Taiwan is a civil law country with some elements of common law. Meanwhile, sense of justice and law culture of the country are based on Confucianism.

Today’s legal system of Taiwan inherited legal system of mainland China before 1949. Almost all Guomindang laws, which ceased to be in force on mainland China after establishment of PRC, continued to be valid on the island. Since 1949 Guomindan legislation was modified according to the needs of accelerated capitalist development of Taiwan.

Since 1980s democratization of Taiwan legal system took place. Alongside liberalization of political life, repeal of military law (1987), draconian criminal laws which were aimed to fight with communist acitivites became invalid.

The main sources of law are legislative acts and other regulatory acts with Constitution of 1947 at the head. ROC law is well systematized. All the acts can be divided into several groups: constitutional, civil, criminal, criminally-remedial, administrative (including labor, financial and land law).

According ROC law there are following types of business entities in Taiwan:

Unlimited companies are registered more rarely than other types of business entities. Foreign investors usually choose limited company, company limited by shares, foreign branch or representative office.

|

Requirements

|

Company

|

Partnership/Sole Proprietorship

|

|

Minimum capital requirement

|

No minimum requirement*, but the capital still needs to be examined and certified by a local CPA that it covers at least the incorporation cost

|

Not required

|

|

Extent of liability

|

Liable to the extent of capital contribution to the company

|

Liable for any liabilities arising from the business operation

|

|

Qualification of being a juristic person

|

Qualified as a juristic person

|

Not qualified as a juristic person

|

|

Requirement for accounting books

|

Compulsory

|

Not compulsorily required

|

*If the business entity engages in activities that require a special permit or approval, the authorities may set a higher capital requirement.

|

Requirements

|

Company (Company Limited by Shares/Limited Company )

|

Foreign Branch

|

Representative Office

|

|

Permitted activities

|

general trading, sales and manufacturing not requiring a special permit or approval

|

general trading, sales and manufacturing not requiring a special permit or approval

|

legal acts and liaison activities

|

|

Income Tax(T)

|

income less than 120.000 tax=0; income more than 120.000 TWD, but less than 181.818 TWD, tax=(income -120.000)*1/2; income more than 181.818 TWD, T=17%

|

income less than 120.000, tax=0; income more than 120.000 TWD, but less than 181.818 TWD, tax=(income -120.000)*1/2; income more than 181.818 TWD, T=17%

|

---

|

|

Profit remittance tax

|

20% + 10% surtax on undistributed profits

|

none

|

---

|

|

Tax incentives under the Statute for Industrial Innovation

|

applicable

|

not applicable

|

not applicable

|

|

Extent of the liability

|

liable to the extent of their capital contribution to the company

|

foreign head office is liable for any liabilities unsettled by the branch

|

---

|

|

Shareholders

|

at least one individual or corporate shareholder (in case of company limited by shares: one corporate shareholder or two individual shareholders); all shareholders may be foreign nationals residing outside of Taiwan

|

not required to have shareholders but required to register a responsible person

|

not required

|

|

Directors

|

1-3 directors (in case of company limited by shares: at least 3 directors)

|

not required

|

not required

|

|

Minimum capital requirement

|

not required*, but the capital still needs to be examined and certified by a local CPA and covers at least the incorporation cost

|

not required*, but the capital still needs to be examined and certified by a local CPA and covers at least the incorporation cost

|

not required

|

|

Keeping of accounting books and records

|

required

|

required

|

required

|

* If the business entity engages in activities that require a special permit or approval, the authorities may set a higher capital requirement.

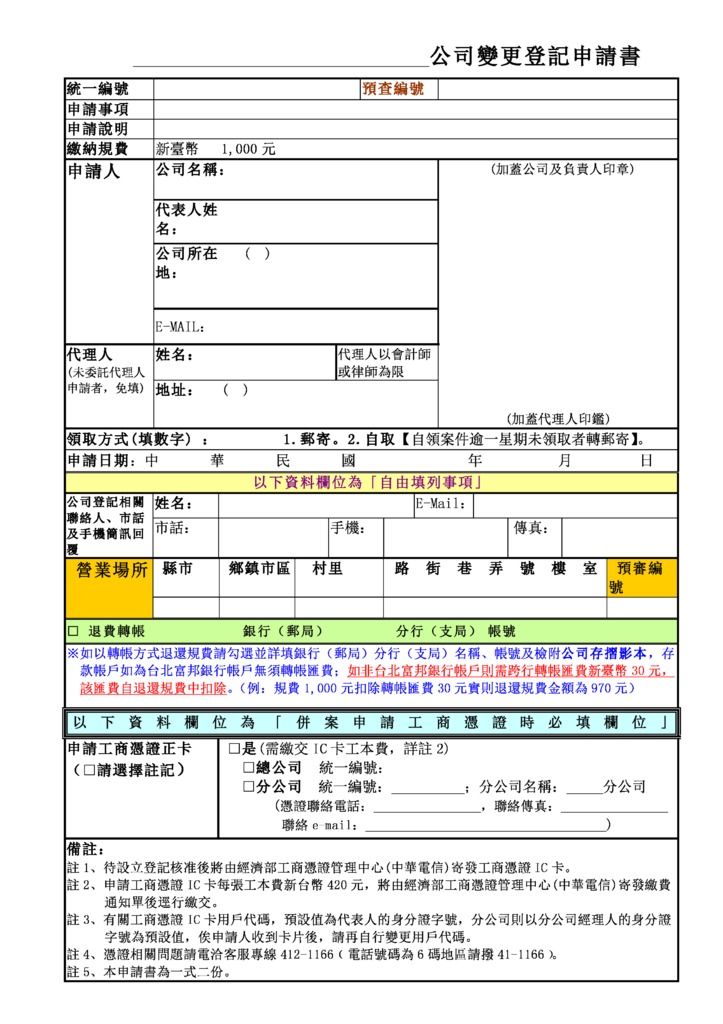

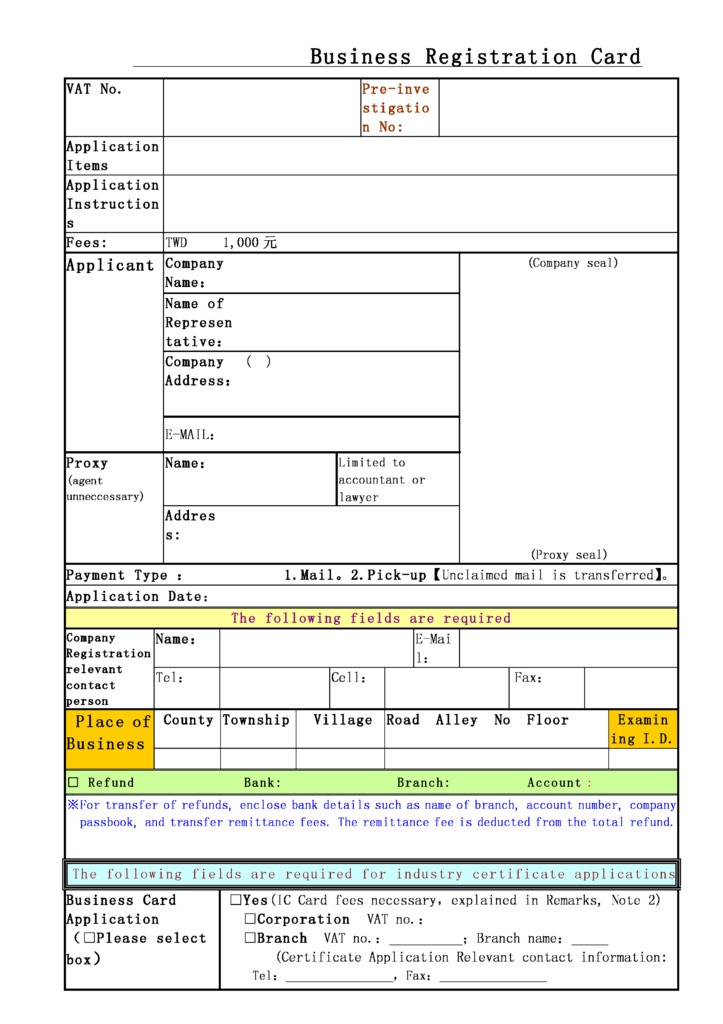

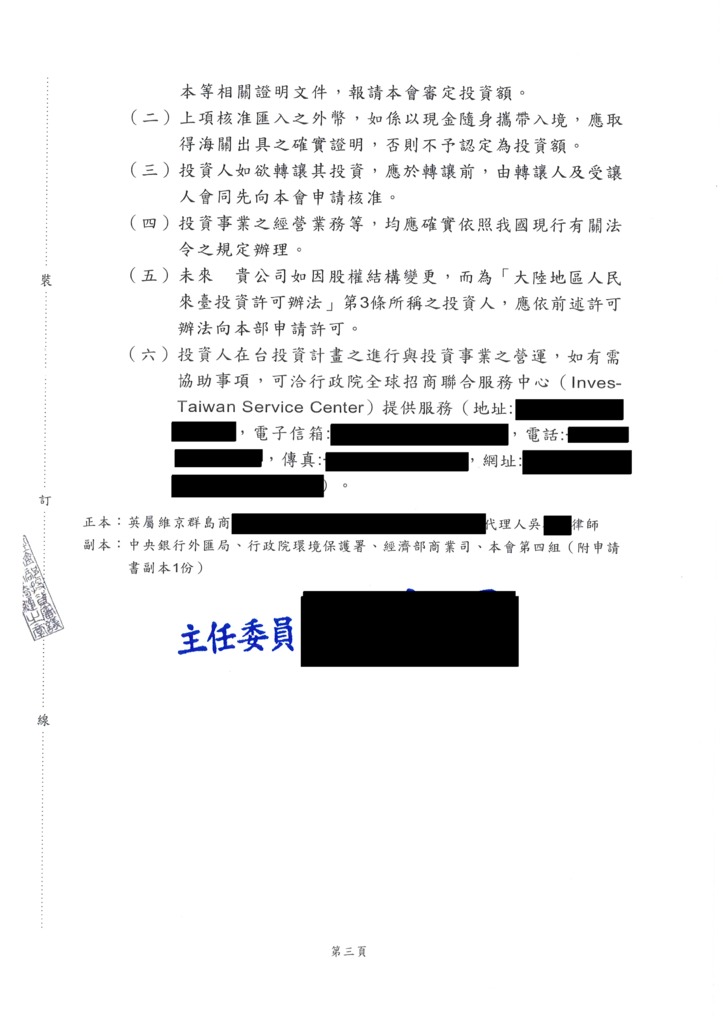

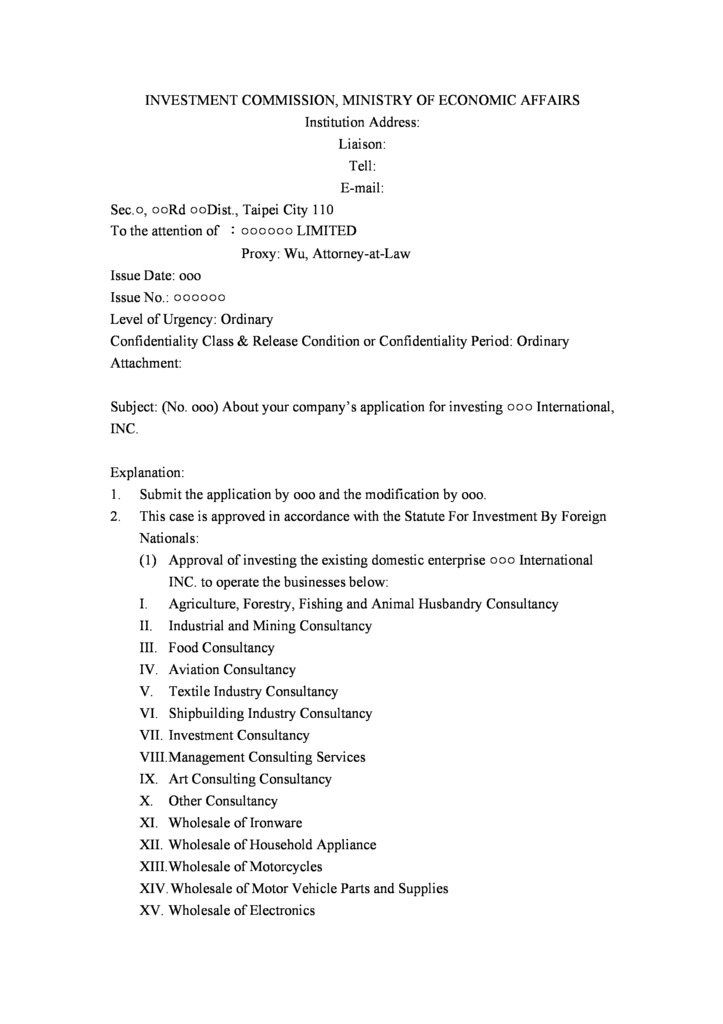

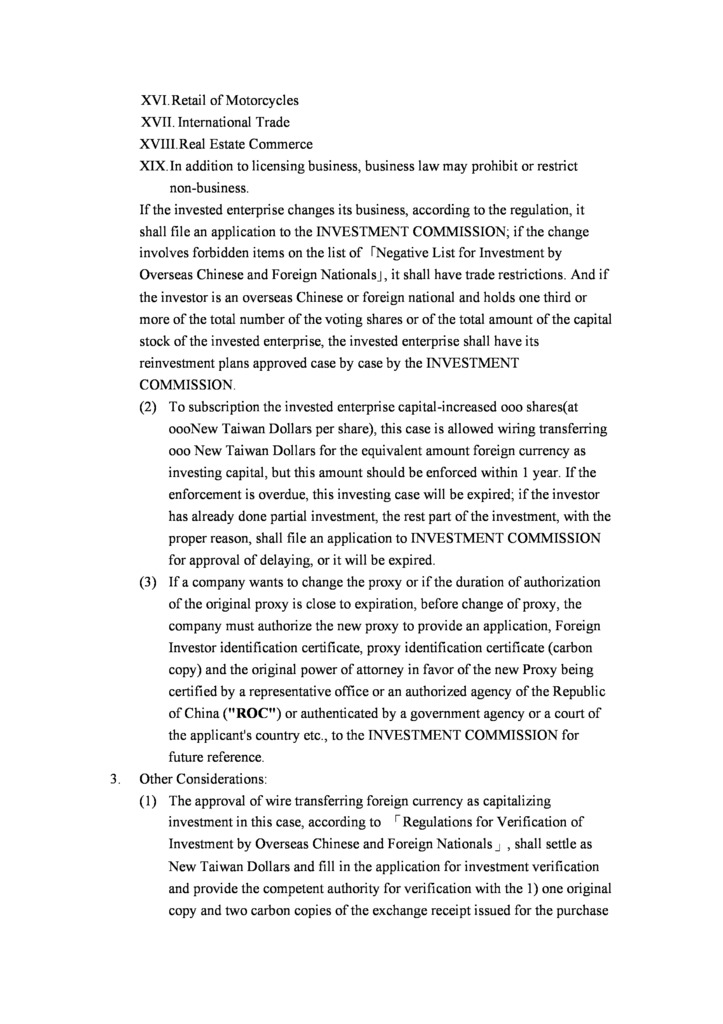

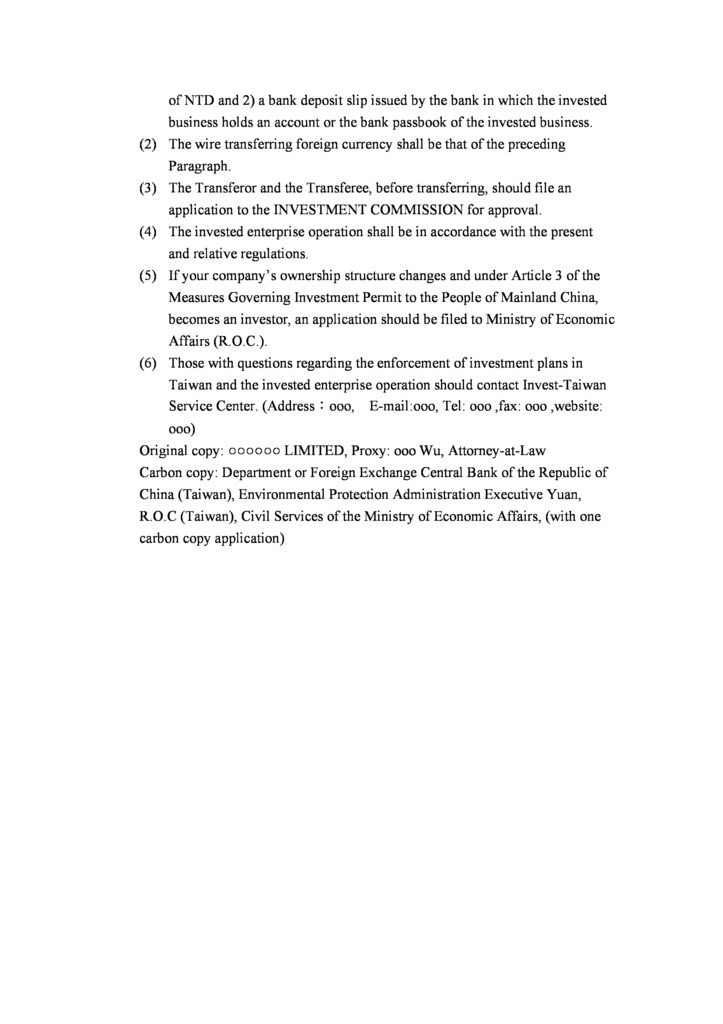

There are several steps of registration of a company limited by shares in Taiwan:

1. Apply for search and reservation of company name and business scope (please provide 1 to 5 company names in Chinese in their order of priority and proposed business scope).

2. Apply for Foreign Investment approval.

Required documents (a Chinese translation of these documents shall be attached):

3. Apply for Examination of Investment Capital.

Required documents:

4. Apply for company registration (a pre-approval is required before applying for company registration if the company intends to conduct special business which is subject to additional requirements and regulations ruled by the competent authority).

Required documents:

5. Apply for business registration.

6. Apply for factory registration (this is not applicable to a non-manufacturing business).

7. Apply for registration of importer/exporter (for trading business only).

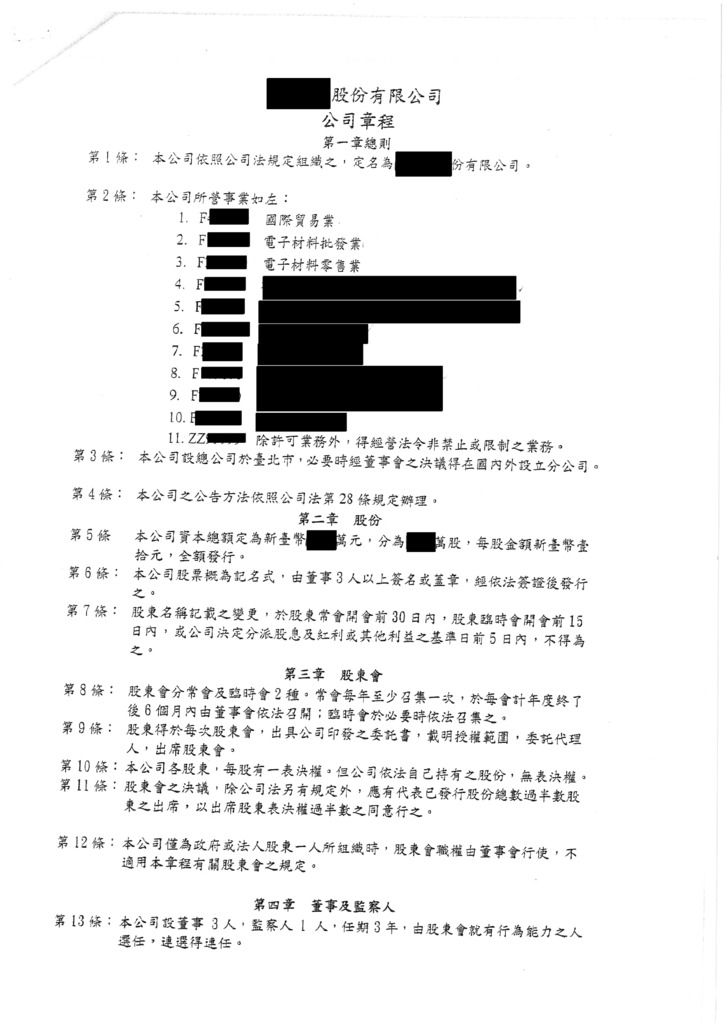

The name of a foreign company should be translated into Chinese, contain type of business entity and nationality. Companies cannot use identical names. Company name should not mislead people, contain words associated with state agencies or social organizations, have an implication of offending against public order or good customs.

Company should have a local registered office. Articles of Incorporation must be kept in the office. In case of violation a fine of not less than 10.000 TWD and not more than 50.000 TWD shall be imposed.

To seal all registration documents and acts company should get a set of seals, including a seal with a company name, a seal with a name of a chairman of board of directors. Each seal costs 450 - 1.000 TWD depending on a quantity of used material.

Company cannot be redomiciled in Taiwan.

Company limited by shares should at least have 3 directors and 1 supervisor. At least a half of directors should be locals residing in of Taiwan. Supervisor represents interests of share holders and is elected from shareholders.

Limited Company can be managed by one director, maximum - 3 directors. Directors are elected from shareholders (legal or natural person). If there are several directors, then one of them acts as an external representative of the company. There are no restrictions on the residency of the director.

Company Limited by Shares should have a Board of Directors. All decisions by the Board should be confirmed by personal signatures of directors. Making decisions through proxy or by phone is prohibited. However, in case of meeting through a video conference call director is considered to have attended the meeting. If a director resides abroad, he can appoint a shareholder residing in Taiwan to be his proxy in writing to take part in meeting on a regular basis.

It is also necessary to choose a director, directing manager or a supervisor to be responsible person who will be in charge of the everyday activity of the company. It is not needed to appoint a local agent to solve legal arguments.

There are no requirements for a Limited Company to have a board of directors.

Secretary is not required. However, company should have at least one managing director who should be a resident of Taiwan.

Company Limited by Shares shall be incorporated by at least one corporate shareholder or two individual shareholders. Shareholders should unanimously adopt the Articles of Incorporation, copy of which must be kept by every shareholder. Shareholders should hold meetings at least once a year. Annual meeting must be held within 6 months after closing a financial year. In case of violation director who represents the company is bound to pay a fine 10.000 to 50.000 TWD.

Shares of the company can be transferred to a third party. There is only one restriction. First shareholders – incorporators of the company cannot transfer their shares within a year after company incorporation.

A Limited Company must be formed by one or more shareholders, who may be an individual or a legal entity. Shareholders are required to unanimously adopt the Articles of Incorporation of the company, a duplicate of which must be kept by each shareholder.

The information on beneficiary is not disclosed.

Minimum capital depends directly on the business type of a company. Minimum capital requirement was canceled by Ministry of Economy. But the capital still needs to be examined and certified by a local CPA and covers at least the incorporation cost.

Registered capital can be paid in installments.

In Company Limited by Shares shareholders are liable to extent of paid in capital share. Capital is divided into shares which have the same nominal price.

The requirements for the mandatory presence of a minimum capital have been abolished by the Ministry of Economy of the country. However, instead of them, a new rule was introduced to provide officials with an audit report prepared by an independent state auditor, which would indicate that the investment capital of the founders would cover the costs of starting a company.

For a Limited Company, the authorized capital must be paid in full by all shareholders, without dividing into contributions and without recourse to external sources.

The following particulars of company registration shall be made open to the public by the competent authority:

Any person may apply to the competent authority for a charged access to the above information.

The total amount of core services include incorporation services, legal services and delivery of documents by courier mail

Price9 500 USD

including incorporation tax, state registry fee, NOT including Compliance fee

Price5 500 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 500 USD

Paid-up “nominee director” set includes the following documents

Paid-up “nominee shareholder” set includes the following documents

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD