Germany has a civil law system based on Roman law with some references to Germanic law.

The principal forms of business organization in Germany are:

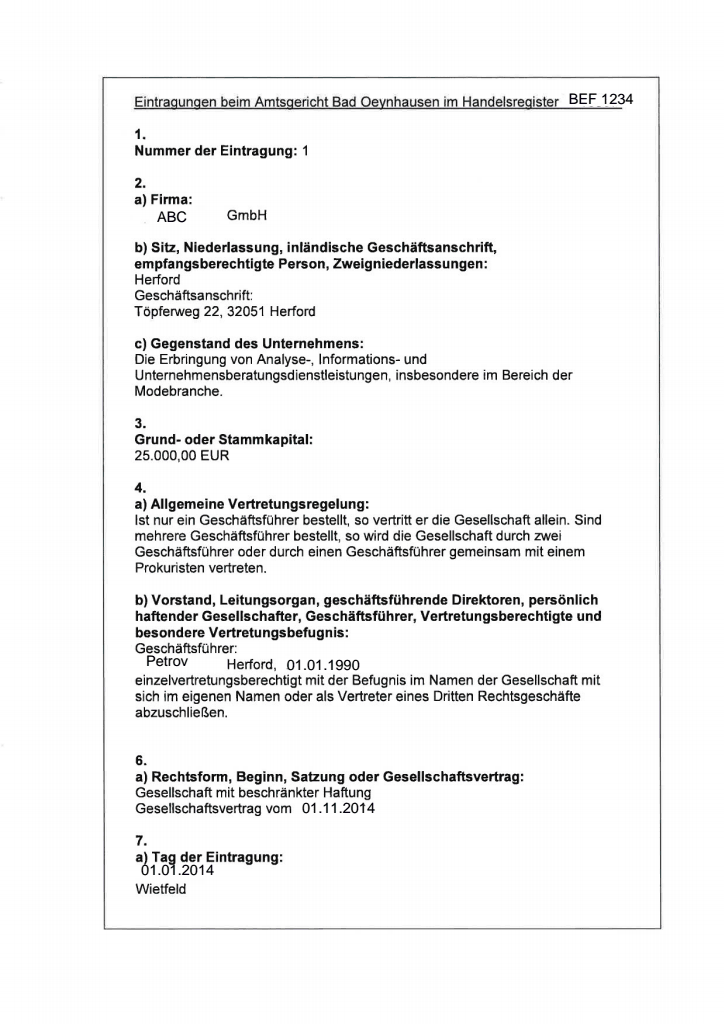

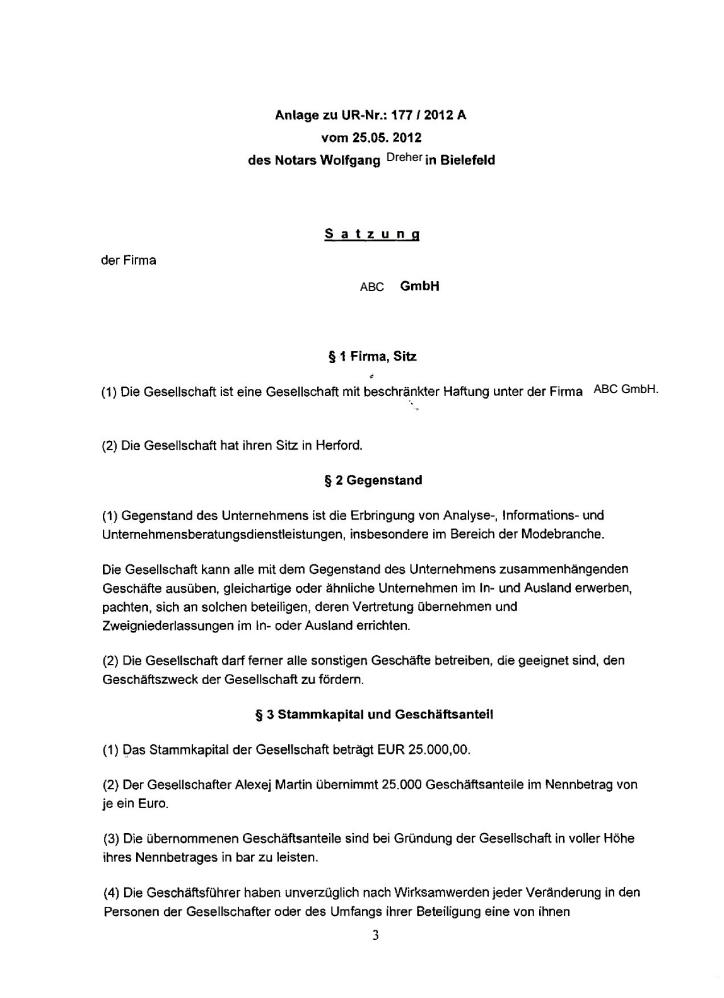

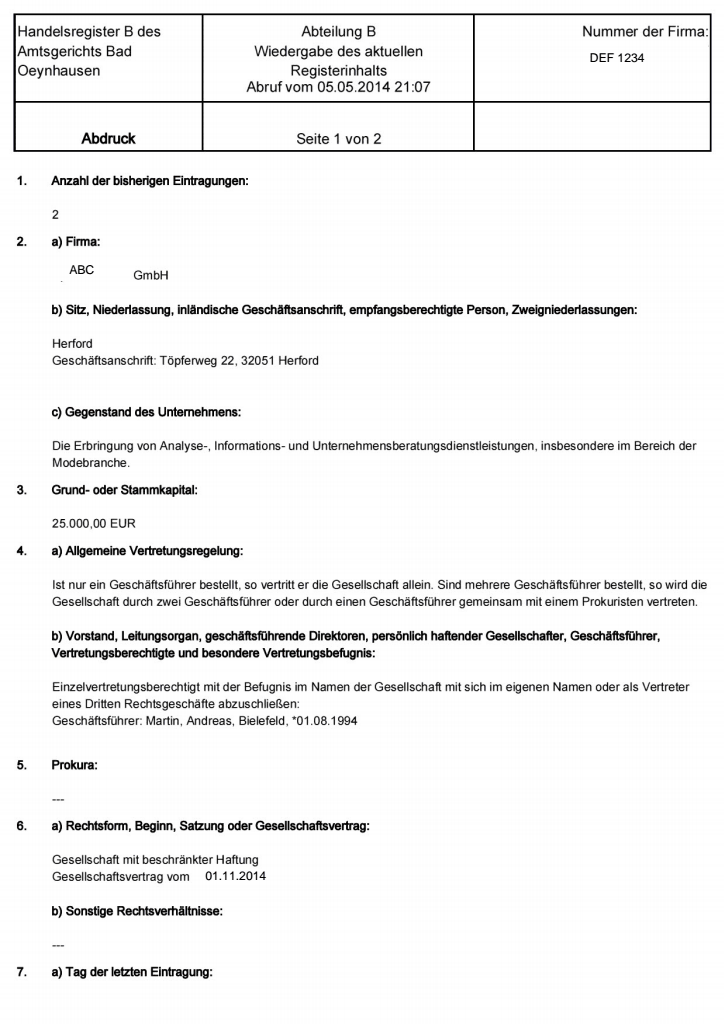

The most common structure is the Company with Limited Liability (Gesellschaft mit beschränkter Haftung, GmbH)). It is governed by the Act concerning Companies with Limited Liability (Gesetz betreffend die Gesellschaften mit beschränkter Haftung, GmbHG).

The corporation designation of the LLC can either be based on the company’s activity (factual designation), contain the name(s) of one or more shareholder(s) (designation by name) or only comprise a fantasy name. Combinations of these elements are also possible, and in any case the factual designation must contain an individualising addition.

The addition “Limited Liability Company” ("Gesellschaft mit beschränkter Haftung") or the abbreviation “LLC” ("GmbH") is a mandatory component of the corporate name.

On the examination of the admissibility of the corporate name by the Court, the principles of identity of the company are to be considered.

The corporate name may not contain any additions suited to causing deceit about the nature and the scope of the business.

Geographical additions are admissible as a matter of principle if the company has a specific relationship to the area stated, e.g. its headquarters.

General describing terms (AutoGmbH), as well as specific names, if there is no founder or director with such name, are not allowed.

To incorporate a GmbH in germany the following steps are required:

1. Obtain the company’s name at the local chamber of industry and commerce: Entrepreneurs need to obtain the company’s name at the Berlin Chamber of Industry and Commerce.

2. Notarize the articles of association and memorandum of association: The fees depend on value of the share capital.

3. Open a bank account: In case of the GmbH only 25% of the initial capital has to be paid up before registration.

4. Notary public files the articles of association at the local commercial register: Applicants must submit to the Commercial Register by electronic form:

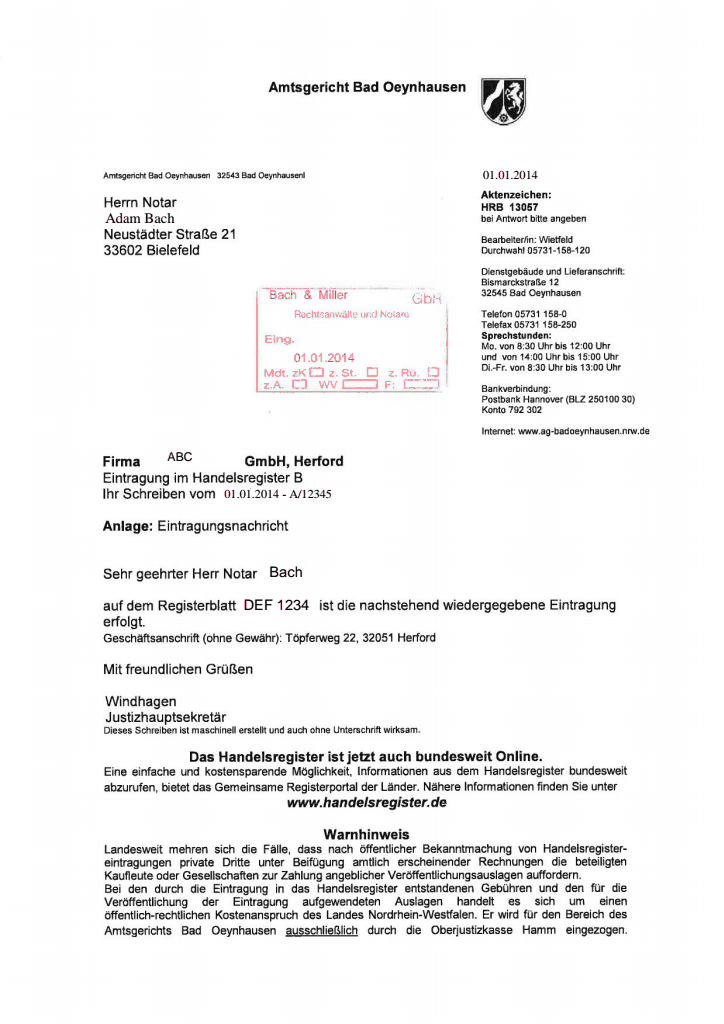

The Commercial Register publishes the registration on a central electronic platform and notifies the local Chamber of Industry and Commerce and the tax office of the new company.

5. Notify the local office of business and standards of the establishment of the company: Certain businesses (e.g. restaurants, brokers) must apply for a trading permit (Gewerbeerlaubnis). However, the permit does not have to be presented at the time of the registration of the GmbH at the commercial register. If no such permit is required, start-up companies must simply notify the local trade office which issues a trading license (Gewerbeschein). This notification procedure also covers registration formalities with the central statistical office, the relevant chamber of industry and commerce, the local labor office, the social security and federal health insurance office.

6. Register with the professional association of the relevant trade: The professional associations are carriers of occupational accident insurance. Registration must be done within a week of the founding of the business (after the notarization of the articles of association).

7. Notify the local labor office of the establishment of the company: The notification can be in writing and/or by phone. The Labor Office assigns an eight-digit operating number, which is needed to report social security.

8. Register employees for health and social insurance: The social security and federal health insurance office notifies the local labor office and the annuity insurance carrier (Deutsche Rentenversicherung Bund).The competent social security and federal health insurance office collects payment for mandatory health, unemployment, and annuity insurance.

9. Mail out the documentation to the Tax Office: Registration must be done within a month of the opening of the business, and not later than a month after the notarization of the articles of association. After the tax office is notified of the company’s business activity by the trade office, the tax office sends the company a questionnaire requesting the company’s business data.

It takes about 1 week to startup a new company in Germany.

A GmbH’s registered office (as stipulated in the articles of association) must be located in Germany. This location can differ from the location of the company’s operational facilities, the company’s management and company’s administration.

Unlike the registered office, the seat of management or administration of a GmbH can be located outside Germany (at least in another EU country or the US); in other countries it may depend on their respective corporate laws.

There are no mandatory requirements regarding the company seal.

The redomiciliation of companies either to or from Germany is not permitted.

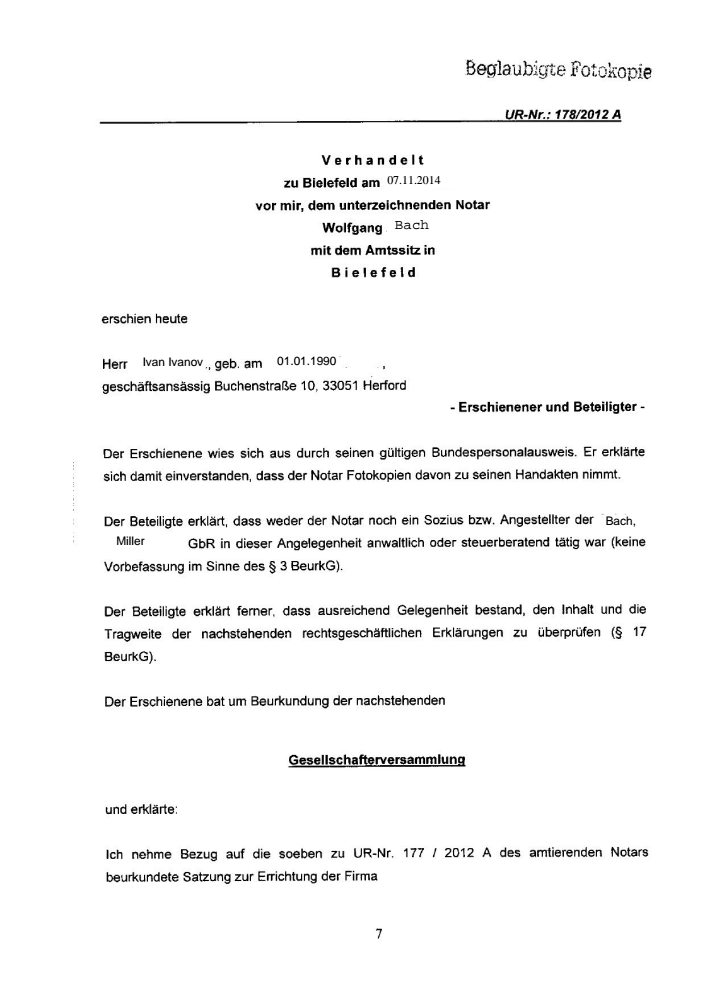

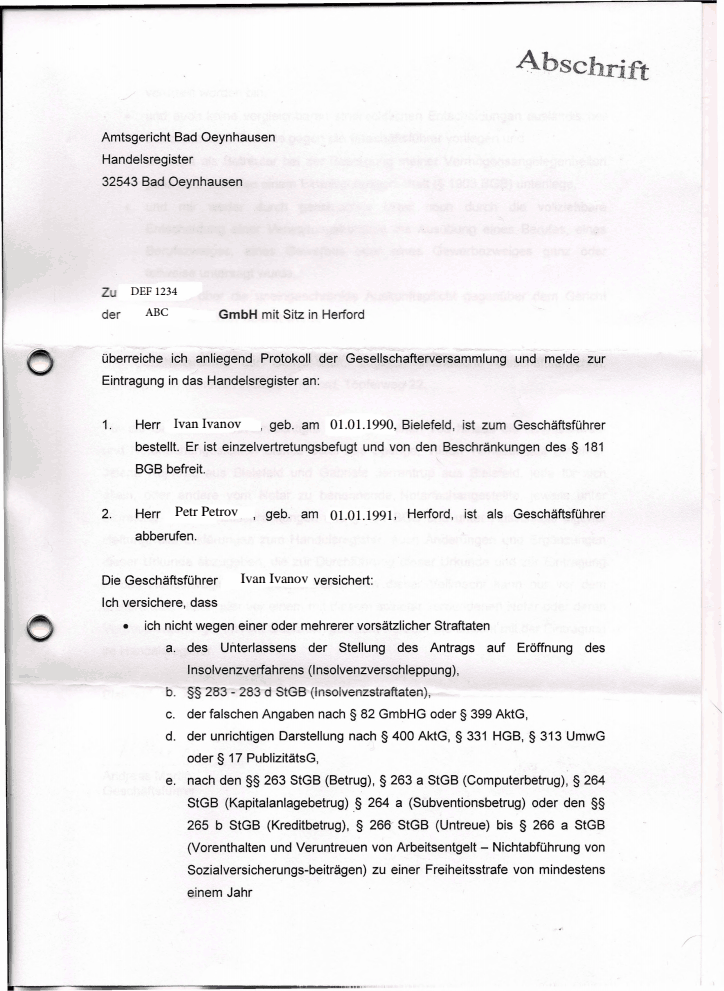

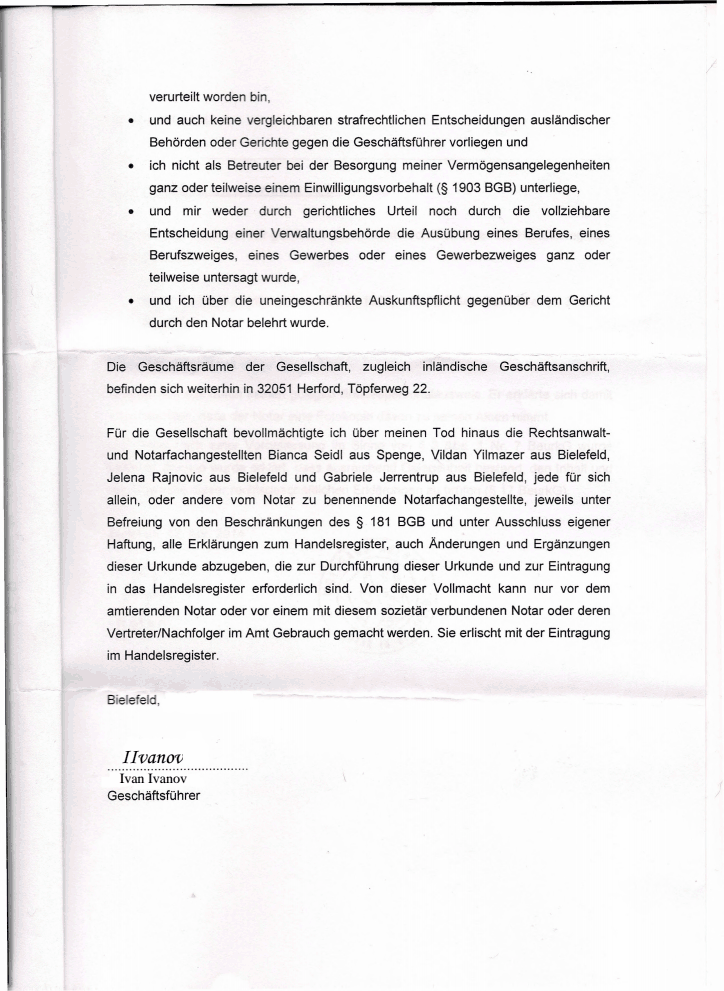

Typically a GmbH acts through one or more managing directors (Geschäftsführer) as its legal representatives. Managing directors can be, but do not have to be, shareholders of the GmbH. Any natural person of full legal capacity can be appointed as managing director. Non-German nationals can also be appointed as managing director. However, the courts sometimes require that foreign managing directors be able to freely enter Germany at any time.

The appointment to office is normally made by a resolution adopted by simple majority of the competent body – typically the shareholders’ meeting. A managing director may be removed from office at any time (also by a shareholders’ resolution adopted by simple majority). The appointment and removal of managing directors takes effect as soon as the resolution is adopted (or on the date specified in the resolution) and such resolution is entered in the commercial register.

German GmbH is not required to appoint a company secretary, but it is strongly recommended to have a secretary. There are no residency requirements, but the Secretary shall communicate and maintain correspondence in German.

No minimum or maximum number of shareholders has been prescribed. Formation of a one-man LLC is also possible. Founders of an LLC can be both German and also foreign natural and legal entities, in addition trading partnerships (general partnerships, limited commercial partnerships and EEIGs) and civil-law corporations (German: GbR).

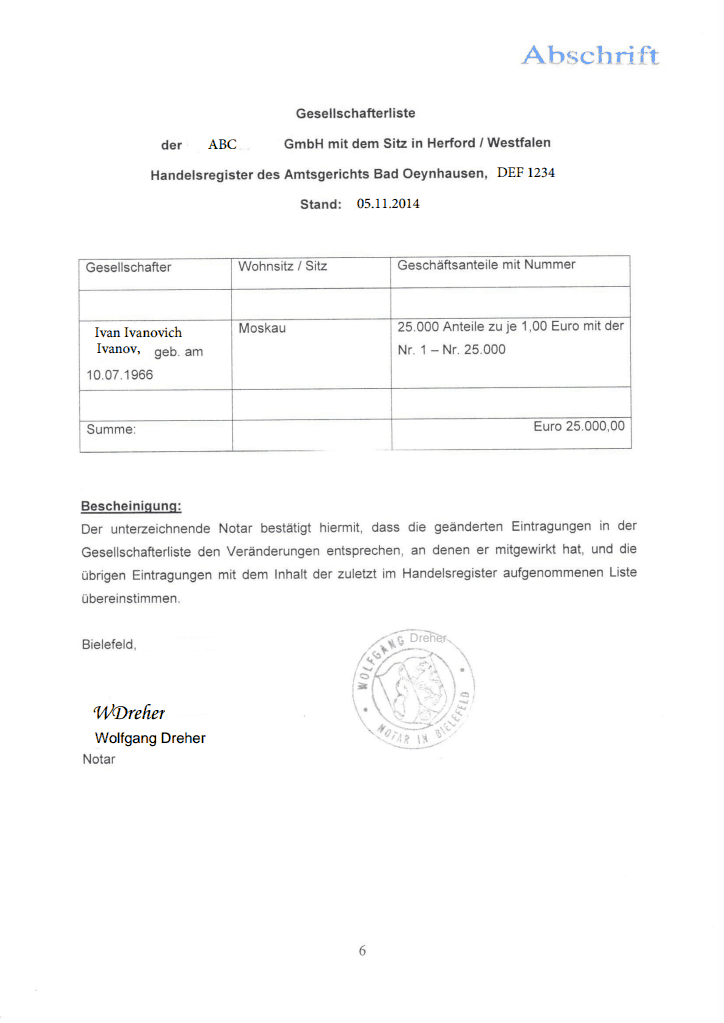

Shareholder names are filed on the public register.

The shareholders' meeting is the GmbH's highest authority/decision making body. Shareholders enjoy the rights and must perform the obligations as set out in the articles of association as well as those granted/imposed by law. Typically these include the appointment and dismissal of managing directors, the formal approval of managing directors' actions, the adoption of the annual financial statements and the appropriation of profits, and the monitoring and review of the management. Some rights and obligations are reserved to the shareholders' meeting. These include amending the articles of association, calling in additional contributions, capital measures, dissolution of the company, certain measures resulting in the formation of a corporate group, and the restructuring measures pursuant to the German Reorganisation of Companies Act (Umwandlungsgesetz, UmwG) (e.g. merger or change of form).

The until 2017/12/27 staggered inspectable central Transparency Register is designed as an overflow register (Auffangregister). Companies or other legal entities have to provide details about the beneficial owner first-time until 2017/10/01 via the Transparency Register, unless this information is already available from entries and documentations via certain other public registers.

According to that apart from the direct entries in the Transparency Register other relevant registers disclosing the beneficial owner are also accessible.

The share capital of the LLC is at least 25 000 EUR.

The share capital can be provided by the shareholders by share contributions of differing amounts. A share contribution must amount to at least 1 Euro. The share contributions can be provided in cash (cash formation) or in the form of contributions in kind (formation by contributions in kind). At least one quarter of each share contribution to be provided in cash must be paid in. The declaration to the Register of Commerce can only be made if the payments together have reached half of the minimum share capital, i.e. 12 500 EUR.

In practice, cash formation is done by an account being opened with a bank for the LLC and being at the company’s free disposal. For the entry into the Register of Commerce, the managing director must assure that the contribution is at his disposal.

Increasing or decreasing the company’s share capital requires notarial certification and is to be declared to the Register of Commerce for entry.

Price5 800 EUR

including Compliance fee, preparation and provision of originals constitutive documents of the company, as well as company seal

PriceIncluded

Stamp Duty and Register of Commerce incorporation fee

Price2 350 EUR

including registered address and registered agent, NOT including Compliance fee

Price250 EUR

DHL or TNT, at cost of a Courier Service

Pricefrom 1 500 EUR

Pricefrom 12 100 EUR

Paid-up “nominee director” set includes the following documents

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR