swedish Tax Agency is responsible for administration of taxes in Sweden. All physical and legal persons have their own tax account at the Swedish Tax Agency where all tax payments are recorded.

Starting a business, it is necessary to apply to the Swedish Tax Agency for an F-tax certificate which signifies that you are an entrepreneur who is responsible for paying your own taxes and contributions. When clients engage you they are sure that they will not be liable for your taxes and contributions.

In the cases when taxes are not declared or paid the F-certificate may be withdrawn by the Swedish Tax Agency.

The fact that the Limited Liability Company has F-tax certificate should be indicated in different types of business documents. In practice, there is usually the note on company’s invoices – “F-tax certificate holder”.

VAT is paid by natural or legal persons selling goods or services which are subject to VAT in Sweden.

Having registered as an employer, the Company pays the employer contribution. The Swedish Tax Agency issues a registration certificate; it also automatically sends the documents for reporting and paying employer contributions and deduct tax for employees.

There are two forms of employment in Sweden:

Employment is always indefinite unless otherwise agreed. It means that if the employment is temporary it must be clear from a written employment contract.

The easiest and most common way to set up a Private LLC in Sweden is to use a “shelf company”. It gives quick access to a new, pre-registered LLC that has not previously traded or been engaged in commercial activity.

There are several stages of purchasing of a shelf company in Sweden:

The company name of Private LLC is registered with the Swedish Companies Registration Office to ensure it will not be taken by another business.

Certain rules are applied for company name:

All company names must include the Swedish word for Limited Liability Company – "aktiebolag", or its abbreviated form, "AB".

The registered business name of a Private LLC in Sweden is protected throughout the country.

The possibility of using one or another company name can be checked at the website of the Swedish Companies Registration Office. You can get an approval or rejection in a day.

It is possible to use such words as “Group”, “Financial”, “International”, “Limited”, and “Ltd.” in the company name.

In most cases there are no formal requirements regarding the design and layout of business documents.

Agreements may be concluded verbally or in written form. Some agreements, such as property transfers and collective agreements have to be in writing.

In practice, many agreements are concluded verbally. However, a written agreement reduces the risk of the parties interpreting the content of the agreement differently.

There are special requirements regarding the content of a LLC's business documents and website. They should provide with the following information:

In Sweden it is required to have a local registered office for the companies. Thereby, LLC must have its legal address in Sweden.

There are no requirements for Swedish companies concerning the Seal.

The redomiciliation of companies is permissible to all countries within European Union.

The minimum number of Directors in Swedish Private LLC is one plus one deputy.

Corporate Directors are not permissible. There are publicly accessible records of Directors in Sweden and information is also disclosed to local agent. The minimum number Meetings of Directors is one meeting in a year.

A Limited Liability Company is formed by one or more founders, who must meet certain qualification requirements.

A founder must be:

The Managing Director of a Swedish Limited Liability Company must be resident in the EEA. However, the Registration Office may grant an exemption from this requirement.

If none of the representatives of the company is resident in Sweden, the Board of Directors shall appoint a person resident in Sweden authorised to accept service on behalf of the company.

A majority of the Directors, and the Managing Director, must be resident in the EEA, unless an exception is granted by the Registration Office.

The Board of Directors is in charge of the organization and management of the company.

The Board of Directors is in charge of:

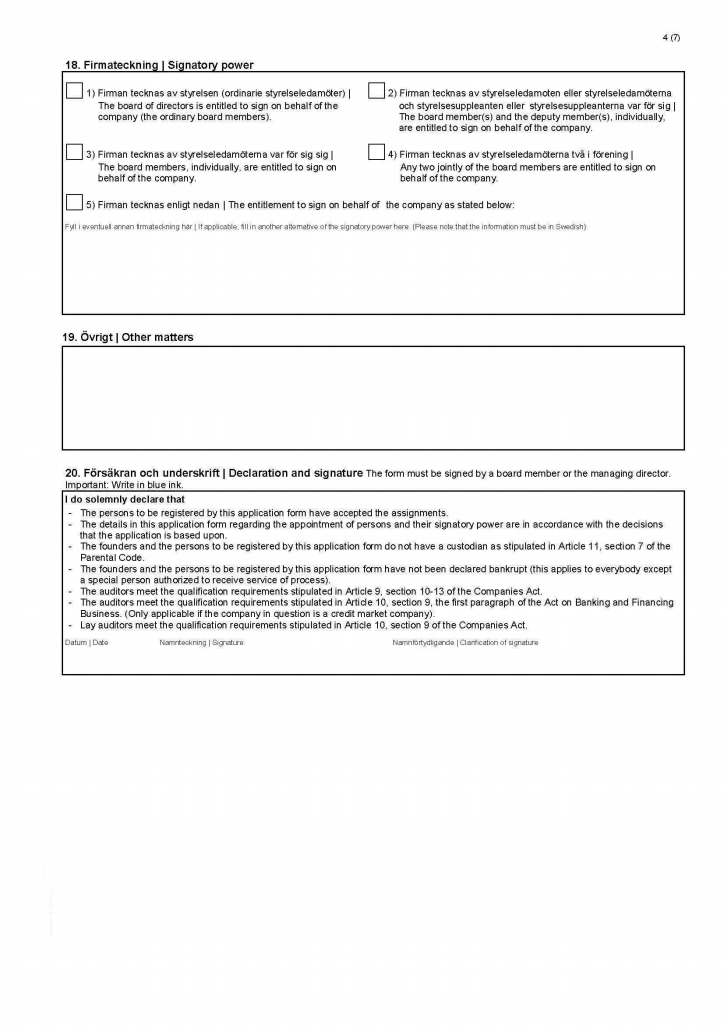

The Board convenes the General Meeting of Shareholders and decides who is authorized to represent the Company, i.e. power to sign. If no individual is registered as having power to sign, the Board is entitled to sign on the Company’s behalf, more than half of the Board members must sign jointly.

There are no requirements for Sweden Companies concerning the Secretary. The appointment of a company Secretary is optional.

The minimum number of Shareholders in Sweden companies is one. It is an advantage that there are residency requirements for Shareholders. Shareholders may reside in any country. Corporate Shareholders are permissible. There are publicly accessible records of Shareholders; the information is also disclosed to local agent. The minimum number of meetings of Shareholders is one meeting in a year.

The Board of Directors must draw up a Share Register and a List of Shareholders. The Share Register is a public document and must be kept available to the public at the Company’s Office.

There are no restrictions on the number, or the nationality, of Shareholders.

In 2017, a new law came into force in Sweden that obliges legal entities to provide information about their beneficiaries to the Swedish Company Registration Service (Bolagsverket). The law implements the Fourth EU Anti-Money Laundering Directive into Swedish law.

Legal entities are obliged to obtain reliable information about the beneficiaries and the nature and extent of the actual owner's interest in the legal entity and then transmit it to Bolagsverket.

Legal entities must also inform Bolagsverket immediately if there are any changes.

If incomplete notification, incorrect information, failure to provide notice on time, or failure to provide notice of beneficial ownership at all, Bolagsverket may impose a fine on the legal entity with an order to provide notice. If the notice is then not provided, the fine may be increased.

The standard currency of Shares and Share capital of the Company is Swedish krona. The minimum authorized share capital for Private Limited Liability Company is 50,000 SEK (approx. 6,110 EUR); the minimum issued share capital is 50,000 SEK (approx. 6,110 EUR); the standard minimum paid up capital is 50,000 SEK (approx. 6,110 EUR). Apart from that, the owners have no personal responsibility for the company’s debts or other obligations, but there are certain exemptions. The Board of Directors and the Managing Director have extensive responsibility and in certain cases these persons can become personally liable for the company’s debts.

Standard par value of shares is 1 SEK (approx. 0.12 EUR). Shares with no par value and bearer shares are not permitted.

Swedish Companies Registration Office must announce the registration entries of new Companies in the Swedish Official Gazette (Post-och Inrikes Tidningar).

On the website of the Swedish Companies Registration Office you may search for and obtain the latest information on more than one million Swedish enterprises. The information may be paid by card and will be delivered by e-mail in a few minutes.

The accessible information:

On payment of a fee, at the public database of the Trade and Industry Register it is possible to obtain the following information:

It is also possible to order the certificates of different kinds. The information obtained varies according to the certificate requested. Copies of documents such as minutes may also be ordered.

The fee may be paid in a bank to the Trade and Industry Register’s account.

The cost for incorporation of the company (AB) in Sweden including the corporate legal service for the second year is 24 350 USD (19 450 EUR):

Price21 400 EUR

including the preparation of basic set of documents for registration, registration of board of directors and accountant(s) incl. registration office fees, entries in the share register, first sending of corporate documents, NOT including Compliance fee

Price8 030 EUR

including: registered address, one nominee board member and one nominee deputy director, Bank Account, Correspondence with the Tax Agency and the Companies Registration Office, Documented board meetings and general meetings, Other corporate matters, NOT including Compliance fee

Pricefrom 700 EUR

(including: opening up and administering of the company’s bank account, invoicing and payments, current recording of transactions and financial administration, current reports of profit/loss and balance, annual reports, annual accounts and periodic reports, tax returns (incl. Value Added Tax) and income-tax returns)

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR