The legal system of New Zealand is based on English common law.

There is no codified Constitution in New Zealand, but there are some constitution acts.

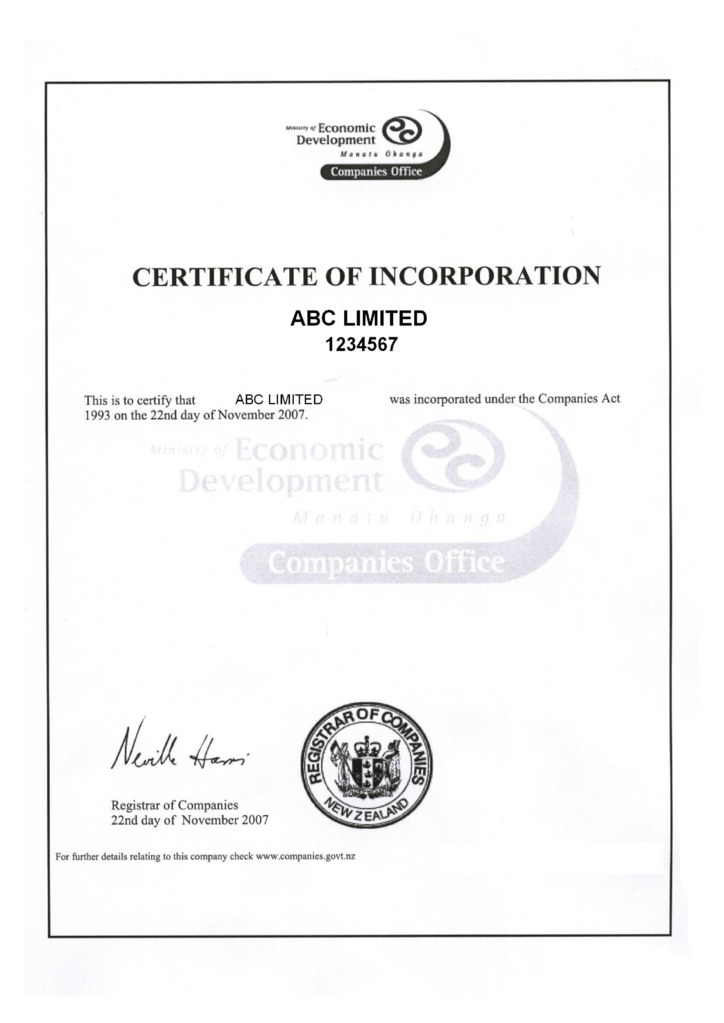

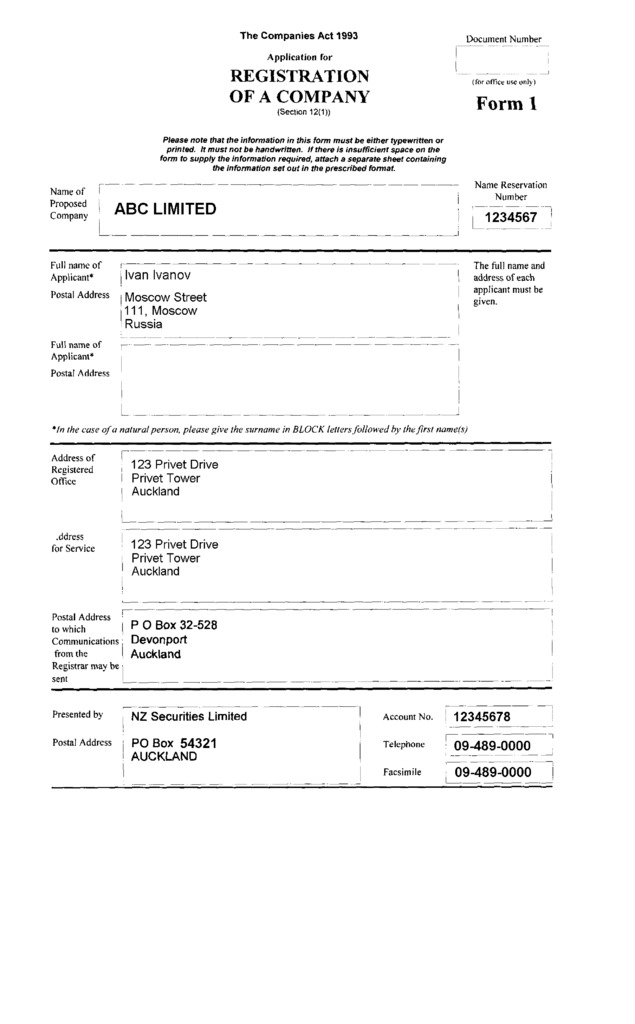

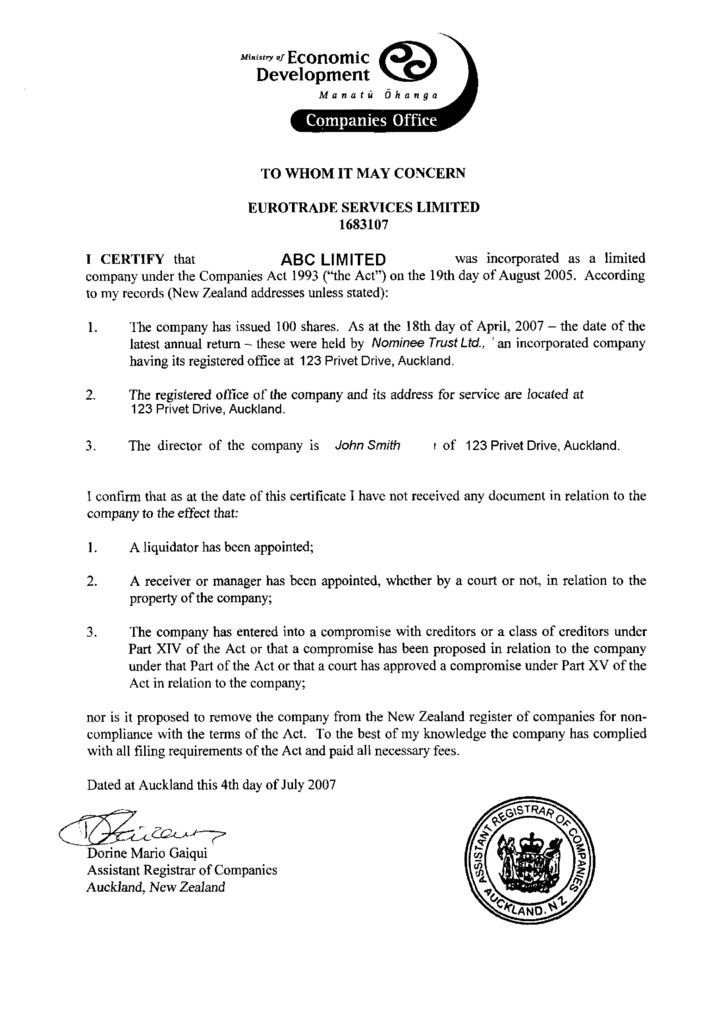

Companies in New Zealand are governed by Companies Act 1993.

The principal forms of business organization in New Zealand are:

The most common structure is the private limited liability company.

There is a range of requirements to the company name in New Zealand:

The following steps are required to incorporate a GmbH in New Zealand:

The formation of a new company in New Zealand takes 1 day.

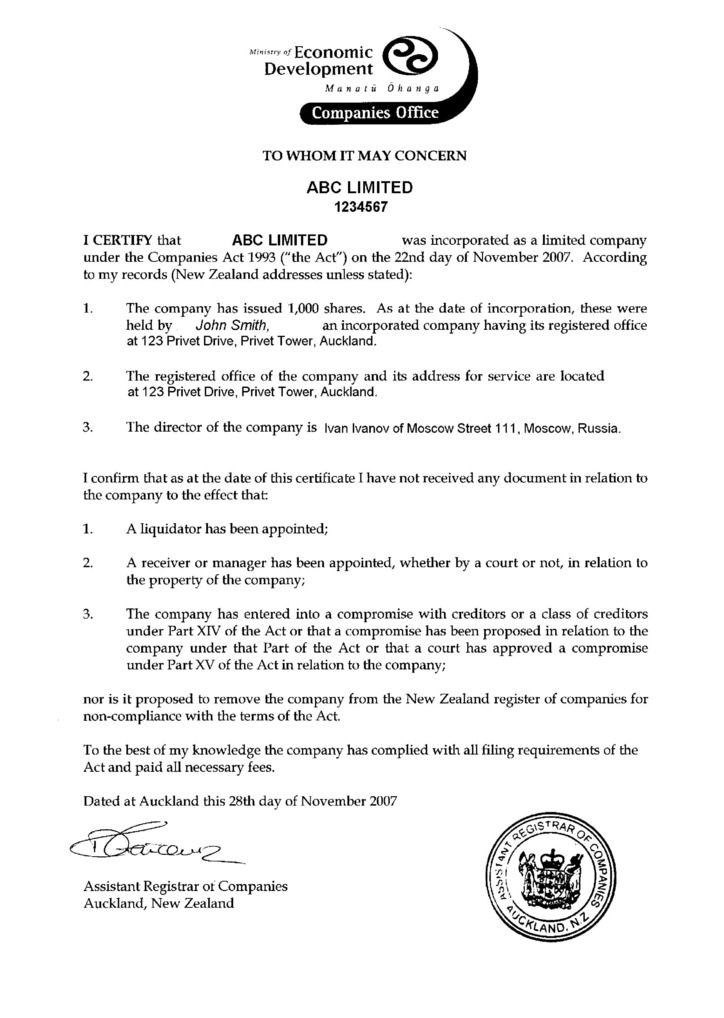

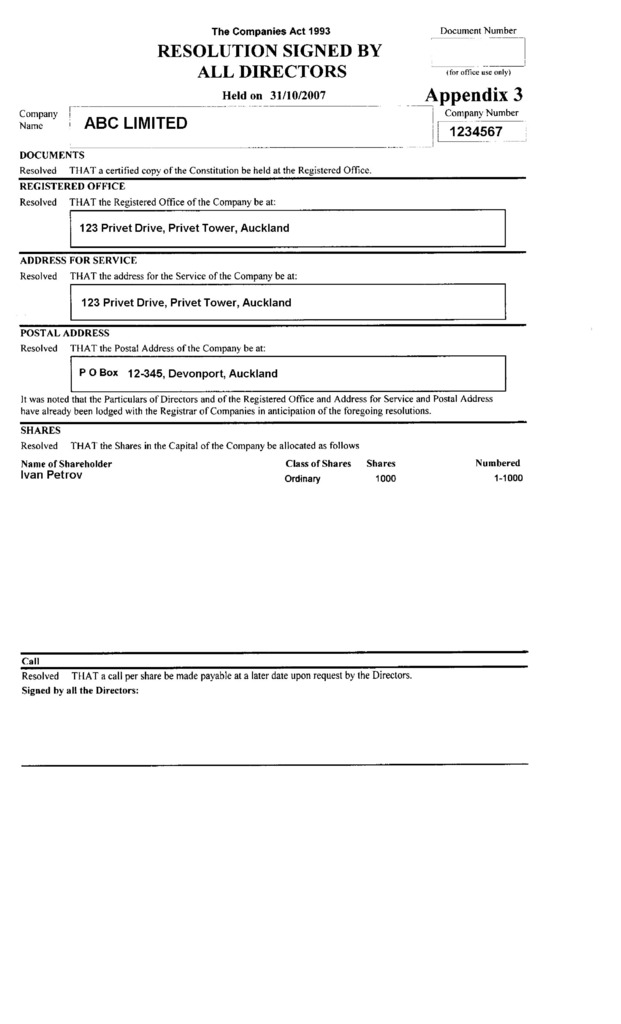

Each company in New Zealand must have a registered office, an address for service, and an address for communication. The address of the registered office and the address for service must be physical addresses in New Zealand. That is, a street address, not a Post Office Box or DX address. The address for communication may be a postal or physical address (but not a DX) and must include an email address.

The companies office requires the following to be stored at the registered office:

All records must be held and updated regularly for the past seven years.

There are no statutory requirements for a company in New Zealand to have a seal.

The redomiciliation of companies to or from New Zealand is permitted.

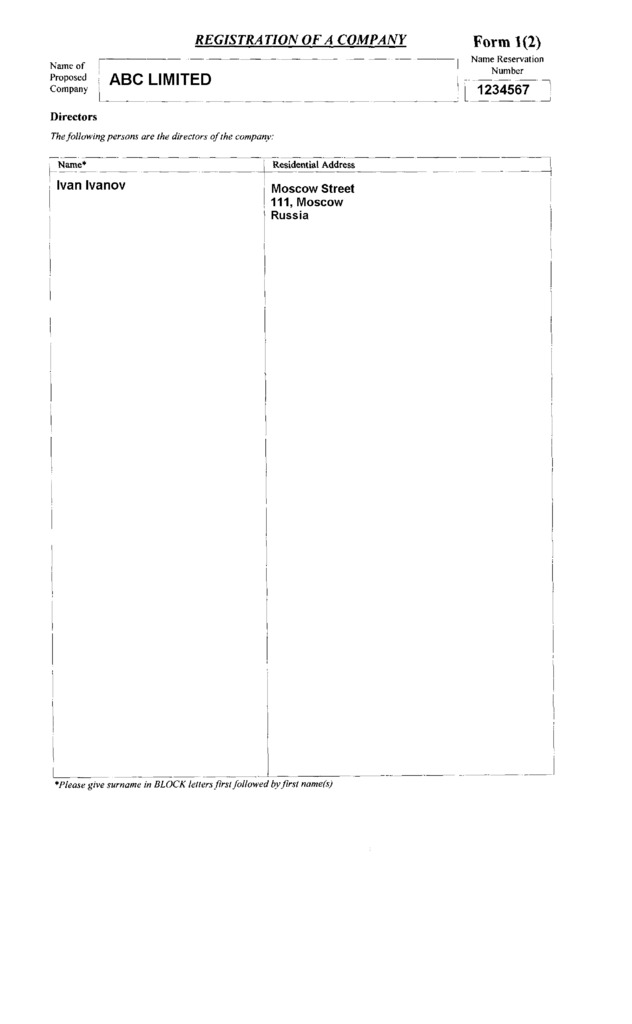

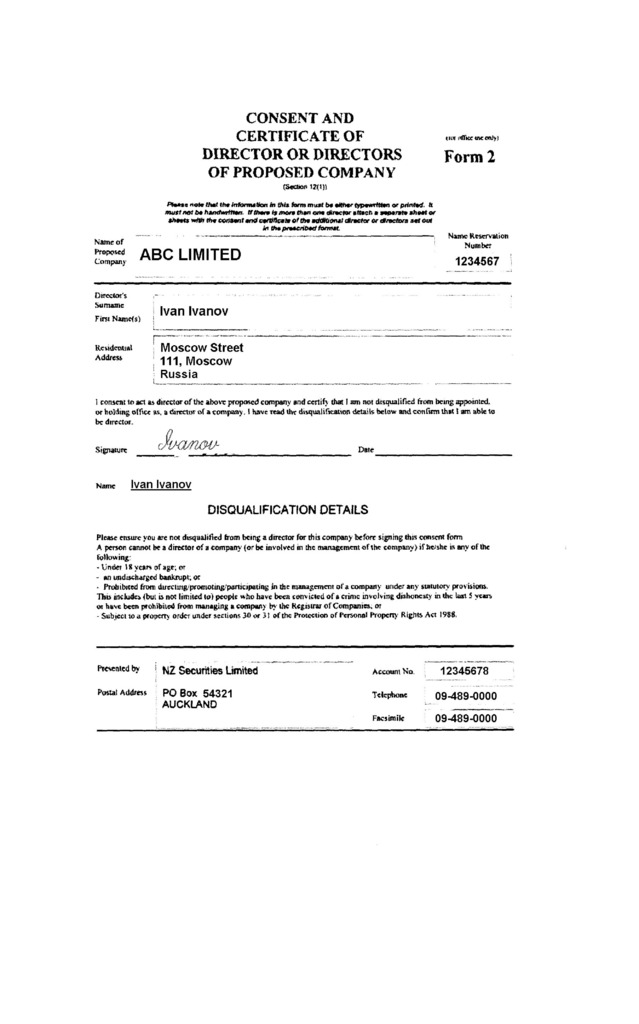

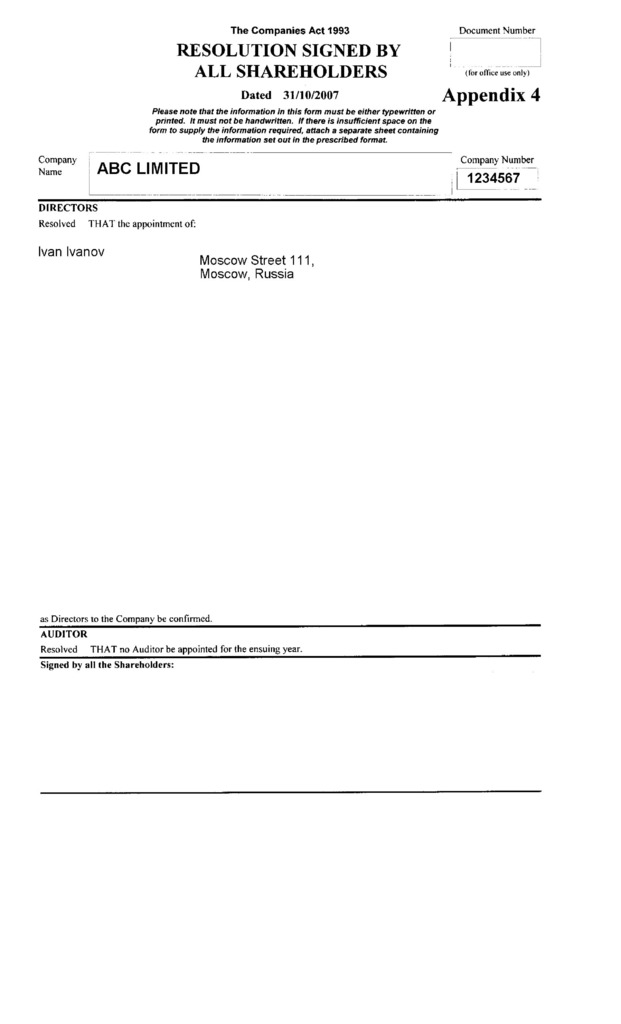

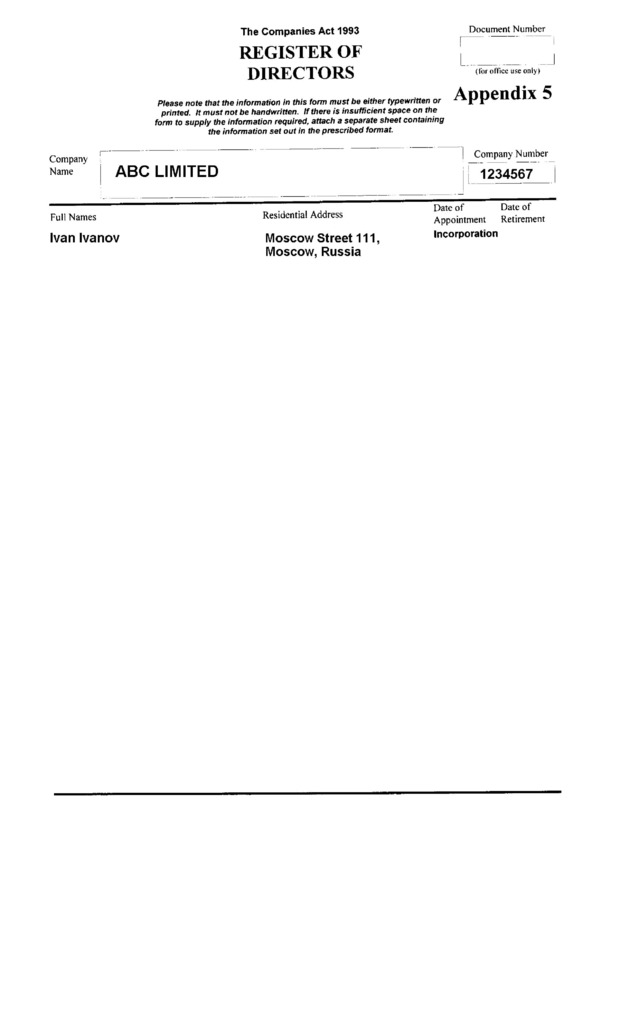

Every company in New Zealand must have at least one director. A director must be a natural person. There are no requirements to the residency of directors. A person cannot be a director of a company if they are:

However, from 1 May 2015, New Zealand companies must also have at least one director who lives in New Zealand or who lives in an enforcement country (currently Australia only) and is a director of a company in that country.

Directors’ information appears on public record.

A meeting of the board may be held either by a number of the directors who constitute a quorum, being assembled together at the place, date, and time appointed for the meeting; or by means of audio, or audio and visual, communication by which all directors participating and constituting a quorum can simultaneously hear each other throughout the meeting.

New Zealand companies are not required to appoint a company secretary.

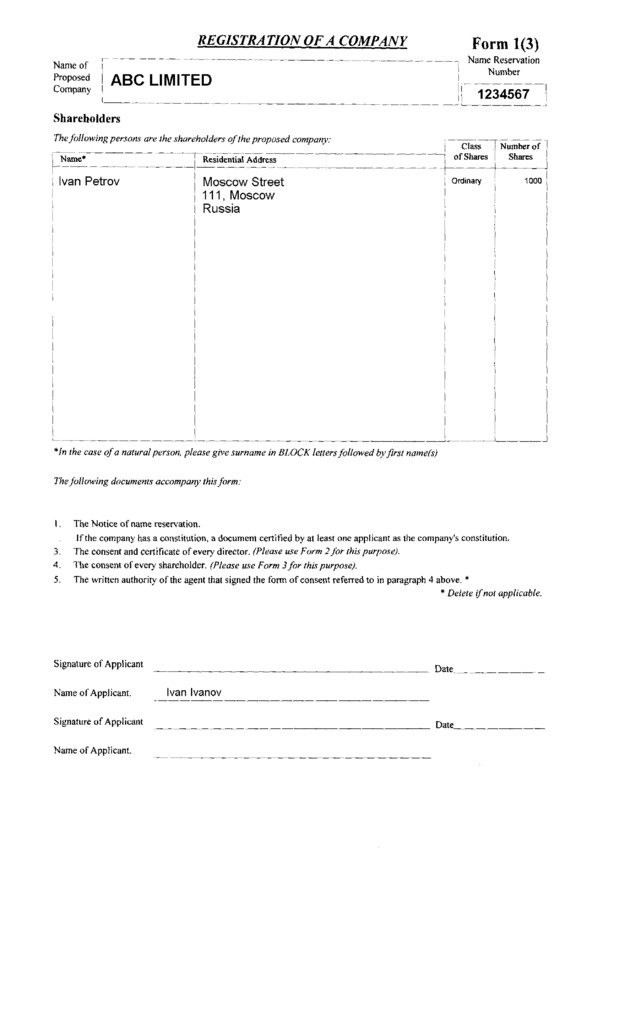

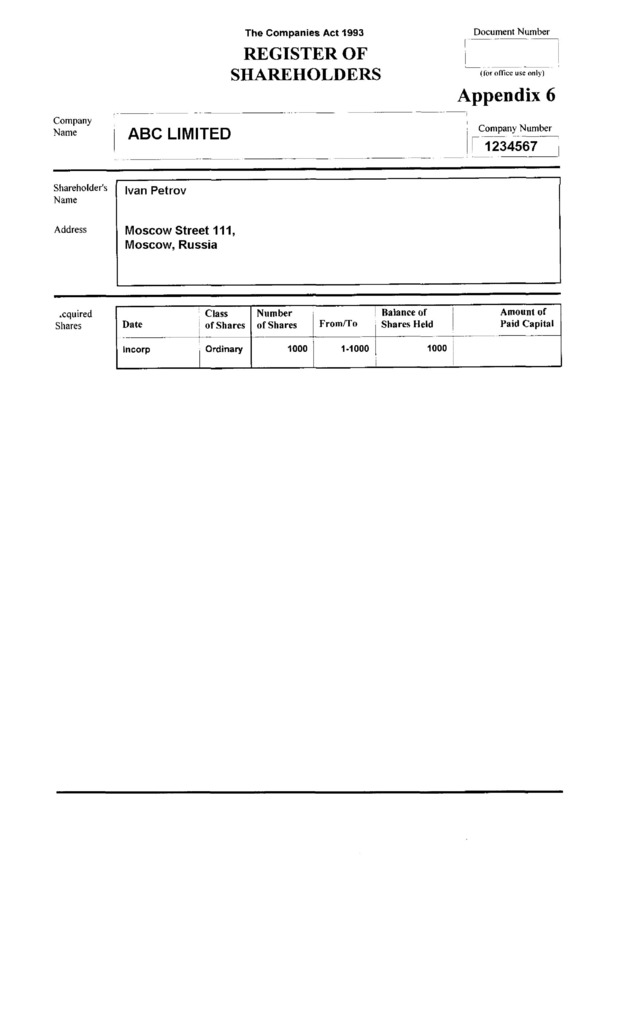

Each company in New Zealand must have at least one shareholder. There is no restriction on the nationality or residency of the shareholders. The shareholders can be individuals and/or legal persons.

Each shareholder is on public record.

The board of a company must call an annual meeting of shareholders. A company does not have to hold its first annual meeting in the calendar year of its reregistration but must hold that meeting within 18 months of its registration. The following meetings should be held not later than 15 months after the previous annual meeting. Meetings may be held in or outside of New Zealand.

The details of the beneficial owner are not available on public record.

There is no specific minimum capital requirement. The usual minimum authorized capital is NZD 100. The minimum issued capital may be one share without par value. Issued shares must be fully paid. Registered shares, preference shares, redeemable shares and shares with or without voting rights are permitted.

Shares must not have a nominal or par value. Bearer shares are prohibited.

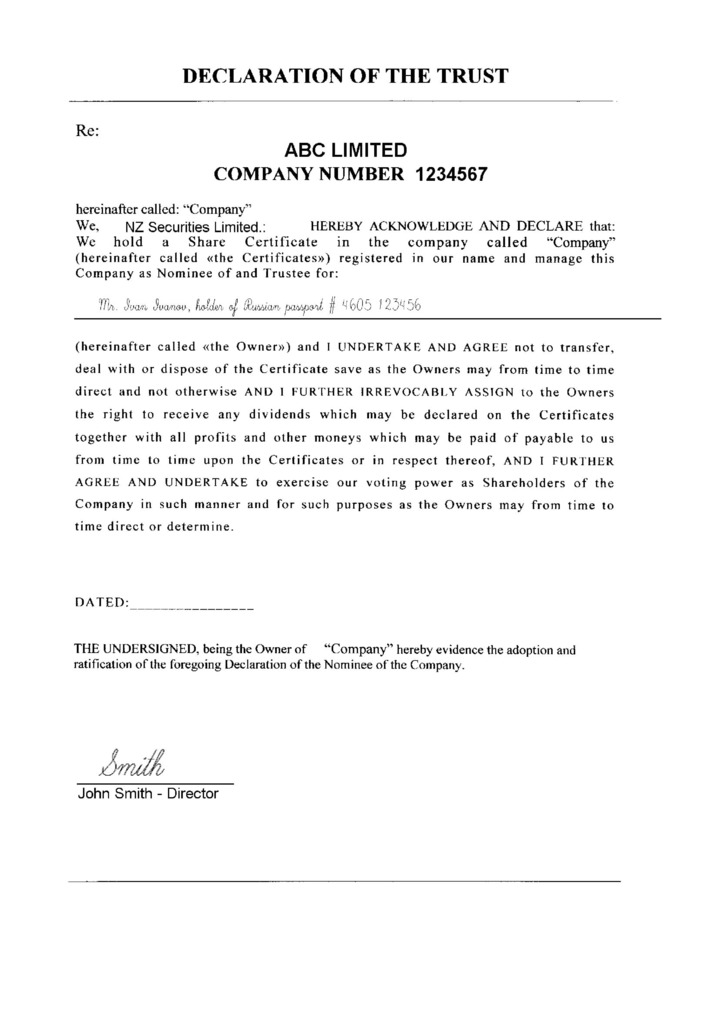

A trust is a legally binding arrangement whereby a person (the "settlor") transfers assets to another person (the "trustee") who is entrusted with legal title to the trust assets, not for the trustee's own benefit, but for the benefit of other persons (the "beneficiaries").

The instructions from the settlor to the trustee as to the distribution of trust assets will normally be contained in a document called the trust deed. The trust deed will usually provide that the trustee has the power to manage and distribute the trust assets in accordance with the terms of the trust deed and the high standards of prudence imposed on trustees under NZ law.

It is also common for a settlor to express to the trustee his wishes as to the management and distribution of the trust fund in a less formal manner. This expression is often contained in a letter of wishes which, although not legally binding, will generally be considered by the trustee to be of persuasive effect when performing the duties of trusteeship which include the distribution of the trust fund to beneficiaries.

Among the most common types of trust are the following:

The discretionary trust provides maximum flexibility and is the most widely used and, often, the most effective solution for both settlor and beneficiaries. Under the terms of a discretionary trust the trustee is given wide discretionary powers as to when, how much and to which beneficiaries the income and capital of the trust should be distributed. Such a form of trust is useful where at the time of creation of the trust the future needs of beneficiaries cannot accurately be determined and are likely to change over time. The beneficiaries are not regarded as having any direct legal rights over any particular portion of the trust fund but only a right to be considered to benefit when the trustee exercises his discretion.

Under a fixed interest trust a named beneficiary will normally be granted a vested interest in the income of the trust fund for life. For example, the trust deed may specify that the trustee is required to distribute all of the income of the trust fund to a particular individual during that person's lifetime and subsequently to distribute the capital of the trust fund in fixed proportions to named beneficiaries (such as the settlor's children).

An accumulation and maintenance trust is one where no beneficiary has a fixed entitlement to the benefits accruing to the trust for a certain period, during which time income is accumulated and becomes part of the capital. The beneficiaries may therefore benefit from the accumulation of capital. The trust deed may give the trustee a discretionary power to make distributions amongst the beneficiaries up to a specific age for their education, maintenance and benefit and to provide thereafter for a designated share of the trust fund to be distributed to each of them on attaining a specified age. An accumulation and maintenance trust may be particularly appropriate where the settlor wishes to benefit a group of children, for example, grandchildren wishing to study at university.

Although for tax and other reasons it is generally desirable for a trust to be constituted as an irrevocable settlement, in certain circumstances the settlor may require the additional comfort of retaining the power to revoke the trust and enforce the return of the trust fund.

Generally, in order for a trust to be valid there must be identifiable beneficiaries who can enforce the duties against the trustees. An exception to this general rule has permitted trusts to be established in favour of charitable purposes. Charitable trusts are often used to further the objectives of philanthropists and not for profit organizations.

It is usual for a trust to be created by the execution of a formal written deed. Trusts created in writing may be either by a settlement of trust signed by both the settlor and the trustee, or by a declaration of trust signed by the trustee alone. Following execution of the trust deed a trust will come into existence upon settlement of the initial property, which may be supplemented later.

The trust relationship is comprised of a number of important components, some of which are essential and others not.

Once a trust is created the settlor will no longer be the legal owner of the trust assets. The settlor may be a beneficiary and he may also act as a co-trustee or protector and, in such capacity, retain a degree of control over the trust, such as the power to approve distributions, the power to appoint and remove trustees and the power to revoke the trust.

However, a settlor may reserve to himself certain powers or grant such powers to a protector. These may include the powers to revoke, vary or amend the terms of a trust, to distribute income or capital, to appoint or remove any trustee or beneficiary, and to change the governing law of the trust.

Legal title to the trust assets is vested in the trustee under the obligations imposed by the trust deed and from then on the trustee is responsible for the management of the trust. A trustee must exercise his powers solely for the benefit of the beneficiaries and the trust assets do not form any part of the trustee's own estate or property available to any creditors of the trustee.

The beneficiaries are the persons entitled to benefit from the assets held on trust by the trustee. The settlor may be one of the beneficiaries. An express power for the addition of further persons to the class of beneficiaries may be included in the trust deed. The beneficiaries may enjoy equal or unequal benefits, as specified in the trust deed, or, in the case of a discretionary trust, as the trustee may determine. It is also possible to include in the trust deed a power to exclude certain people from benefiting under the trust.

There are no restrictions on the type of assets which may be held in trust and further assets may be added from time to time. It is normal to establish a trust with a nominal initial amount and subsequently to add further assets such as real property, shares or other forms of investment.

NZ trust law recognises and permits the use of a protector to counterbalance the wide discretionary powers conferred on a trustee. Often the settlor will fulfil this role or appoint a trusted friend or professional advisor to act as a protector of the trust. In such cases the consent of the protector will generally be required before the trustee may exercise certain important powers under the trust deed.

NZ trust law permits family advisors, settlors and beneficiaries to influence the exercise of powers by the trustees by the use of a mechanism which separates powers between custodian trustees, managing trustees and advisory trustees.

These provisions are invaluable tools for the international wealth planner to cut across time zones and appease settlors unwilling to cede complete control to foreign trustees.

For example, a NZ resident custodian trustee could hold the assets whilst discretionary investment management could be delegated to an investment firm in Zurich. Meanwhile, a trusted family advisor resident in the jurisdiction in which the settlor resides could hold office as advisory trustee. The management and administration of the trust could be exercised by a managing trustee based in Jersey or under a delegated administration agreement. All transactions would be implemented by the NZ resident custodian trustee which would also retain the power to review directions given.

The range of uses to which a trust may be employed is widespread and constantly evolving but flexibility and confidentiality are the principal advantages which a trust has over other legal forms designed to hold, preserve and transfer wealth. The trust concept has proved to be enormously adaptable and is widely used in financial planning including:

Aside from use in structuring personal and family wealth NZ trusts can also be used for the following commercial purposes:

Where the settlor of the trust is resident outside NZ the trust will be exempt from assessment in respect of NZ tax on income and capital gains arising outside of NZ. Accordingly, the trustee may make distributions out of a trust fund established in NZ without any withholding or deduction for NZ income or capital gains tax. There are no inheritance, wealth or capital gains taxes levied in NZ nor is there any gift duty, stamp duty, value added tax or equivalent forms of indirect taxation charged on the creation or transfer of assets to a trust by a non-resident of NZ.

There are minimal reporting requirements to the Inland Revenue.

Price3 900 USD

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Companies Office incorporation fee

Price1 770 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 600 USD

Price3 950 USD

Paid-up “nominee shareholder” set includes the following documents

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD