Hungary offers entrepreneurs a unique combination of European respectability and favorable business conditions. As a jurisdiction consistently absent from offshore "blacklists," the country has established itself as a reliable and stable destination with a transparent banking system that accommodates both euro and US dollar transactions. The company registration process is remarkably efficient, with corporate bank accounts potentially opened within a single business day, significantly accelerating commercial operations.

The Hungarian tax system stands out as one of Europe's most attractive frameworks. With a corporate tax rate of just 9% (capped at 11% including municipal levies) and a 0% rate on dividends and capital gains, the jurisdiction proves particularly advantageous for holding structures and investors. Newly registered companies automatically receive an EU VAT number, while Hungary's extensive network of double taxation treaties facilitates optimized international financial flows.

A key advantage lies in the ability to quickly establish substantive business presence in compliance with modern international requirements. Furthermore, operating in Hungary creates pathways to obtaining Schengen residence permits - a valuable opportunity for Europe-focused entrepreneurs. This combination of European reliability and economic advantages positions Hungary as an exceptionally attractive jurisdiction for international business operations.

Hungary offers one of the most attractive tax systems in Europe, making the country a preferred destination for international corporations and startups. The combination of low tax rates and transparent regulation creates optimal conditions for conducting business within the EU.

Corporate taxation in Hungary features competitive rates. A 9% tax rate applies to profits not exceeding HUF 500 000 000 (~ EUR 1 400 000), while profits above this threshold are taxed at 12%. A distinctive feature of the system is the potential reduction of the tax base through dividend payments, subject to specific conditions.

Small businesses may benefit from special tax regimes, including the itemized tax for small businesses (KATA) with fixed monthly payments of HUF 50 000 for annual turnover below HUF 12 000 000. Sole proprietors enjoy simplified reporting requirements, significantly reducing administrative burdens.

The Hungarian VAT system employs multiple rates. The standard rate stands at 27% (the highest in the EU), with a reduced rate of 18% applicable to certain food products and services, and a super-reduced rate of 5% for essential medicines, medical equipment, and printed publications. Mandatory VAT registration becomes compulsory when annual turnover reaches HUF 8 000 000 (~ EUR 22 000), with reporting options available on either monthly or quarterly basis depending on company size.

Individual taxpayers in Hungary are subject to progressive taxation: 15% and 20% rates apply based on income levels. Additionally, social contributions of 18.5% are levied, while sole proprietors pay a special entrepreneurial tax (SZOCHO) at 13%.

Hungary actively promotes investment through tax incentives for job-creating enterprises, regional development projects, and research-intensive activities. The country maintains an extensive network of international tax treaties (exceeding 70 agreements), effectively mitigating double taxation risks.

Since 2023, Hungary has implemented sector-specific taxes targeting banking, retail, and telecommunications industries. The tax administration system demonstrates advanced digitalization - most filings are submitted electronically through the EBEV government portal, substantially streamlining compliance procedures with fiscal authorities.

The cornerstone of Hungarian corporate law is Act V of 2013 on the Civil Code, which sets forth general principles of civil legal relations, including the status of legal entities, rights and obligations of company members, and matters concerning management liability. This document serves as the basis for all subsequent specialized regulations in corporate governance.

Primary issues regarding company formation and operations are thoroughly regulated by Act V of 2006 on Companies. This legislative act covers all aspects of corporate life - from registration procedures and share capital requirements to corporate governance matters and shareholder rights. The law provides for various business structures, including limited liability companies (Kft) and joint-stock companies (Rt), establishing specific operating rules for each type.

Financial reporting and accounting practices of companies are governed by the Accounting Act of 2000, which defines accounting standards, disclosure requirements, and audit procedures. This legislation ensures transparency in financial operations of Hungarian companies and aligns with international financial reporting standards.

Taxation aspects of corporate activities are determined by the Corporate Tax Act of 1996, establishing a 9% tax rate for profits up to HUF 500 000 000, and the Value Added Tax Act of 2007, which implements a standard VAT rate of 27%. These regulations contain detailed rules for calculating tax liabilities and submitting reports to tax authorities.

A special place in the corporate regulatory system belongs to the Securities Act of 2001, which governs share issuance and trading, stock exchange operations, and regulation of corporate securities. This legislation protects investor rights and facilitates corporate financing.

The competitive environment in Hungary is regulated by the Competition Act of 1996, prohibiting monopolistic practices, unfair competition, and restrictive agreements between market participants. In cases of corporate bankruptcy, provisions of the Bankruptcy Act of 1991 apply, establishing liquidation procedures and creditor claim satisfaction processes.

The principal forms of business organization in Hungary are:

Suitable for: freelancers, small businesses, consultants.

The sole proprietor (Egyéni vállalkozó) represents the simplest form of conducting business. This structure is ideal for freelancers, consultants, and owners of small enterprises. The main advantage is minimal bureaucratic requirements during registration. The entrepreneur has complete decision-making freedom and can choose between different taxation systems, including the favorable KATA regime with fixed payments. However, a significant disadvantage is unlimited liability, where personal assets may be used to settle business debts. Additionally, this form is not suitable for business scaling.

Pros:

✅ Simple registration – minimal bureaucratic requirements.

✅ Full control – the owner makes all decisions.

✅ Tax flexibility – the entrepreneur can choose between income tax (15% or 9% for incomes up to 18 million HUF per year) or a fixed tax (KATA) – for small entrepreneurs (HUF 50 000 / month with a turnover of up to HUF 2 000 000 per year).

Cons:

❌ Unlimited liability – personal assets may be used to settle debts.

❌ Limited scalability – difficulty attracting investors.

**Registration:**

- Submission of an application to the Hungarian Tax Authority (NAV).

- Obtaining a tax number (adószám).

A general partnership (Kkt.) is suitable for those planning to conduct business jointly with partners. The main advantage is the absence of capital requirements and flexibility in management. However, all partners bear joint and several liability for the partnership’s obligations, which creates significant risks. Conflicts between partners may arise due to the need for unanimous decision-making.

Pros:

✅ No capital requirements – can start without investments.

✅ Management flexibility – partners determine the working rules themselves.

Cons:

❌ Unlimited joint and several liability – all partners are liable with their personal assets.

❌ Risk of conflicts – decisions are made unanimously.

Taxation:

- Profits are taxed at the partners’ level (as personal income).

Registration:

- Signing the partnership agreement.

- Entry into the Companies Registry (Cégközlöny).

Suitable for projects where one partner contributes capital and another manages. A limited partnership provides mixed liability: the managing partner is fully liable, while the contributing partner is liable only up to their contribution. Although this structure allows flexible profit distribution, it remains risky for the managing partner.

Pros:

✅ Mixed liability: the general partner manages and bears full liability, while the limited partner contributes capital but is liable only up to their contribution.

✅ Flexibility in profit distribution.

Cons:

❌ Risk for the managing partner – their personal assets are unprotected.

Taxation is similar to a general partnership (taxes are paid by the partners).

Registration:

- Entry into the Companies Registry with specification of partners’ roles.

The limited liability company (Kft.) is the most popular form in Hungary, optimally balancing asset protection and management simplicity. Founders risk only their capital contribution, with a minimum capital requirement of HUF 3 000 000. The company can be managed either solely by a director or by a members’ meeting. However, an audit is mandatory for turnovers exceeding HUF 300 000 000, and reporting is more complex than for sole proprietors.

Pros:

✅ Limited liability – founders risk only their capital share.

✅ Minimum capital – HUF 3 000 000 (~ EUR 7 500), which can be contributed in cash or assets.

✅ Flexible structure – management via a director or members’ meeting.

Cons:

❌ More complex reporting than for sole proprietors.

❌ Mandatory audit for turnovers > HUF 300 000 000 or assets > HUF 200 000 000.

Taxation: 9% corporate tax (for incomes up to HUF 500 000 000) and 15% dividend tax.

Registration:

- Signing the articles of association.

- Depositing capital into a bank account.

- Submitting documents to the Companies Registry.

Designed for large businesses and projects planning to attract investments through share issuance. A joint-stock company exists in two forms: private (ZRt.) with a minimum capital of HUF 5 000 000 and public (NyRt.) – HUF 20 000 000. Although a JSC provides maximum growth opportunities and high counterparty trust, the registration process is more complex and requires establishing a supervisory board.

Pros:

✅ Shareholders’ liability is limited to the share value.

✅ Ability to attract investments through share issuance.

✅ High level of counterparty trust.

Cons:

❌ Complex registration – requires notarization of the articles of association.

❌ Minimum capital: for public JSCs (NyRt.) – HUF 20 000 000, for private – HUF 5 000 000.

❌ Mandatory supervisory board.

Taxation: 9% corporate tax, 15% dividend tax.

Registration:

- Drafting the articles of association, share issuance.

- Capital contribution.

- Registration in the Companies Registry.

A non-profit form of company in Hungary – created for non-commercial activities in cultural, scientific, or charitable spheres. Associations do not require capital and may qualify for tax exemptions, but commercial activities are strictly prohibited.

Pros:

✅ No capital requirement.

✅ Tax exemption if non-profit status is maintained.

Cons:

❌ Commercial activity is prohibited (only auxiliary activities allowed).

❌ Requires articles of association and court registration.

The most common structure is the limited liability company.

A Hungarian limited liability company should at least have one director. Directors can be either natural persons or corporate bodies. There are no requirements to the nationality of directors.

Directors’ meetings should be held at least once a year to approve the annual report of the company.

The names of directors appear in public records.

Hungarian limited liability companies are not required to appoint a company secretary.

Each Hungarian company must have at least one shareholder. There is no restriction on the nationality or residency of the shareholders. The shareholders can be individuals and/or legal persons.

Shareholders’ meetings must be held at least once a year, there are no requirements as to place of holding of the meeting.

The names of shareholders appear on public records.

The law introducing the Beneficiary Registry came into force in Hungary in June 2017. The deadline for its entry into force was set as January 1, 2019. However, 20 months later, the registry has still not appeared, and no separate website has been created for it. The Hungarian government claims that there is currently no definite date for the entry into force of the register of beneficiaries and it is impossible to predict that date at this time.

However, there is a list of necessary information about the beneficiary that must be included in the registry in the future: Full name, date and place of birth, citizenship, postal address, the basis for recognizing the person as the beneficiary, indicating his share in the company, the affiliation of the beneficiary to politically exposed persons.

It is worth noting that access to information from the register of beneficiaries on a par with the tax authorities will also have anti-terrorist organizations and state security services.

Minimal amount of the authorized share capital of a Hungarian limited company is HUF 3 000 000. Within the incorporation procedure each member must deposit his contribution – 50% of monetary assets. The other 50% of monetary assets must be paid within 1 year from the date of incorporation of the company. If there is only one founder in the company, min. HUF 100 000 must be paid within the incorporation procedure.

Shares are not issued. Share of each member is recorded in the deed of foundation or articles of association. Standard par value of shares is 10 000 HUF.

There is a range of requirements to the company name in Hungary:

The following steps are required to incorporate a Limited liability company in Hungary:

The formation of a new company in Hungary takes from 2 to 15 days.

As a rule, a Hungarian Limited Liability Company must have a registered office in Hungary. Register of shares, minutes of meetings and accounts should be kept at the registered office.

There are no statutory requirements for a company in Hungary to have a seal.

The redomiciliation of companies to or from Hungary is permitted.

Following successful company registration in Hungary, it is necessary to ensure its ongoing legal and financial maintenance in compliance with local legislation. Hungarian companies are required to adhere to a number of corporate and tax obligations, including regular preparation of financial statements, timely filing of tax returns, and execution of mandatory corporate procedures.

Financial statements must be prepared in full accordance with Hungarian accounting standards. Companies exceeding established financial thresholds (turnover exceeding HUF 300 000 000, assets exceeding HUF 200 000 000, or more than 50 employees) are required to undergo annual audits. The auditor's report must be submitted to the Companies Registry within prescribed deadlines.

Tax obligations include filing corporate income tax returns by May 31 each year, regular VAT reporting (monthly or quarterly depending on company turnover), as well as timely payment of social security contributions for employees. Particular attention should be paid to compliance with reporting deadlines, as violations may result in penalty sanctions.

During the operation of a Hungarian company, changes to its corporate structure may become necessary. This includes replacing directors or members, adjusting share capital amounts, changing registered office addresses, or modifying business activity classifications. All such changes require timely amendments to founding documents and mandatory registration with relevant government authorities.

To ensure uninterrupted company operations, it is recommended to engage local accounting services that will assist with compliance reporting requirements, as well as obtain regular legal consultations regarding corporate governance matters. Proper administration of a Hungarian company will minimize legal risks and ensure stable business operations in accordance with local regulations.

Third parties can request the following information on Hungarian companies:

All documents filed to the Registrar including deed of foundation or articles of association are available to public inspection.

PriceEUR 5 780

including a registered address for the first year without postal services, preparation and provision of the company’s original founding documents and seal

PriceIncluded

Stamp Duty and Registration Court incorporation fee

PriceEUR 3 630

including registered address and registered agent, NOT including Compliance fee

PriceEUR 275

DHL or TNT, at cost of a Courier Service

Pricefrom EUR 500

Pricefrom EUR 6 050

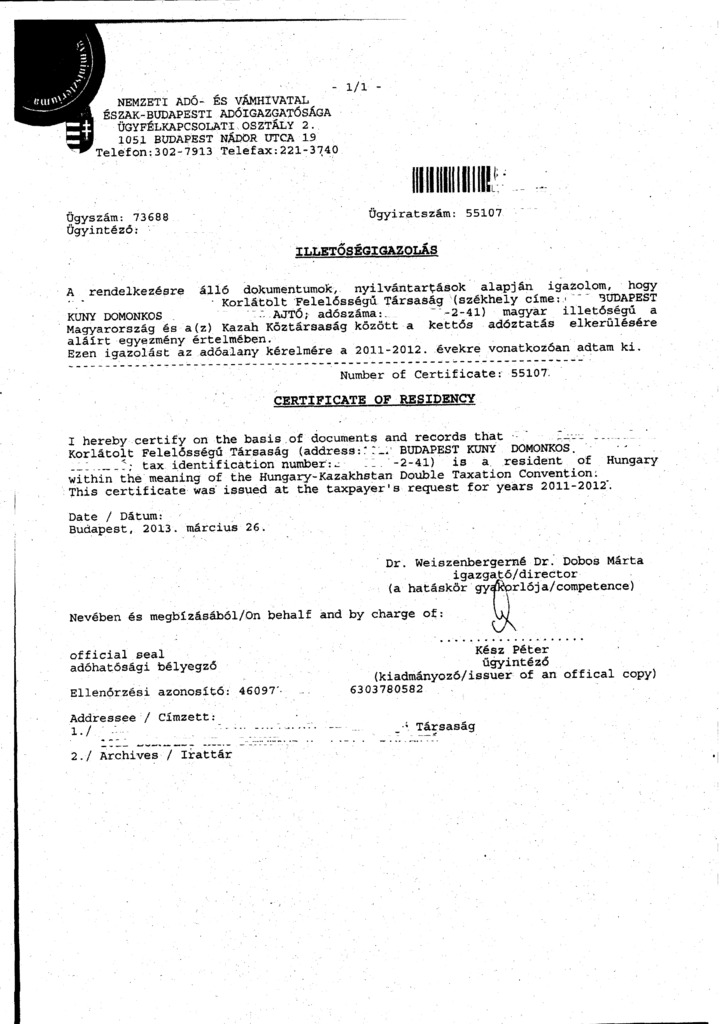

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

PriceEUR 385

simple company structure with only 1 physical person

PriceEUR 165

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

PriceEUR 220

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

PriceEUR 495

PriceEUR 110