The Maltese legal system is a hybrid system containing elements of both English common law and Roman civil law. English legal principles are very influential in public and commercial law, especially in shipping and company law. However, the system of judicial precedents does not apply: judges are not bound by previous case law, though much weight is attached to these decisions.

The principal forms of business organization in Malta are:

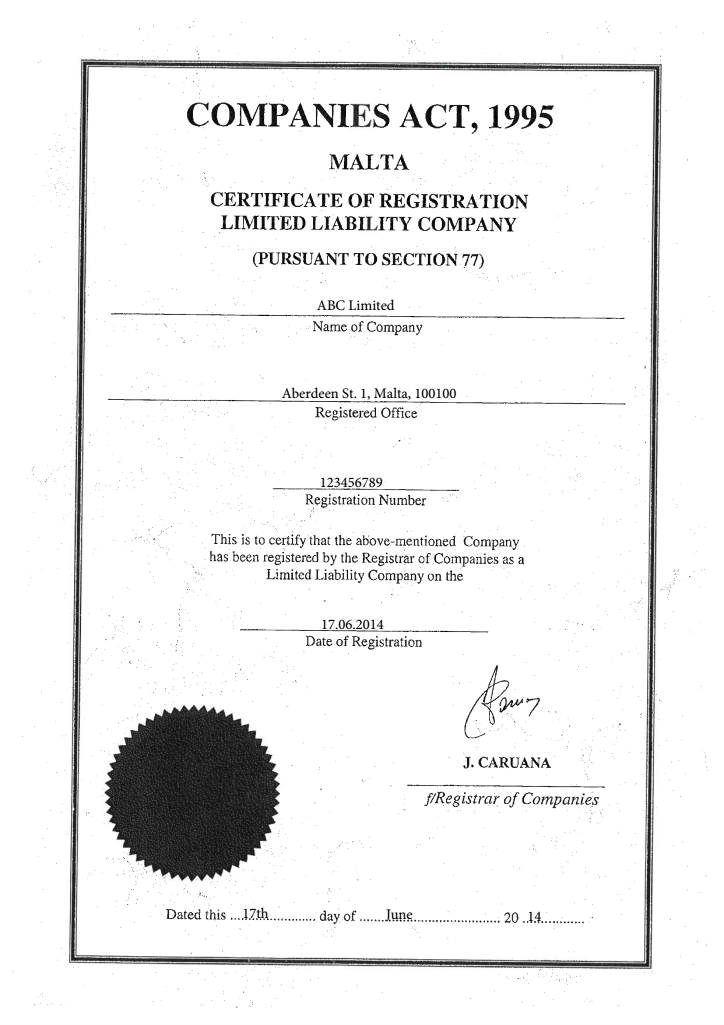

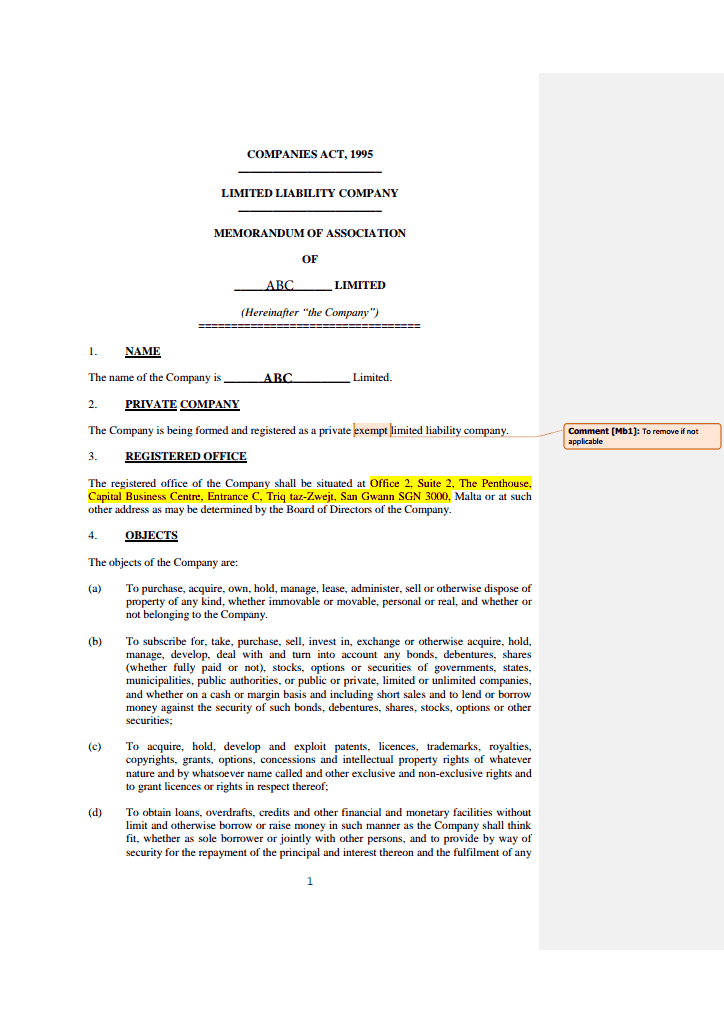

The most common structure is the private limited liability company.

A private company may be designated by any name, but such name shall end with the word ‘limited’ or its abbreviation ‘ltd’. Company names may be expressed in any language using the Latin alphabet. Names in Cyrillic alphabet are not allowed. A company may not be registered with a name which is the same or so similar that in the opinion of the Registrar it could create confusion, a name which is offensive or otherwise undesirable, or has been reserved for registration of another company by written notice to the Registrar (names may be reserved for a period of up to 3 months). The following elements of the name, their abbreviations, contractions or derivatives or foreign language equivalents require permit or authorisation from a competent authority: Fiduciary, Nominee, Trustee.

The procedure of the registration of a private limited liability company in Malta is as follows:

The Registry timescale to incorporate a new company is 2-3 days. The timescale for a new turnkey entity is about one month.

There are a number of restrictions imposed on the activities of Maltese companies. They, for example, cannot undertake insurance business, provide investment services or other financial services, or carry on gaming activities, unless a license is granted.

Maltese companies may open accounts with banks both within and outside Malta.

Maltese companies must maintain a registered office in Malta. This may be at the office of a firm of lawyers, accountants or other providers of corporate services. Any changes to the company's registered office must be notified to the Registrar of Companies. The following information and documents should be kept at the registered office: original certificate of registration, register of members, minute book of general meetings of the company, minute book of meetings of the board of directors, and accounting records. The registers and books containing minutes can be kept at such other place as may be specified in the company’s memorandum or articles. The accounting records can be kept at such other place as directors may think fit, however if they are kept outside Malta, there still must be sent to and kept in Malta such accounts and returns with respect to the business dealt with in the accounting records that will disclose the financial position of the company and will allow to prepare its financial statements.

There are no statutory requirements for a Maltese company to have a seal.

Maltese companies are renewed annually and the renewal normally includes: payment of fees for nominee directors and shareholders (if any), secretary, registered office and government fee for filing with the Registrar of an Annual Return containing the details of registered office, directors, secretary, shareholders, and share capital or changes in the same (the annual fee is calculated in accordance with the authorised share capital of the company).

Under the Continuation of Companies Regulations 2002, which came into force in 2002, foreign-registered companies can be redomiciled to Malta by pursuing a procedure outlined in the law. It is also possible for Maltese companies to choose to redomicile out of Malta.

A Maltese company is required to have a minimum of one director, corporate or individual. There is no legal requirement that the directors be Malta residents.

Director’s details (adress and passportdetails) are disclosed to the local agent and appear on the public file.

There are no requirements to directors’ meetings.

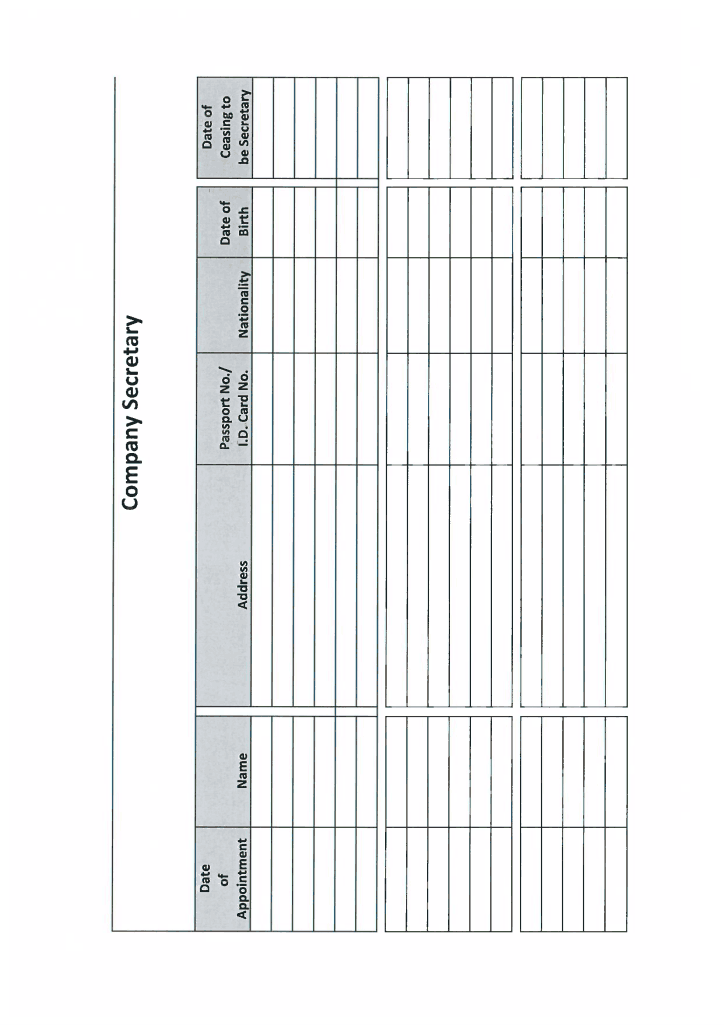

All Maltese companies must appoint a company secretary who should be an individual, a resident or non-resident. There are no special requirements for qualifications of the secretary. The law prohibits appointing as secretary the sole director of the company. Besides, if a company already has as secretary a sole director of a body corporate, then such body corporate cannot be appointed the sole director of the company. However, in the case of a private exempt company, the sole director is entitled to hold office of company secretary during the entire period of his directorship. One of the shareholders can serve as a secretary.

Maltese companies normally require two shareholders, individuals or corporations of any nationality or residence. Maximum number of shareholders is 50. A private exempt company may have just one shareholder. Such single member company must specify in the objects clause of its memorandum the activity which will constitute its main trading activity, and the company’s business must consist principally of that activity.

An individual shareholder can be a secretary and director at the same time.

Shareholders’ details are disclosed to the local agent and appear on the public file.

General meetings are to be held either in Malta or abroad annually, with the first annual general meeting to take place within eighteen months of the company’s incorporation. It is important that not more than 15 months elapse between the date of one AGM and another.

Malta has introduced a beneficial ownership register in 2018.

All companies registered in Malta must provide beneficiary information at the time of registration. If the information is not submitted or if false information is submitted, the officer, shareholder or beneficiary may be fined up to EUR 5,000 or imprisoned for up to 6 months.

Information to be submitted to the Registry:

Part of the information from the Registry of Beneficiaries is public. However, in exceptional cases beneficiary information may be classified. This is due to the risk of fraud, extortion, harassment, violence, intimidation, etc. or if the beneficiary is a minor or incompetent.

In November 2022, the Maltese authorities decided to temporarily suspend public access to the register of beneficiaries under the EU Court of Justice (CJEE) Decision in consolidated cases C-37/20 and C-601/20 of November 22. The Court ruled that Article 1, paragraph 15(c) of Directive (EU) 2018/843 of the European Parliament and of the Council of 30 May 2018, which provides for access to information on the beneficiaries of legal persons for any member of the public, was invalid as it constituted a serious interference with the fundamental rights to respect for privacy and to the protection of personal data enshrined in Articles 7 and 8 of the EU Charter of Fundamental Rights.

The share capital of a private limited liability company can be denominated in any convertible currency. The minimum authorized and issued share capital is EUR 1,165. Where the authorised share capital is equal to the minimum stipulated by law, it must be fully subscribed in the memorandum.

Usually the share capital is EUR 1,200 which is divided into shares of EUR 1 each.

Bearer shares or shares with no par value are not permitted.

A company may wind up:

Voluntary Winding Up

To liquidate a company voluntarily, a company has to pass an extraordinary resolution resolving to be dissolved. A company may decide to liquidate for any reason. Either from the date of such resolution or from a later date fixed in it, the company goes into dissolution and must ceases to carry on its business, except so far as may be required for the beneficial winding up. The resolution is then passed within 14 days to the Registrar of Companies for registration, subsequently published on the Registry’s website and in a daily newspaper. The resolution must be accompanied by a declaration of solvency, which is a declaration made by the directors before the passing of the resolution, stating their belief that the company will be able to pay its debts in full within one year from the date of dissolution. A winding up in relation to which a solvency declaration has been made by the directors is called a members’ voluntary winding up, and a winding up in relation to which such declaration cannot be made is called a creditors’ voluntary winding up.

Within one month after the date of dissolution, the company would then have to appoint a liquidator for the purpose of winding up the affairs of the company and distributing its assets.

Once the affairs are fully wound up, the liquidator then draws up a scheme for the distribution of the company’s assets. This is then audited, either by company appointed auditors, or failing that, by auditors appointed by the Court. When the affairs of the company are fully wound up, the liquidator must call a general meeting of the company to lay before the shareholders information concerning the winding up, the auditor’s report and the scheme of distribution. Within seven days of this meeting, the liquidator must send these documents together with a return relating to the holding of the meeting to the Registrar of Companies, who is entrusted with registering and publishing them. Three months after publication, the Registrar strikes the name of the company off the register unless interested parties have objected before the Court.

Winding Up by Court

The court may order the dissolution of a company where:

Where company is dissolved by court, Registrar of Superior Courts shall forward copy of winding up order to Registrar for registration.

Any interested person may by application to Court within five years from the strike off date request that the name of the struck off company be restored to the register and the winding up be reopened. If the Court is satisfied that the winding up and striking off has been vitiated by fraud or illegality of material nature, it may order the restoration of the company name to the register and reopening of winding up for such purposes and such period as the court will specify in its decision. It should be noted that the Court will only accede to application for restoration if it is satisfied that this is the only remedy available.

Price6 050 EUR

including incorporation tax, state registry fee, NOT including Compliance fee

Priceincluded

Stamp Duty and Companies Registry incorporation fee

Price4 190 EUR

including registered address and registered agent, NOT including Compliance fee

Price220 EUR

DHL or TNT, at cost of a Courier Service

Pricefrom 940 EUR

Price5 060 EUR

Paid-up “nominee director” set includes the following documents

Price7 810 EUR

Paid-up “nominee shareholder” set includes the following documents

Price800 EUR

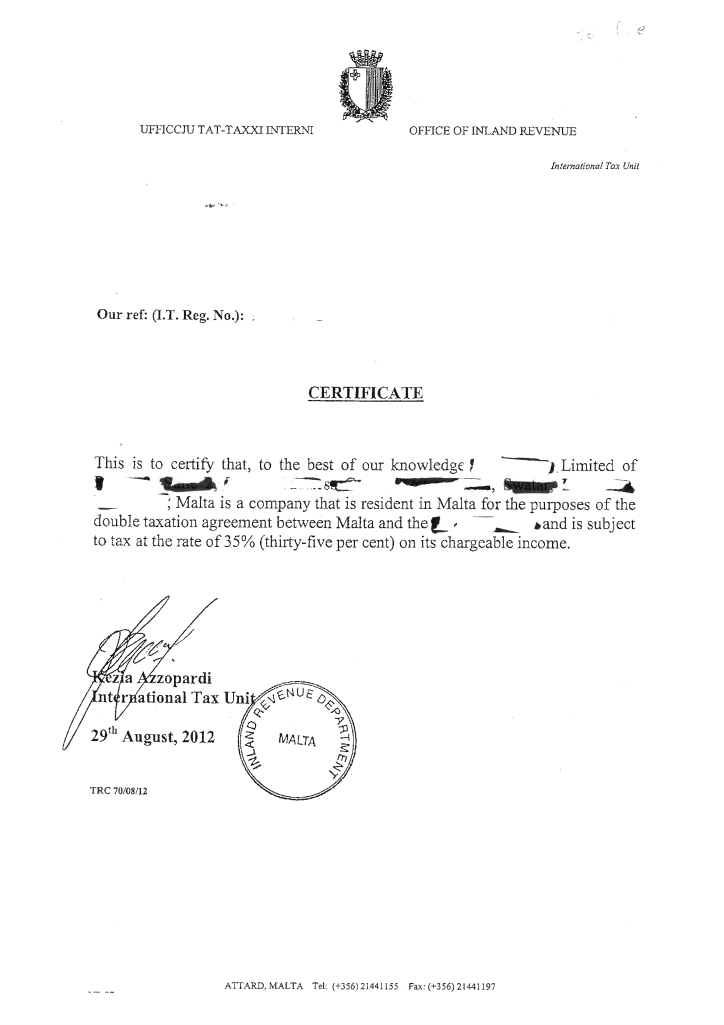

Company’s tax residence certificate for access to double tax treaties network

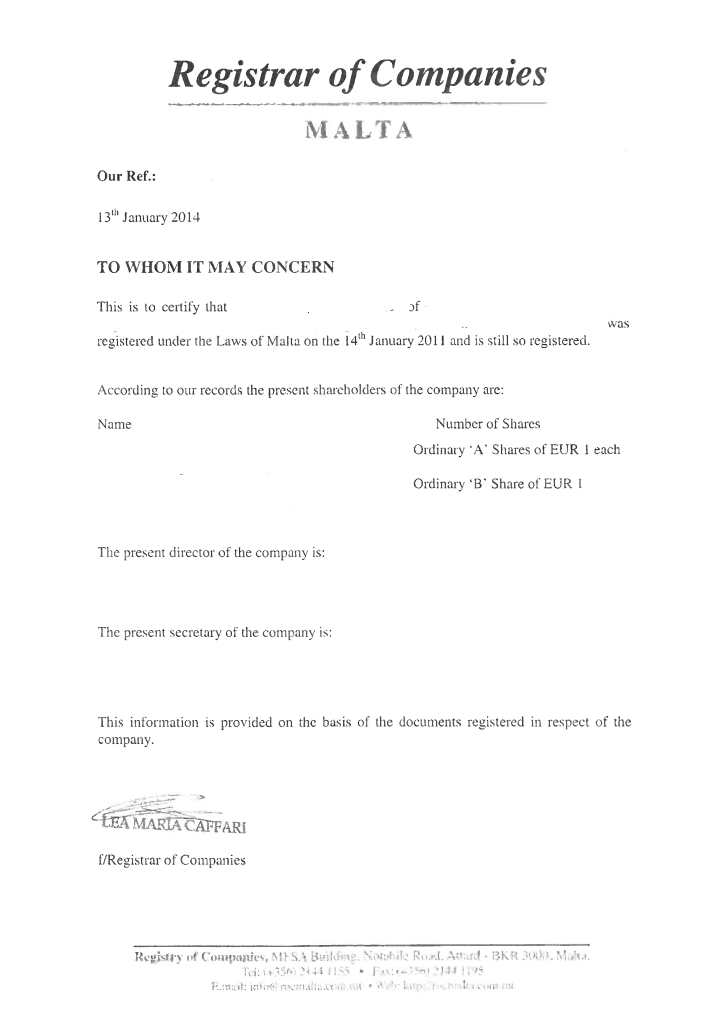

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: In the case of incorporating a company with more than one BO / officer; change of director / shareholder / BO (except the change to a nominee director / shareholder), issue of a power of attorney to a new attorney. Incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price850 EUR

In the case of incorporating a company with more than one BO / officer; change of director / shareholder / BO (except the change to a nominee director / shareholder), issue of a power of attorney to a new attorney; in other cases please see below

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR