The Austrian legal system is based on the civil law tradition and has its origin in Roman law.

The principal forms of business organization in Austria are:

- Sole proprietorship;

- General Partnership;

- Limited Partnership;

- Limited Liability Company, GmbH;

- Joint Stock Company, AG;

- European Company, SE;

- Branch of Foreign Company;

- Private Foundation.

Except GmbH another common structure is the joint stock company, AG.

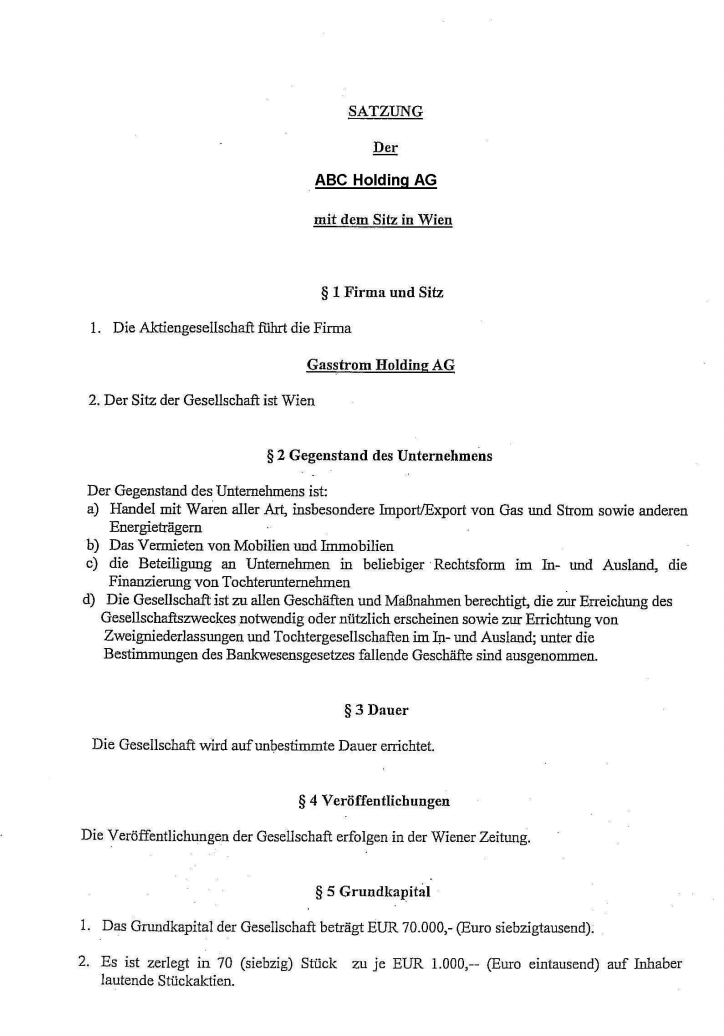

Every company in Austria must have a name. Company name requirements for AG are as follows:

- A company name should not be similar to the existing company names.

- It should contain a mandatory legal element: "Aktiengesellschaft" or AG.

- It should not be obscene.

- It should not be misleading.

- A company name should not contain any prohibited words or phrases, such as Austria, Austrian, etc.

- The name needs to be pronounceable.

To incorporate an Austrian company, the following steps are required:

- Obtain the confirmation from the Economic Chamber that the start-up company is really a new enterprise: A form (Neufö 1 or NeuFö 3), which is available electronically on the homepage of the Austrian Ministry of Finance must be filled in and be confirmed by the Economic Chamber. Procedure 1 is optional but it can lead to exemption from paying certain publicly levied fees and taxes. If certain requirements are met, the following fees and taxes will be waived: stamp duties and certain administrative fees; real estate transfer tax; charges for registration in the commercial register and the cadastral register; capital transaction tax (1% of nominal capital); for 1 year, certain ancillary wage costs borne by the employer in addition to social security contributions.

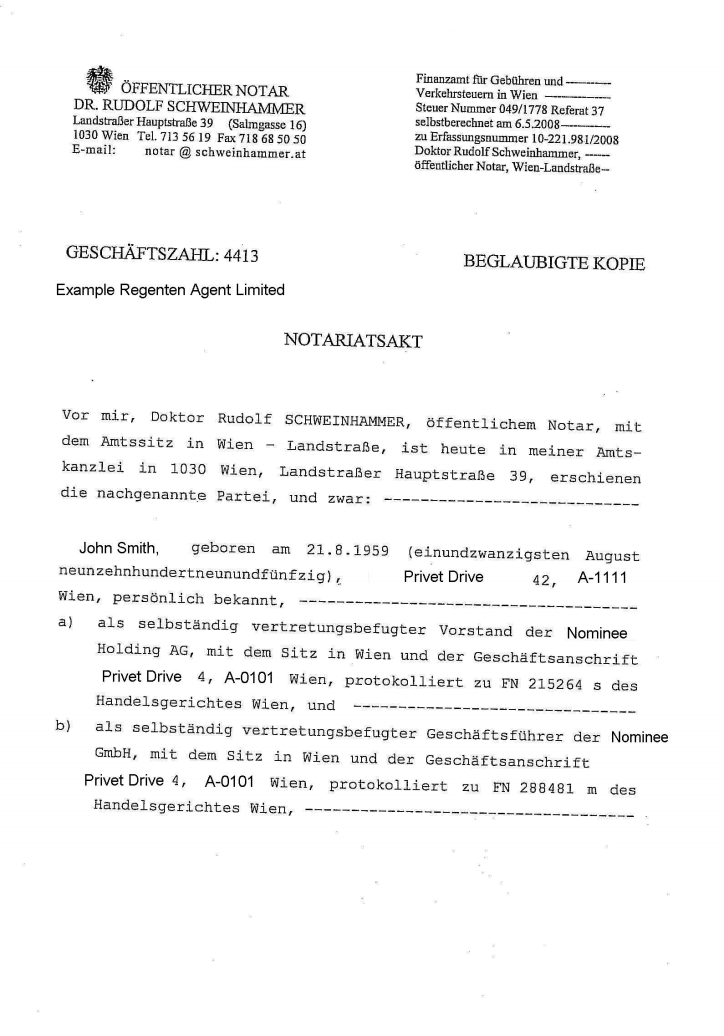

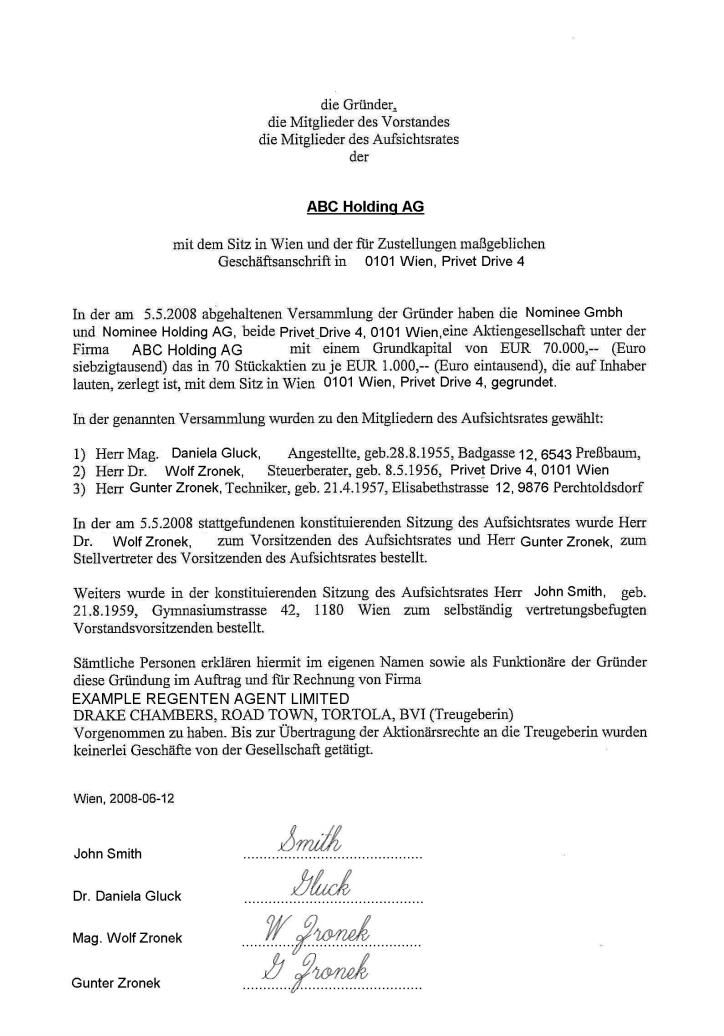

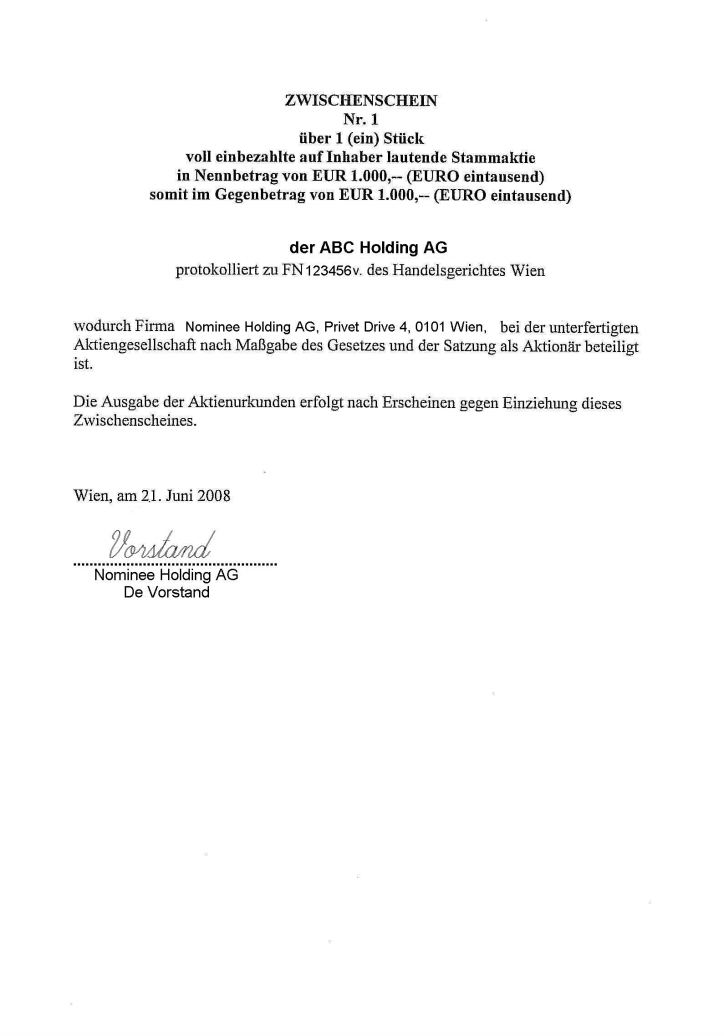

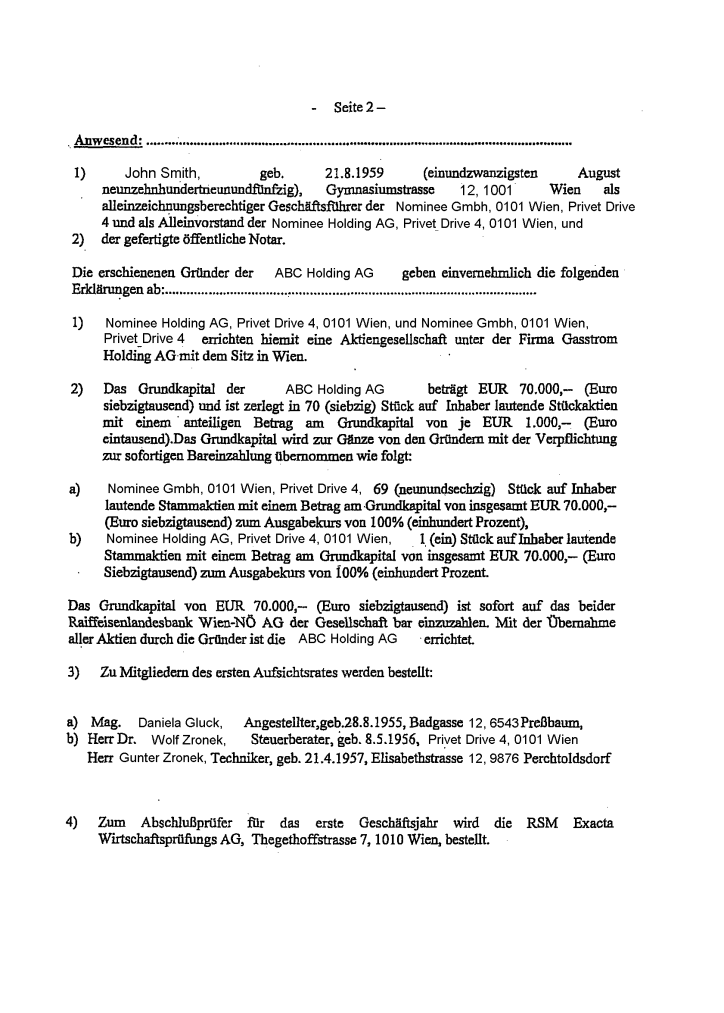

- Notarize the statutes/articles of association or the declaration of establishment: The articles of association (Gesellschaftsvertrag), which must be executed before a notary by notary deed (Notariatsakt), must include the following: name, seat, scope of activities, capital and initial contribution by each shareholder.

- Deposit the minimum capital requirement in the bank.

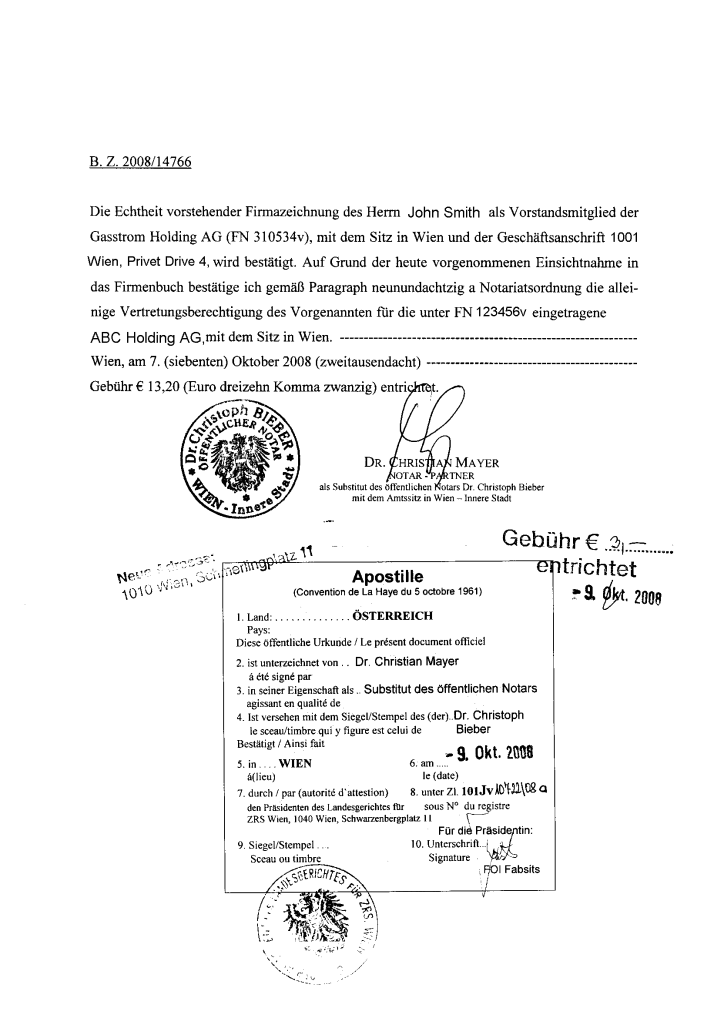

- Register the company at the local court (Handelsgericht) and publish an announcement of formation in the Wiener Zeitung: The application for registering an Austrian AG must be accompanied by the following documents: declaration of establishment notarized; articles of association; a declaration (accompanied by a banker's confirmation) that the demanded amount of primary deposit, to be paid in cash, has been paid; evidence that the free disposability of the paid primary deposit by managing directors is not restricted by counterclaims; specimen signatures of the managing directors; and confirmation by the tax authorities that the capital transaction tax on the formation has been paid or is guaranteed. If the court has doubts about the company name, it may request an opinion from the Chamber of Commerce. A GmbH comes into legal existence upon registration in the commercial registry.

- Tax Office registration (obtain a VAT number): The commercial register automatically informs tax authorities of the registration of new companies. In turn, tax authorities usually respond by requesting that the company file for tax registration. One of the following forms must be filed with the tax authority: Form 15, or 24 (available at www.bmf.gv.at/), and the articles of association, the opening balance sheet, an excerpt of the company register, an identification card of a managing director, a specimen signature sheet of the representatives must be filed as attachments. The authority issues the tax number within 10 to 14 days. The VAT number is usually issued simultaneously with the tax identification number.

- Register trade (Gewerbeanmeldung) with the trade authority (Bezirksverwaltungsbehörde) (simultaneous with previous procedure).

- Register employees for social security (simultaneous with previous procedure).

- Register with the municipality for tax purposes (simultaneous with previous procedure).

The following company information is inter alia listed and published in the commercial registry:

- corporate name,

- registered office and address,

- name and the date of birth of the company´s representatives and shareholders,

- nominal capital.

All Austrian companies must have a registered office. The registered office is where documents may be legally served on the company. The registered office must be a physical address in Austria.

Company records and sharehoders' register should be kept at the registered office.

An Austrian company is not required to have a seal.

The redomiciliation of companies to or from Austria is permitted.

Redomiciliations within the EU or EEA are possible, however based on particular decisions at the EU level. Under Austrian case law of the supreme court, seat transfer of an EEA company to Austria is possible, provided that the company changes its legal form to a company under Austrian law (and fulfills all conditions as to articles of association, capital resources und statutory representatives under Austrian law), the company transfers both the seat pursuant to the articles of association and the seat of administration to Austria, the seat transfer is allowed under the laws of the previous state and the company fulfills the conditions of the previous state. In contrast, the conditions of a seat transfer from Austria have not been clarified yet, but should be possible correspondingly as well. Irrespective of the general possibility of cross border-redomiciliations, the transfer of the registered office requires a notarized shareholder resolution, as it represents an amendment to the articles of association under Austrian law.

As to non-EU or non EEA-countries, redomiciliation to Austria is not possible. If a company seeks to transfer its registered office to Austria, it has to be founded again under Austrian law.

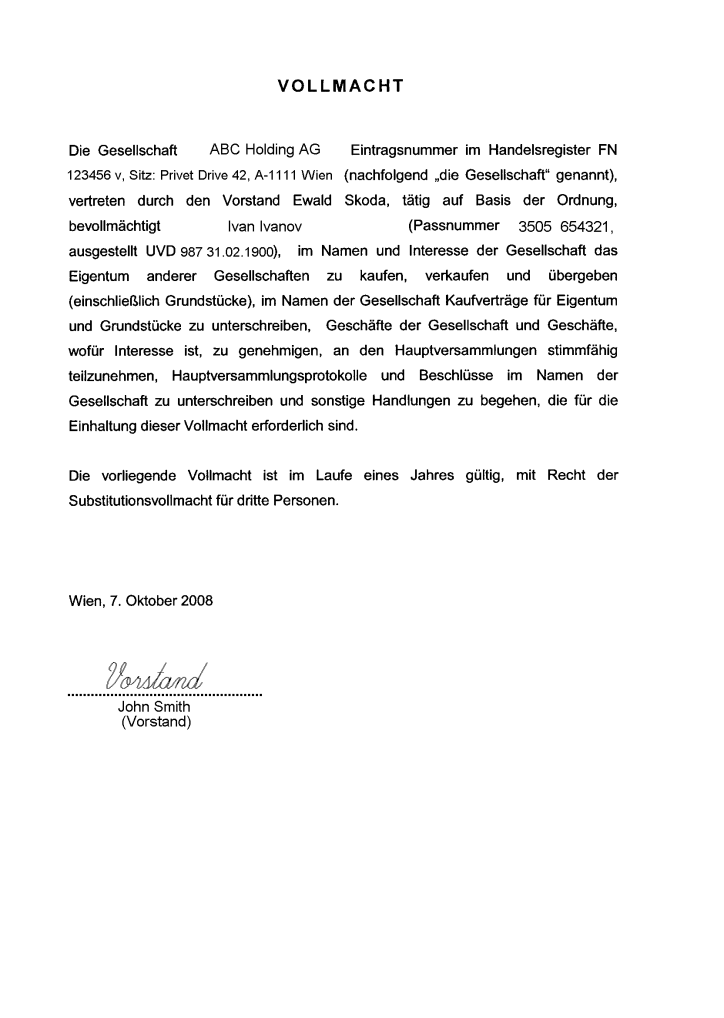

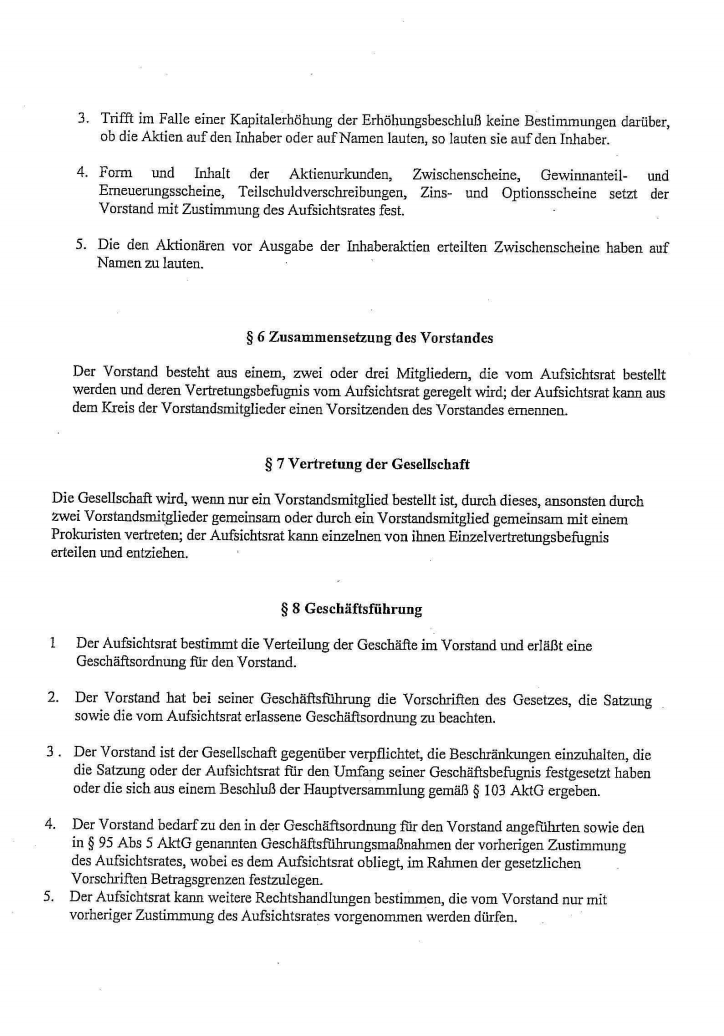

An AG must have at least one managing director. Only natural persons may be appointed as managing directors. The appointed managing director must also be of legal age and possess legal competence. The managing director is likewise not required to have his ordinary residence in Austria. Members of the management board are not required to hold any shares in the AG.

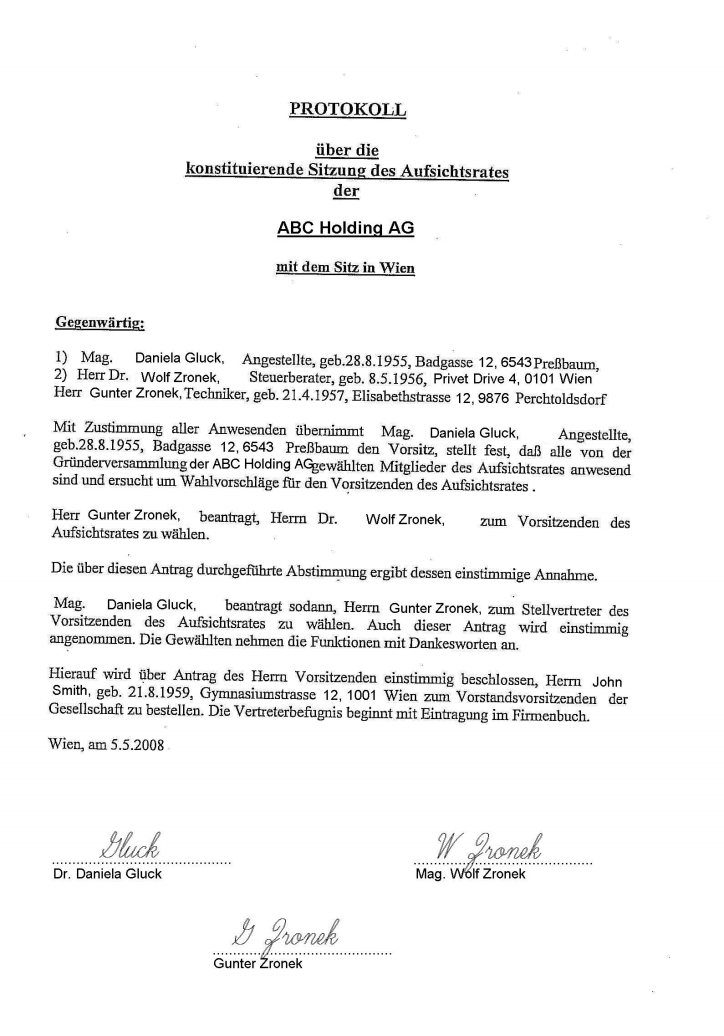

In contrast with a GmbH, a supervisory board is compulsory for every AG. The members of the supervisory board (of whom there must be at least three) are elected by the general meeting of shareholders. Elected members of the supervisory board are appointed for a maximum term of approximately five years. It is permissible to appoint members of the supervisory board for a shorter term, and members may be reappointed.

The supervisory board of the AG must meet at least four times a year.

Corporate Secretary is not required.

Any natural person or legal entity and comparable foreign entities are eligible to become shareholders of an AG. It is not required for a shareholder to be an Austrian citizen or to have his domicile or place of residence in Austria. Where only a single shareholder is present in the AG, that shareholder must be identified by name in the Commercial Register.

The top-level constitutive body of the AG is the general meeting of shareholders. The shareholders adopt resolutions either at the general meeting of shareholders or by written consent. However, it is also permissible for them to adopt resolutions of the shareholders orally, even tacitly.

General meetings of shareholders must be held at least once per fiscal year, in each case during the first eight months of such year.

The general meeting of shareholders must be held at least once per year, within the first eight months of the year, for the purpose of presenting the annual financial statements, granting a discharge to the management board and the supervisory board, adopting resolutions on appropriation of profits and appointing a chartered accountant to audit the financial statements.

The beneficial owner registry was created in Austria in 2018. It contains information on the beneficial owners of legal entities registered in Austria. The registry was created to prevent money laundering and terrorist financing in accordance with the Fifth EU Anti-Money Laundering Directive.

In 2020, part of the information of the Austrian Register of Beneficiaries became publicly available. Information about the company: name, registration number, address. Information about the beneficiaries: name, date of birth, nationality and country of residence, as well as the amount of beneficial ownership. Other information about the beneficiaries is available only in cases provided for by law and in accordance with a certain procedure.

Austrian legal entities have to file information about their beneficiaries once a year. They are also obliged to report any changes. Failure to submit the required information to the register of beneficiaries, or deliberate misrepresentation of data, is subject to a fine (up to EUR 200 000).

The minimum amount of the capital of a GmbH is EUR 10 000. The capital may be paid in cash or in tangible form, but at least 50% of the share capital must be paid in cash.

Where the AG is formed not exclusively based on paid-in cash contributions, but also by contributions in kind, a court-appointed formation auditor must undertake a formation audit. Just as in the case of a GmbH, cash contributions must be paid into a bank account of the “AG in formation” and a confirmation from the bank must be submitted to the Commercial Register court.

How long does it take to set up a company in Austria?

It takes about 1 month to set up a new company in Austria, from applying for registration to receiving a set of documents.

How much does it cost to register a company in Austria?

The cost of opening a company in Austria starts from EUR 13 100 and depends on the set of services you need. The minimum package includes: turnkey company registration, lease of registered office for one year and secretarial services, payment of all necessary fees and charges, as well as apostilled translation of the founding documents.

What taxes are in Austria?

In Austria, businesses are subject to various taxes, including: 1) Corporate income tax: This tax is levied on the profits of a company at a rate of 25%. 2) Value-added tax (VAT): Businesses are required to charge VAT on the goods and services they sell. The standard VAT rate in Austria is 20%. 3) Social security contributions: Employers in Austria are required to pay social security contributions on behalf of their employees. The rate varies depending on the type of contribution, but generally ranges from 20-33%. 4) Property tax: Businesses that own commercial property in Austria may be subject to property tax, which is levied at a rate of 1.1% of the property's value. 5) Other taxes: Depending on the type of business and the nature of its activities, a company may also be subject to other taxes, such as withholding tax on dividends and capital gains tax on the sale of assets.

Is Austria offshore?

Austria is not an offshore jurisdiction. It is a sovereign country located in Central Europe and is a member of the European Union. It has a developed economy and is considered a high-income country. Companies operating in Austria are subject to the same tax laws and regulations as other businesses in the country. They are required to pay corporate income tax, value-added tax (VAT), and may be subject to other taxes and fees depending on the nature of their business and their specific circumstances.

Can a foreigner register a company in Austria?

Yes, a foreigner can register a company in Austria. There are no restrictions on foreign ownership of businesses in Austria, and the process of registering a company is generally the same for both citizens and foreigners. To register a company in Austria, you will need to choose a legal form for your business, select a business name, and register your company with the relevant authorities. You may also need to obtain any necessary licenses and permits, and register for taxes. It is advisable to seek the help of a lawyer or other professional when setting up a business in Austria to ensure that you are following all the necessary steps and complying with local laws and regulations.

How do I start a GmbH in Austria?

To start a GmbH (Gesellschaft mit beschränkter Haftung) in Austria, you will need to follow these steps: 1) Choose a unique company name that is not already in use by another company in Austria. You can check the availability of a company name by searching the online company register at the Federal Economic Chamber (Wirtschaftskammer Österreich). 2) The articles of association is a legal document that outlines the rules and regulations for the operation of your GmbH. It must be signed by all founders and must include the following information: the company name, the purpose of the company, the names and addresses of the founders, the amount of share capital, the distribution of shares, and the duration of the company. 3) To register your GmbH, you will need to submit the articles of association and other required documents to the Commercial Court (Handelsgericht). You will also need to pay a registration fee. 4) Depending on the nature of your business, you may need to obtain various licenses and permits in order to operate legally in Austria. 5) You will need to open a corporate bank account in order to conduct financial transactions on behalf of your GmbH. 6) You will need to register your GmbH for taxes and pay any applicable taxes, such as value-added tax (VAT) and corporate income tax. 7) If you plan to hire employees, you will need to follow Austrian labor laws and regulations, including those related to hiring, wages, and benefits.

What is difference between LLC and GmbH?

LLC, or Limited Liability Company, and GmbH, or Gesellschaft mit beschränkter Haftung, are both types of legal business structures that offer limited liability protection to the owners. One key difference between LLCs and GmbHs is the country in which they are formed. LLCs are a type of business structure commonly used in the United States, while GmbHs are a type of business structure commonly used in Austria and Germany. Another key difference between LLCs and GmbHs is the way in which they are owned and managed. LLCs can be owned by one or more individuals or entities, and the management of an LLC can be structured in a variety of ways, such as through a board of directors or through the owners themselves. GmbHs, on the other hand, must have at least one managing director and can also have one or more authorized representatives. The managing director is responsible for the day-to-day management of the GmbH, while the authorized representatives are responsible for representing the GmbH in legal matters. In terms of taxes, LLCs and GmbHs are treated differently in their respective countries. In the United States, LLCs can be taxed as a sole proprietorship, partnership, or corporation, depending on the number of owners and the specific tax election made by the LLC. In Austria, GmbHs are subject to corporate income tax at a rate of 25%. In summary, LLCs and GmbHs are both types of business structures that offer limited liability protection to the owners, but they differ in the country in which they are formed and the way in which they are owned and managed. They also have different tax implications in their respective countries.