The legal system of Estonia belongs to civil law family. Today’s legal system of Estonia has been formed for 150 years on the basis of the interaction of various legal cultures, mainly German, pre-revolutionary Russian and Soviet.

The principal forms of business organization in Estonia are:

The most common structure is the private limited company.

There is a range of requirements to the company name in Estonia:

The following steps are required to incorporate a Limited liability company in Estonia:

1. Check online the uniqueness of the proposed company name – less than 1 day: The Commercial Register refuses to register a company if the name resembles an existing company name or registered trade mark. The entrepreneur can check proposed names online at www.rik.ee.

2. Deposit the initial capital in a bank – 1 day: If the share capital is higher than EUR 25,000 the entrepreneur needs to deposit it in a bank. However, if the decided share capital is not over EUR 25,000, it can be established at the memorandum of association that the shareholders are not obliged to make pre-payments for the shares. In that case a shareholder does not make a payment for the share, it will be personally liable to the company in the amount of his/her unpaid share contribution.

3. Submit the registration application to the Commercial Register – 1 day: The costs of registration into the Commercial Register are EUR 140.60 for regular registration or EUR 185.34 for expedited registration. A separate registration with the National Social Insurance Board, which gets its information from the Estonian Tax and Customs Board, is not required. Electronic filing request to the Commercial Register is possible for the holders of Estonian, Portuguese, Finnish and Belgian ID-card. OR verification of foundation documents by the notary who will present those to the Commercial Register. The following documents should be enclosed with the application:

4. Register for VAT at the Estonian National Tax Board – 3 days: The company must register itself as VAT payer if the taxable turnover of the company, excluding imports of goods, exceeds EUR 16,000, as calculated from the beginning of the calendar year. The company’s management board must file an application for company registration, making the company liable for VAT with the Tax and Customs Board, within 3 days as of the date on which the taxable turnover of the company. Registration shall be completed by the Tax and Customs Board within 3 days of filing the application. Registration may be (and in the practice, often is) effected immediately after establishment. Starting January 1, 2009 the application for registration of the company as a taxable person can also be submitted electronically via the electronic system of the Commercial Register.

5. Register with the Central Sick Fund of Estonia – 1 day: In Estonia, health insurance is provided through a compulsory scheme under which employers are obliged by law to pay social tax (the source of revenue for health insurance) for their employees. The employer is obliged to register all new employees, contractual workers and board members with the Health Insurance Fund within 7 days from their recruitment date.

If registered electronically, a company can be established in just a few hours. Registering through a notary will take up to 3 days.

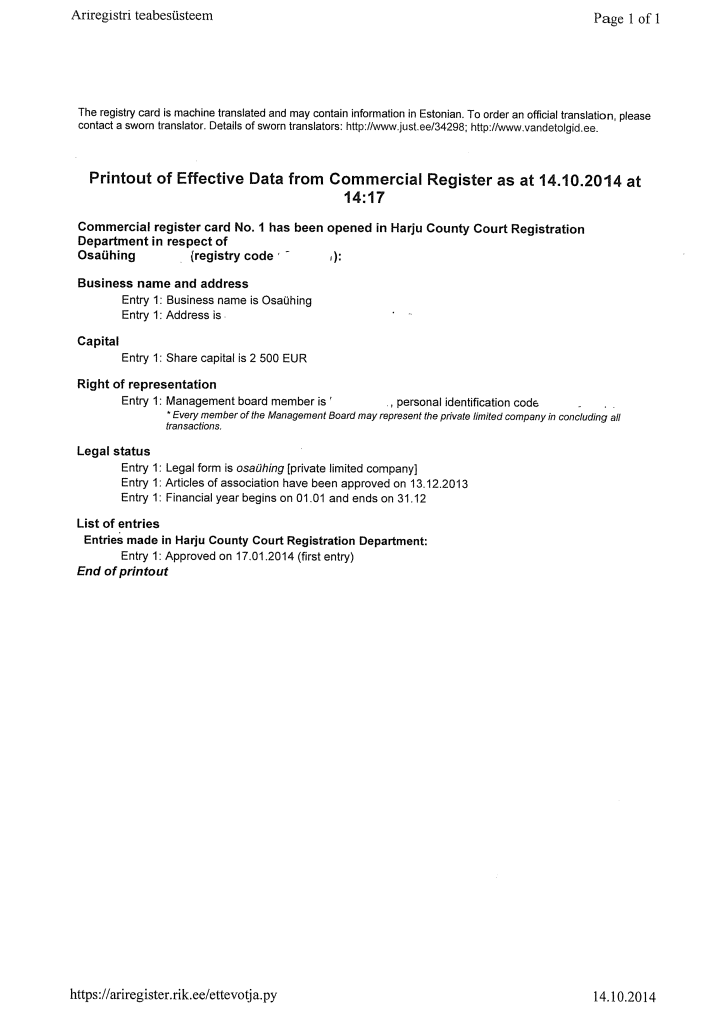

The following information shall be entered in the Commercial Register:

Each company in Estonia must have a registered office.

It is not obligatory to keep any documents at the registered office of the Estonian company.

There are no statutory requirements for a company in Estonia to have a seal.

The redomiciliation of companies to or from Estonia is permitted within the territory of the EU.

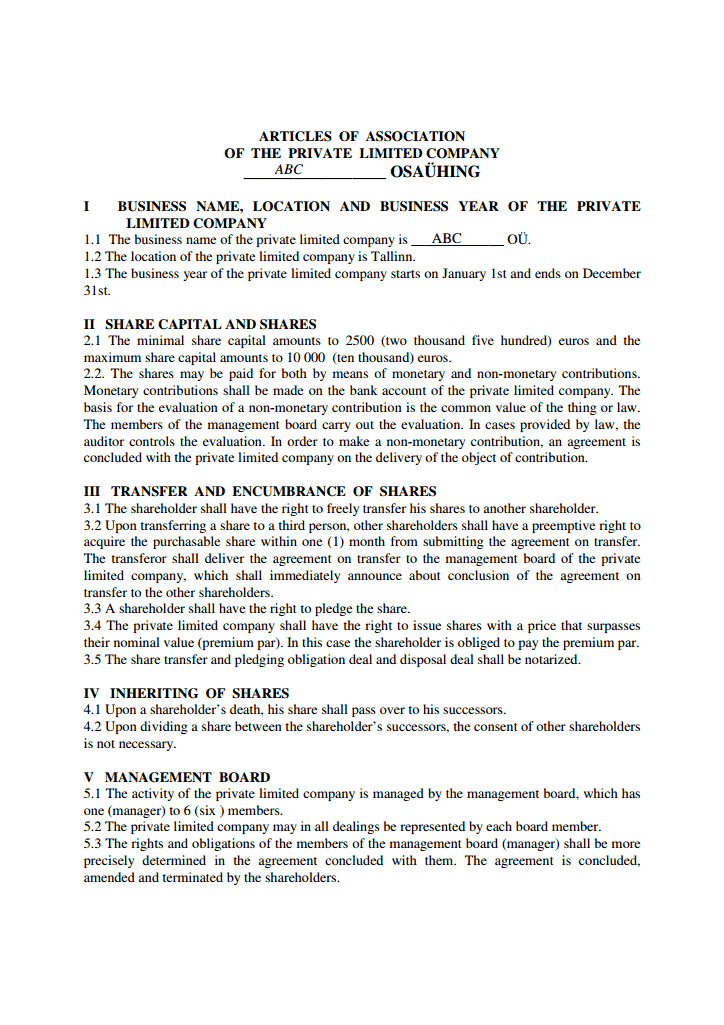

A private limited company must have a management board. The management board is a directing body of the private limited company that represents and directs the private limited company. The management board may have one member (director) or several members. A member of the management board need not be a shareholder. A member of the management board must be a natural person with active legal capacity. If more than half of board members are not residing in Estonia then the company must give the Commercial Register a contact in Estonia where necessary documents can be sent. The foreign owner must give the Commercial Register his/her address and e-mail address.

A private limited company can have a supervisory board if prescribed by the Articles of Association. But it is not mandatory by the law.

A private limited company must have an auditor if prescribed by law or the Articles of Association. An auditor is also mandatory when the company surpasses certain threshold values in terms of turnover, number of employees and asset value.

Estonian companies are not required to appoint a company secretary.

A private limited company may be founded by one or several persons. A founder may be a natural person or a legal person, a resident or non-resident of Estonia.

Shareholders' details appear on public profile.

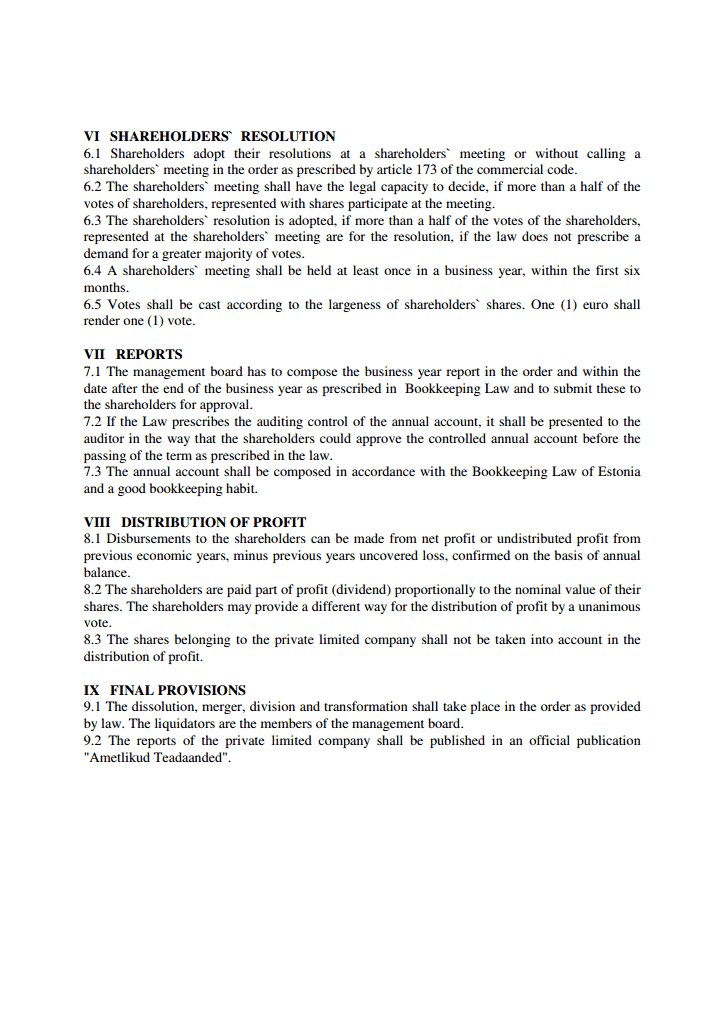

Shareholders should hold general meeting at least once a year.

Since September 2018 all companies registered in Estonia are required to submit information about the ultimate beneficiary to the Registry at the time of registration. There are penalties of up to EUR 400.000 for violation of this rule.

Information provided in the Register of Beneficiaries in Estonia is publicly available on a fee basis (2 EUR). Information kept in the Registry:

The share capital must be a minimum of EUR 2,500. The minimum nominal value of a share is EUR 1. Shares may have the same or different nominal values. The shares of a private limited company may be entered in the Estonian Central Register of Securities.

If the founders are private persons and the share capital is less than EUR 25,000 then the founders can decide that the contribution must not be paid upon the establishing of the company. Until the whole sum has been paid, the founders are personally liable for the obligations of the company within the amount of the missing contribution.

Share capital shall be denominated in euros.

Bases for dissolution of private limited company

A private limited company shall be dissolved:

Adoption of dissolution resolution of private limited company

A dissolution resolution shall be adopted if at least two-thirds of the votes of the shareholders who participate in the meeting, unless the articles of association prescribe a greater majority requirement.

The management board shall present the preceding annual report and an overview of the economic activities of the private limited company for the current year to the shareholders. The overview of economic activities shall indicate the term during which the private limited company is able to satisfy the claims of creditors.

Compulsory dissolution

A private limited company shall be dissolved by a court ruling if:

Petition for dissolution of private limited company

The management board shall submit a petition for entry of the dissolution resolution of the private limited company in the commercial register. The resolution of the shareholders and the minutes of the meeting of shareholders or the record of voting shall be appended to the petition.

If a private limited company is dissolved on the basis of a court decision, the court shall send the decision to the commercial register for entry.

A private limited company is deemed to be dissolved as of the making of the entry on dissolution in the commercial register. Compulsory dissolution enters into force as of the entry into force of the court decision.

A private limited company shall be liquidated (liquidation proceeding) upon dissolution unless otherwise provided by law.

Appointment of liquidators

The liquidators of a private limited company shall be members of the management board unless the articles of association, a resolution of the shareholders or a court ruling prescribes otherwise. A natural person who is prohibited from acting as a member of the management board shall not be a liquidator.

The residence of at least one liquidator must be in Estonia.

A court shall appoint the liquidators in a compulsory dissolution or if this is requested by shareholders whose shares represent at least one-tenth of the share capital. The court shall also specify the procedure for and amount of remuneration for the liquidators.

Removal of liquidators

A liquidator who is a member of the management board, or who has been appointed in accordance with the articles of association or by a resolution of the shareholders can be recalled at any time by a resolution of the shareholders. In order to adopt such resolution, a majority of votes equal to the majority of votes necessary for appointment of a liquidator is needed.

A court may recall a liquidator appointed by the court, and to appoint a new liquidator. At the request of the shareholders whose shares represent at least one tenth of the share capital, a court may also recall, for a good reason, a liquidator who is a member of the management board, or who has been appointed in accordance with the articles of association or by a resolution of the shareholders, and to appoint a new liquidator.

A liquidator may resign for the same reasons and pursuant to the same procedure as a member of the management board.

Entry of liquidator

The management board shall submit a petition for entry of the first liquidators in the commercial register. A petition for entry in the commercial register of a change of liquidator or the right of representation of a liquidator shall be submitted by the liquidators.

If a liquidator is appointed by a court decision, the court shall send the decision to the commercial register for entry.

The names and personal identification codes of the liquidators shall be entered in the commercial register.

Rights and obligations of liquidators

Liquidators have the rights and obligations of the management board which are not contrary to the nature of liquidation. Liquidation does not affect the legal relationships between the shareholders or between the shareholders and the private limited company, or the rights of the supervisory board.

The liquidators shall terminate the activities of the private limited company, collect debts, sell assets and satisfy the claims of creditors.

The liquidators may only conclude transactions which are necessary for liquidation of the private limited company. The right of representation of liquidators is unrestricted with regard to third persons.

The right of representation of liquidators who are members of the management board does not change upon liquidation unless the articles of association, a resolution of the shareholders or a court decision prescribes the changing of the right of representation into joint representation or sole representation. Liquidators appointed by a resolution of the shareholders or a court decision may represent the private limited company only jointly.

During a liquidation proceeding, the notation “likvideerimisel” [in liquidation] shall be appended to the business name of the private limited company.

If dissolution of a private limited company is prescribed by the articles of association or is decided by the shareholders, the shareholders may, until commencement of the distribution of assets among the shareholders, decide on continuation of the activities of the private limited company or on merger, division or transformation of the private limited company. A resolution on continuation of activities shall be adopted if at least two-thirds of the votes of the shareholders who participate in the meeting, unless the articles of association prescribe a greater majority requirement.

If continuation of activities is decided, the same resolution shall designate the new management board and supervisory board, and shall reduce the share capital to the value of the remaining assets.

The liquidators shall submit a petition for entry of the continuation of activities in the commercial register. The resolution on continuation shall enter into force as of its entry in the commercial register.

Liquidators shall submit a petition for deletion of a private limited company from the commercial register after the conclusion of the liquidation, however not earlier than six months after the entry of the liquidation of the private limited company in the commercial register and publication of the liquidation notice and after three months of the date on which the shareholders were informed that the final balance sheet and asset distribution plan are presented to the shareholders for examination, provided that the private limited company is not a party to any court proceedings currently conducted in Estonia. The final balance sheet and asset distribution plan shall be appended to the petition. The petition shall include a confirmation by all the liquidators that the final balance sheet and asset distribution plan have not been contested in court, or the action has been not been heard or has not been satisfied, or that the proceeding in the matter has been terminated and the claims of the creditors of the private limited company have been satisfied or that the assets necessary to satisfy the claims have been deposited and that the private limited company is not a party to any court proceedings currently conducted in Estonia.

If, after the private limited company has been deleted from the register, it becomes evident that the private limited company has assets which were not distributed and that supplementary liquidation measures are necessary, a court may, at the request of an interested person, order a supplementary liquidation and restore the rights of the former liquidators or appoint new liquidators.

Price5 400 EUR

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and Commercial Register incorporation fee

Price1 900 EUR

providing a registered address, from the first year (including the services of a local representative if the director of the company is a non-EU citizen)

Price250 EUR

DHL or TNT, at cost of a Courier Service

Pricefrom 700 EUR

Price3 750 EUR

Paid-up “nominee director” set includes the following documents

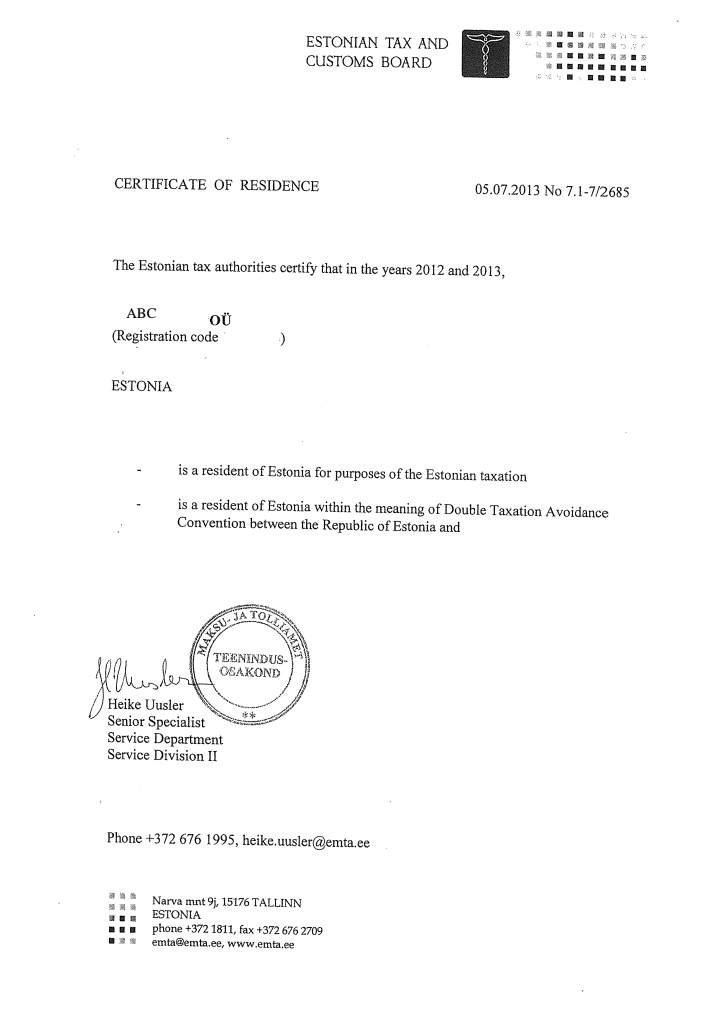

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD