Jersey law has been influenced by several different legal traditions, in particular Norman customary law, English common law and modern French civil law. Jersey's legal system is therefore described as 'mixed' or 'pluralistic', and sources of law are in French and English languages, although since the 1950s the main working language of the legal system is English.

The principal forms of business organization in Jersey are:

The most common structure is the limited liability company.

There is a range of requirements to the company name in Jersey:

The following steps are required to incorporate a Limited liability company in Jersey:

The formation of a new company in Jersey takes 2 days.

A Jersey company must have a registered office in Jersey and must include its company name and registered office in all business letters, correspondence, notices, negotiable instruments and letters of credit.

Every company must maintain a register of members at the registered office of the company, or such other place in Jersey as the company may specify. The register should be open to inspection by the members of the company, without charge, during normal business hours.

Minutes of all directors' and shareholders' meetings and a register of directors and secretaries must also be maintained by a company. In each case, records held by a Jersey company may be kept in any form (whether electronic or hard copy) provided that such information can be reproduced in an intelligible manner and steps are taken to safeguard the information.

There are no statutory requirements for a company in Jersey to have a seal.

The redomiciliation of companies to or from Jersey is permitted.

A private company must have at least one director. Directors must be over 18 years of age. There is no requirement under the Law for directors appointed to Jersey companies to be resident in Jersey or to hold shares in the company. A Jersey company may appoint a corporate director, providing that such corporate director is regulated to conduct financial services business under the Financial Services (Jersey) Law 1998 and does not itself have a corporate director.

Meetings of directors of a Jersey company are not required to take place in Jersey and may be held by telephone or other means of communication, providing that those present are able to hear what is said by the other participants. It is also possible for directors to pass resolutions in writing.

Particulars of the directors must be maintained in a register kept by each company and open to inspection by members of the company and by the Registrar. The Registrar may not disclose information on the register except for the purpose of enforcing any provisions of the Law or any obligation owed to the company by a director or secretary.

All companies must appoint a secretary. In the case of a public company, the secretary must have certain prescribed qualifications, as set out in the Law. A sole director cannot also be the company secretary.

Particulars of the secretary must be maintained in a register kept by each company and open to inspection by members of the company and by the Registrar. The Registrar may not disclose information on the register except for the purpose of enforcing any provisions of the Law or any obligation owed to the company by secretary.

Each Jersey company must have at least one shareholder. There is no restriction on the nationality or residency of the shareholders. The shareholders can be individuals and/or legal persons.

Unless the Articles of Association provide otherwise, or all members of the company agree in writing, every company is required to hold an annual general meeting in each year, the first of which should take place within 18 months of incorporation. Where annual general meetings are to take place, they must be held no more than 22 months apart in the case of private companies.

There is no requirement for shareholders' meetings to be held in Jersey.

Where membership in a company is held by a body corporate, the body corporate may appoint any person to attend any meeting and vote on its behalf.

The Government of Jersey has passed a law establishing a central registry of beneficiaries and controlling persons in 2020.

The opening date of the Beneficiary Registry was scheduled for May 31, 2021. For now, however, the Registry is not public.

The Beneficiary Registry will not contain data on minors, company secretaries, etc. In addition, for the time being, limited liability partnerships are exempt from the obligation to submit information about their beneficiaries to the Registry.

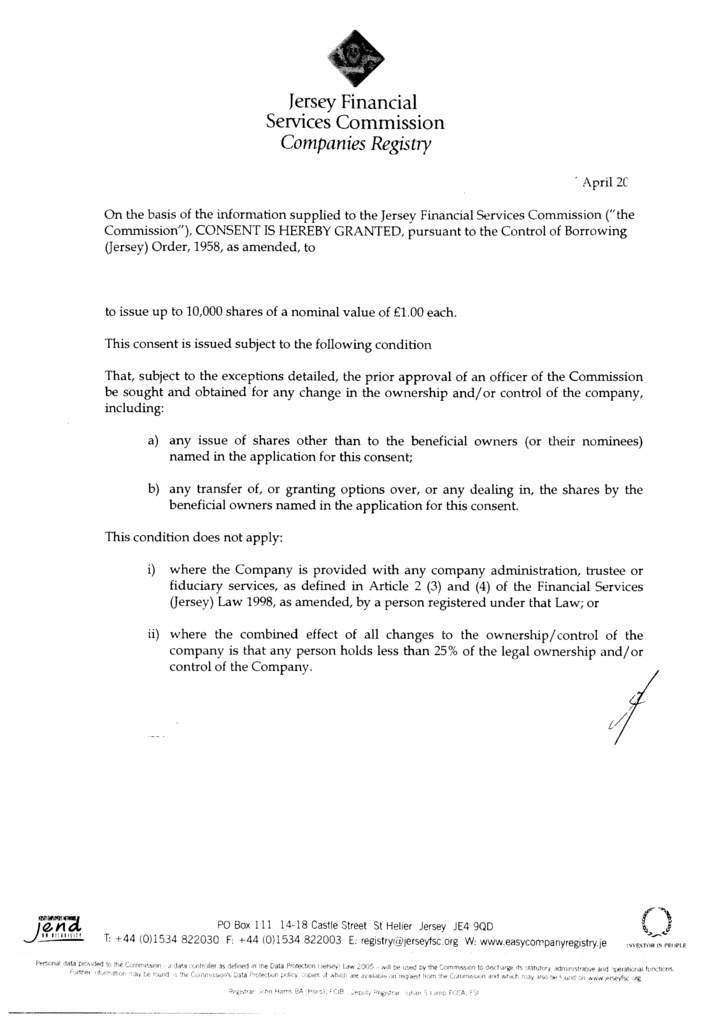

A beneficiary is any natural person who ultimately owns (directly or indirectly) a sufficient percentage of the shares or voting rights or ownership interest (generally 25% or more, but the exact amount is determined by the laws of the country individually) or controls the company or the natural person on whose behalf the transaction or activity of the company takes place.

Jersey companies may be incorporated with a share capital denominated in any currency, may allot shares at different prices, convert par value shares into no par value shares (and vice versa) and accept a member with wholly or partly paid up shares.

The usual authorized share capital is GBP 10 000 or its foreign currency equivalent, although issued capital may be nominal e.g. GBP 1. Stamp duty is payable on higher amounts of capital. All issued shares must be paid in full in cash.

Pricefrom USD 14 500

including incorporation tax, state registry fee, NOT including Compliance fee

Priceincluded

Stamp Duty and Companies Registry incorporation fee

Pricefrom USD 10 340

including registered address and registered agent, NOT including Compliance fee

PriceUSD 275

DHL or TNT, at cost of a Courier Service

Pricefrom USD 865

PriceUSD 780

Paid-up “nominee director” set includes the following documents

PriceUSD 585

Paid-up “nominee shareholder” set includes the following documents

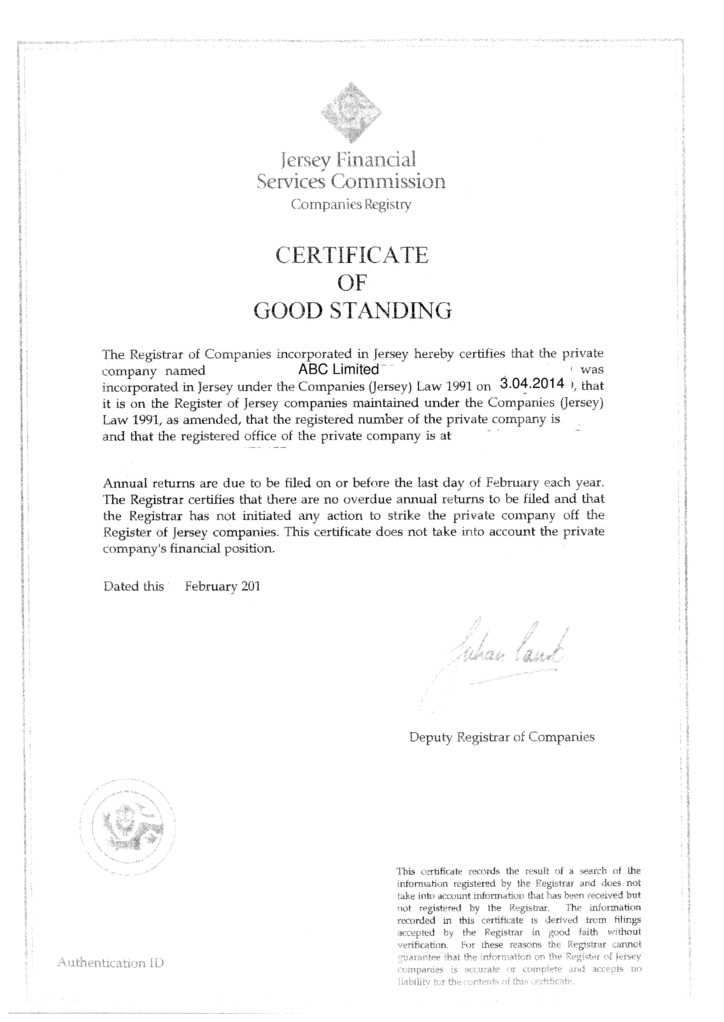

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

PriceUSD 275

simple company structure with only 1 physical person

PriceUSD 165

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

PriceUSD 220

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

PriceUSD 385

PriceUSD 110