The legal system of Canada is English common law for all matters within federal jurisdiction and in all provinces and territories except Quebec, which is based on the civil law, based on the Custom of Paris in pre-revolutionary France as set out in the Civil Code of Quebec.

In Ontario, the legal system is based on English common law.

The principal forms of business organization in Ontario are:

For offshore purposes, the most common structures in Ontario are the extra-provincial corporation and limited partnership.

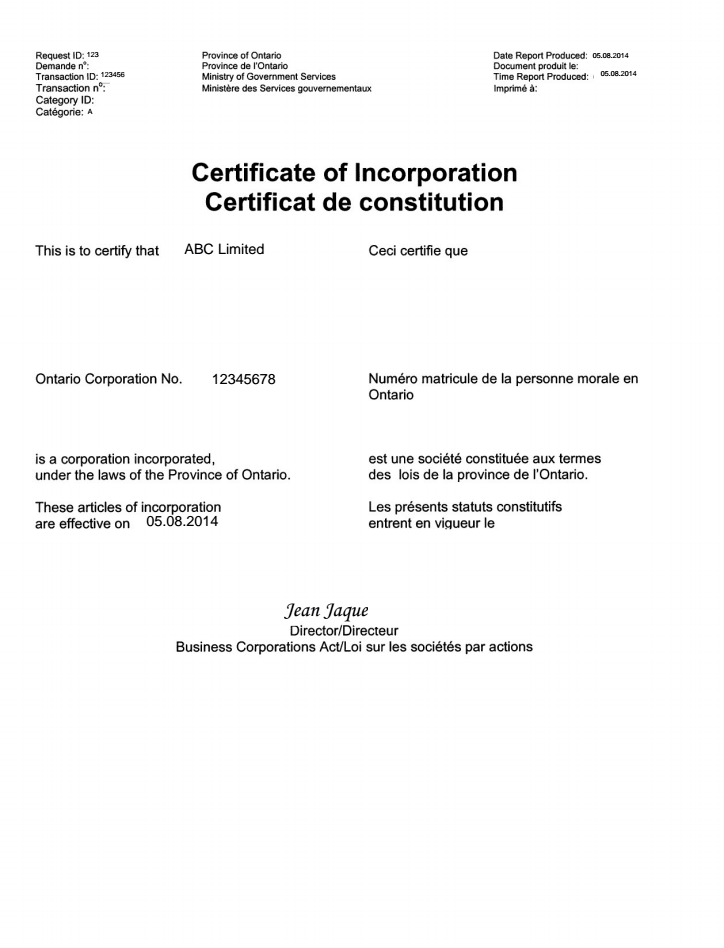

Extraprovincial Corporation is a company incorporated, continued or amalgamated federally or in other Canadian provinces (extra-provincial domestic) than Ontario. It is a company with transferable ownership, continuous existence and separate legal entity. The Ministry of Government Services issues Ontario Corporation Numbers to domestic corporations that wish to carry on business in Ontario. Non-resident foreign corporations (including offshore corporations) must obtain an extra-provincial license in order to operate and carry on business in Ontario as set out in the Ontario Extra-Provincial Corporations Act. This extra-provincial license (EPL) must be obtained before the non-resident foreign corporation commences carrying on business in Ontario.

Non-resident foreign limited liability companies are unincorporated organizations and are a hybrid of both a corporation (separate legal personality) and a partnership (flow-through taxation). Unlike non-resident foreign corporations, non-resident foreign limited liability companies are not subject to the Ontario Extra-Provincial Corporations Act and are not required to obtain an Ontario extra-provincial license in order to operate and carry on business in Ontario. Rather, non-resident foreign limited liability companies are extra-provincially registered in Ontario under the Ontario Business Names Act. Registration is a simple process with a nominal Ontario government filing fee of CAD 80.00. The government processing time is the same day.

In accordance with the Ontario Extra-Provincial Corporations Act, “carrying on business” is defined very broadly to cover most business/commercial activities. It includes, but is not limited to, having an Agent for Service, representative, warehouse, office, and/or an interest in real property (other than a security interest, such as a mortgage) in Ontario.

The status of an Ontario extra-provincial corporation enhances the business image of non-Canadian companies. The extra- provincial license gives rights to the non-resident foreign corporation to set up an office, open a bank account and conduct business in the Province of Ontario and, from Ontario, conduct business with all other Canadian provinces/territories and overseas.

It is important to note that the extra-provincial registration of the non-resident foreign corporation in Ontario does not create a separate Canadian legal entity; however, such corporation registered as an extra-provincial corporation in Ontario will still be subject to tax on its income earned in Canada at the regular corporate tax rates

Every corporation in Canada must have a name; it may be a corporate name or a numbered name.

Company name must be distinct from the names of all other corporations in Ontario.

A corporate name should contain three elements:

A company name should not contain any prohibited words or phrases, such as <i>“co-operative”, “credit union” or “municipal”, “Engineering”, “Nursing Home”, “bank”, “trust”, “insurance”, “stock exchange”, “college,” “institute,” or “university”</i>, as well as words suggesting connection with government.

Company name should not be obscene or too general.

Business names must be registered in the Roman alphabet (English, French, Spanish, Italian, Latin, etc.) and may contain numerals.

In order to have the exclusive use of a corporate name in Canada, you must provide two things to Corporations Canada:

An approved federal corporate name offers an extra degree of protection of your rights to that name. Specifically, federal incorporation allows your business to operate using its corporate name right across Canada, which is important if you decide to expand your business to other provinces or territories.

Every incorporating jurisdiction in Canada screens proposed corporate names. However, if you incorporate under the legislation of one province or territory and later want to expand your business to another province or territory, you could find that another corporation is already using a name similar to yours in that other location.

Please note that the Province of Quebec does not currently provide corporate name data to NUANS. It is your responsibility to verify with the Registraire des entreprises, Quebec that the chosen corporate name is not used in Quebec by another business.

Instead of asking Corporations Canada to approve a name for your corporation, you can also choose to have a number name assigned (e.g., 1234567 Canada Ltd.). In such cases, Corporations Canada simply assigns the next available number when processing the articles. You must ask for a number name when you apply for your Articles of Incorporation. A NUANS Name Search Report is not needed.

Many companies choose this option when a corporate name is not important to their business. This ensures faster processing and saves the expense of a NUANS Name Search Report.

Another option is to apply for a number name and ask for a name change later. To replace a number name by a corporate name, you must amend your Articles of Incorporation by filing Articles of Amendment and paying the CAD 200 fee. In this case, a NUANS Name Search Report is required.

Some incorporators choose this option when they want to incorporate a business but do not have enough time to obtain approval for a corporate name.

To incorporate an extra-provincial company in Ontario, the following steps are required:

1. Complete Form 1 Application for Extra-Provincial License and Form 2 Appointment of Agent for Service: these forms should be completed in duplicate and bear original signatures on both copies.

2. Conduct and obtain required Ontario NUANS name search report to reserve name in Ontario (CAD 48.00).

3. Prepare Ontario Agent for Service Agreement.

4. Obtain Certificate of Status from the home jurisdiction, issued under seal of office and signed by the proper officer of the home jurisdiction setting out:

Note: If the home jurisdiction will not issue an original Certificate of Status with the above information, a legal opinion from a lawyer authorized to practice in that jurisdic¬tion, setting out all the above information, will be required.

The Ontario Extra-Provincial License is issued under the Ontario Extra-Provincial Corporations Act.

The foreign corporation receives its Ontario Extra-Provincial License with an assigned Ontario corporation number confirming its extra-provincial registration in Ontario.

The government fee for license is CAD 330.00.

It takes 3 to 4 weeks to register a company extra-provincially.

Every extra-provincial corporation that carries on its business in Ontario shall ensure the continuing appointment, at all times, of an individual, of the age of eighteen years or older, who is resident in Ontario or a corporation having its head office or registered office in Ontario as its agent for service in Ontario on whom service of process, notices or other proceedings may be made and service on the agent shall be deemed to be service on the corporation.

A Canadian corporation is not required to have a seal. If you want to have a corporate seal for your corporation, you may purchase one from a legal stationery store or commercial supplier.

Not applicable. Directors of the EPC are not required to be reported on the public records in order to obtain and maintain an Ontario extra-provincial license (EPL).

Not applicable. Secretaries and other officers of the EPC are not required to be reported on the public records in order to obtain and maintain an Ontario extra-provincial license (EPL).

Not applicable. Shareholders of the EPC are not required to be reported on the public records in order to obtain and maintain an Ontario extra-provincial license (EPL).

Beneficiary. Not applicable. Beneficiaries of the EPC are not required to be reported on the public records in order to obtain and maintain an Ontario extra-provincial license (EPL).

Not applicable.

If a corporation with an Extra-Provincial License decides to cease carrying on business within the province of Ontario, the corporation must complete and submit in duplicate, Application for Termination of Extra-Provincial License, Form 4 under the Extra-Provincial Corporations Act to the Companies and Personal Property Security Branch.

In addition, the corporation must submit an Initial Return/Notice of Change, Form 2, under the Corporations Information Act to the Companies and Personal Property Security Branch with the Application for Termination of Extra-Provincial License, Form 4. This form must be completed with the appropriate information and must include the “Date Commenced” business activity in Ontario and the “Date Ceased” carrying on business activity in Ontario (item numbers 9 and 10 on the form).

Price2 600 USD

including incorporation tax, state registry fee, NOT including Compliance fee

Priceincluded

Stamp Duty and Corporate Registry incorporation fee

Price1 600 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 500 USD

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD