The calculator allows you to calculate the approximate cost of maintenance of accounting services to support and audit the company.

CalculateThe main regulating laws: Companies Act 2014; Companies (Accounts) Act 1999; Companies (Consolidated Accounts) Act 1999.

According to the Companies Act of Gibraltar, companies must file financial statements with the Registrar (Companies House) annually. Financial statements can be prepared in accordance with IFRS or in accordance with the above laws and generally accepted accounting practice (GAAP) of Gibraltar, including the Financial Reporting Standard FRS102 (Financial Reporting Standard applicable in Great Britain and Ireland and adopted in Gibraltar). FRS102 can be called a “copy” of IFRS for small and medium-sized enterprises; it has applied in Gibraltar since 2016.

Requirements regarding the set of financial statements to be filed with the Registrar change depending on the company’s classification. Companies are classified as large, medium-sized, micro and small companies based on revenue, assets (balance sheet) and number of employees.

|

Company

|

Revenue

|

Assets (balance sheet)

|

Average headcount of employees

|

|

Micro

|

< 632 000 GBP

|

< 632 000 GBP

|

< 10

|

|

Small

|

< 10 200 000 GBP

|

< 5 100 000 GBP

|

< 50

|

|

Medium-sized

|

< 36 000 000 GBP

|

< 18 000 000 GBP

|

< 250

|

|

Large

|

> 36 000 000 GBP

|

> 18 000 000 GBP

|

> 250

|

For example, a company will be classified as medium-sized if it exceeds 2 of 3 parameters in the table in line 2 in the current and previous period. Later on the company will cease to be classified as medium-sized only after it does not exceed the said limits in two straight years.

|

Group of companies

|

Revenue

|

Assets (balance sheet)

|

Average headcount of employees

|

|

Small

|

< 10 200 000 GBP net

< 12 200 000 GBP gross |

< 5 100 000 GBP net

< 6 100 000 GBP gross |

< 50

|

|

Medium-sized

|

< 36 000 000 GBP net

< 43 200 000 GBP gross |

< 18 000 000 GBP net

< 21 000 000 GBP gross |

< 250

|

|

Large

|

> 36 000 000 GBP net

> 43 200 000 GBP gross |

> 18 000 000 GBP net

> 21 000 000 GBP gross |

> 250

|

The principle of classification of a group of companies is analogous to that described in the example for a separate company above.

Small and medium-sized groups are exempt from preparation and filing of consolidated accounts with the Registrar, except for when the group contains listed companies, a bank or an insurance company. In the case of a medium-sized group, exemption from consolidation must be confirmed in an auditor’s opinion.

Set of documents to be filed with the Registrar depending on the size of the company:

Large company – full financial statements, including

Medium-sized company – the same set of financial statements as for a large company, but the profit and loss statement can be condensed.

Micro and small companies file only condensed financial statements, i.e. balance sheet.

The deadline for filing accounts with the Registrar is 12 months after the reporting date for all companies and 10 months after the reporting date for public companies. A public company, no matter its size, files the same set of financial statements as a large company.

The currency of accounts to be filed with the Registrar can be: GBP, GIP, USD, EUR, JPY or CHF. If the currency of accounts differs from the currency in which the share capital is issued, the company must disclose in the notes the currency of the share capital and the rate of conversion into the currency of accounts.

According to the Companies Act of Gibraltar, companies that have subsidiaries must make consolidated financial statements, and such financial statements must include a consolidated profit and loss statement, consolidated balance sheet and notes.

Requirements regarding compulsory audit of consolidated financial statements are analogous to audit requirements for a separate company, i.e. small groups are exempt from audit of consolidated financial statements.

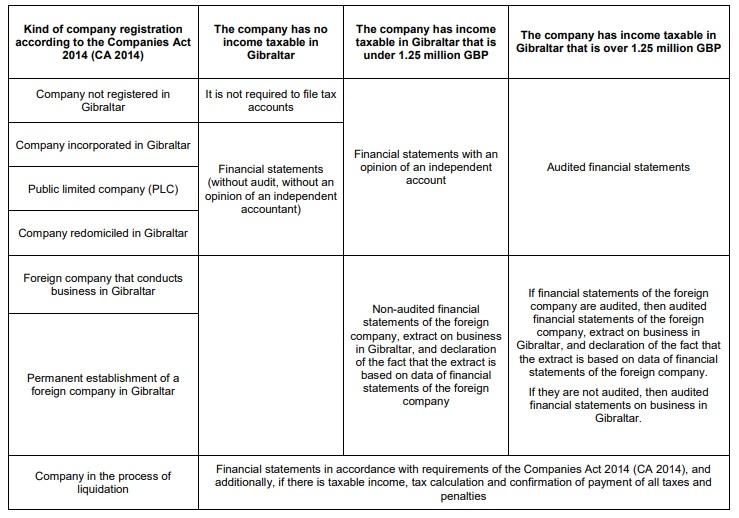

All companies incorporated in Gibraltar or (other) companies that have income taxable in the territory of Gibraltar must prepare and file tax accounts with state authorities (HM Government of Gibraltar). Even if a company has no taxable income, it must file a zero tax return.

Since 1 January 2011, companies shall fill out and file a tax return according to form CT1 along with an additional set of documents, including:

Requirements regarding the set of financial statements accompanying a tax return are described in the tax return, see the table below. The requirements are minimal, i.e. the company, if it wishes, can provide more detailed information.

Tax accounts must be filed and tax must be paid in Gibraltar within 9 months after the end of the financial year.

The following penalties are imposed for late filing of tax accounts:

For example, the company’s financial year ended on 31 December 2021:

The following penalties are imposed for late payment of tax:

For example, the financial year ended on 31 December 2021, and the tax is 1 000 GBP:

Penalties and expenses when filing accounts with the Registrar (Gibraltar Companies House):

It means that in total 175 GBP of penalties and filing fees can be charged.