The legal system of Gibraltar is based on English common law.

The English Law (Application) Act of 1962 stipulates that English common law will apply to Gibraltar unless overridden by Gibraltar law. However, as Gibraltar is a self-governing British overseas territory, it maintains its own independent tax status and its parliament can enact laws independently of the United Kingdom.

Due to its specific status with the EU, the agricultural policy, customs union and the value added tax regulations - are not applicable in Gibraltar. Rules of free movement within the territory of the EU apply to capital, people and services, but not to goods. Gibraltar complies with European standards in the sphere of financial leverage and information exchange. Gibraltar issues bank licenses according to the common EU format; banking secrecy is protected by special legislation.

In December 2006, Gibraltar adopted a new constitution for the jurisdiction, which aimed to give it more autonomy from the United Kingdom over its own internal affairs.

The main business entities in Gibraltar are the following:

The most popular form in Gibraltar is a company limited by shares. For offshore solutions the most recommended form is non-resident company. Activity of such a company is regulated by Gibraltar law, but its management is carried out from abroad. A Company incorporated in Gibraltar has the same powers as a natural person.

To be a non-resident company, a Gibraltar-registered company has to satisfy the following criteria:

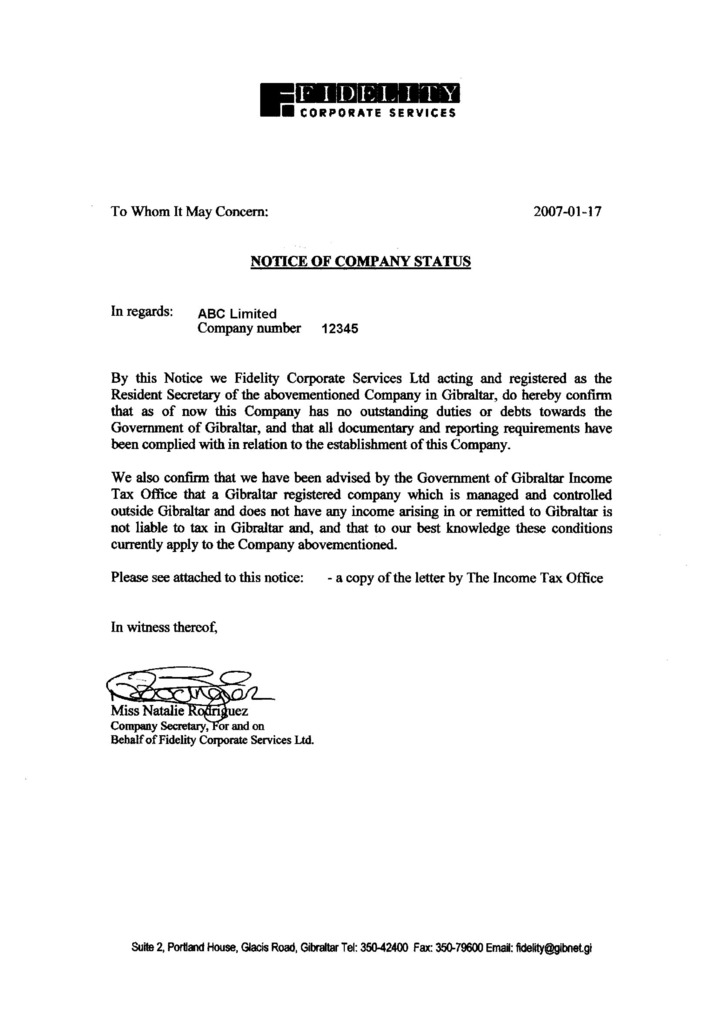

The last requirement effectively means that in order to maintain its no-tax status a Gibraltar non-resident company should not hold any bank accounts in a Gibraltar-situated bank. If the above criteria are satisfied, the company will not fall under the Gibraltar tax system by definition and will not be required to register for Gibraltar taxation purposes. This also means that the non-resident company can in no circumstances be considered as a Gibraltar taxpayer.

A company name must satisfy the requirements of the Gibraltar Business Names Registration Act. The name must be checked and approved at the Company Registry and registered at the Registry of Business Names.

The name may be expressed in English or any language using the Latin alphabet (certified translation required). Names in Cyrillic alphabet are not allowed.

Upon registration and payment of the appropriate fee, the Registrar will issue a Certificate of Registration of a Business Name. Once registered, the Business name is unique to the owner and no one else can use that name. A Business Name, once registered, cannot be changed. However, changes that occur to the company’s details stated in the application (for example, change of address, change in the nature of the business, addition of new partners) must be notified to the Registrar by completing a Form of Change in Particulars and payment of a fee. When the business ceases to exist and the Business Name is no longer required, a Form of Notice of Cessation of Business has to be presented to the Registrar.

A non-resident company cannot use a name without special permission, which is identical or similar to an existing company; any name which is undesirable or offensive in the opinion of the Registrar, any name which suggests royal or government patronage, or which may imply an activity associated with the banking or finance industry e.g. "Association", "Bank", "Imperial", "Assurance", "Group", "International", "Royal" or "Trust".

The following words require special permission from the Gibraltar authorities to appear in a company name and such permission is close to impossible to obtain:

British, National, Gibraltar or Great Britain, Authority, board or council, Association, Federation or Society, Patent or Patentee, Chamber of Commerce, and/or Trade and/or Industry, Co-operative, Group Holding(s), Post office, Giro or Stock Exchange, Register or registered, Friendly Society or Industrial Provident Society, Trade Union, Charter or Chartered, Benevolent, Foundation or Fund, Chemist or Chemistry or Pharmaceutical, Police, Customs, Immigration, Foundation, School or University or College; Club, Authority, Council, Federation, Institute, Trust, and Investment Trust, Unit Trust, Bank, Directors, Financial, Savings, Commodities, Brokers, Credit, Nominee, Dire.

The suffix to denote limited liability in company names is ‘Limited’, or ‘Ltd.’.

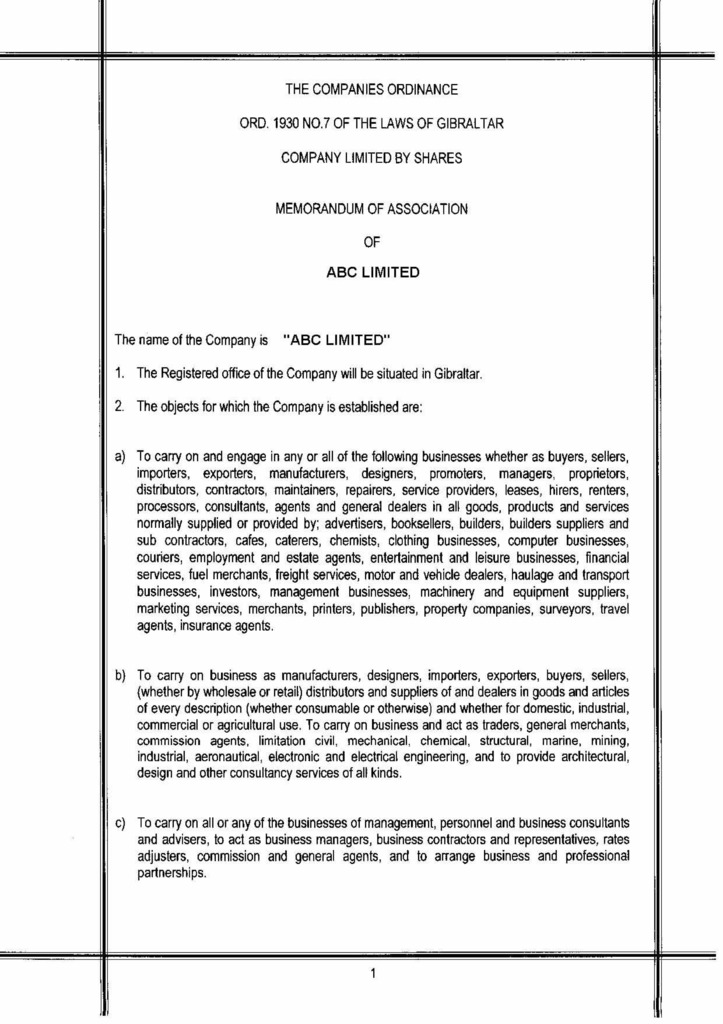

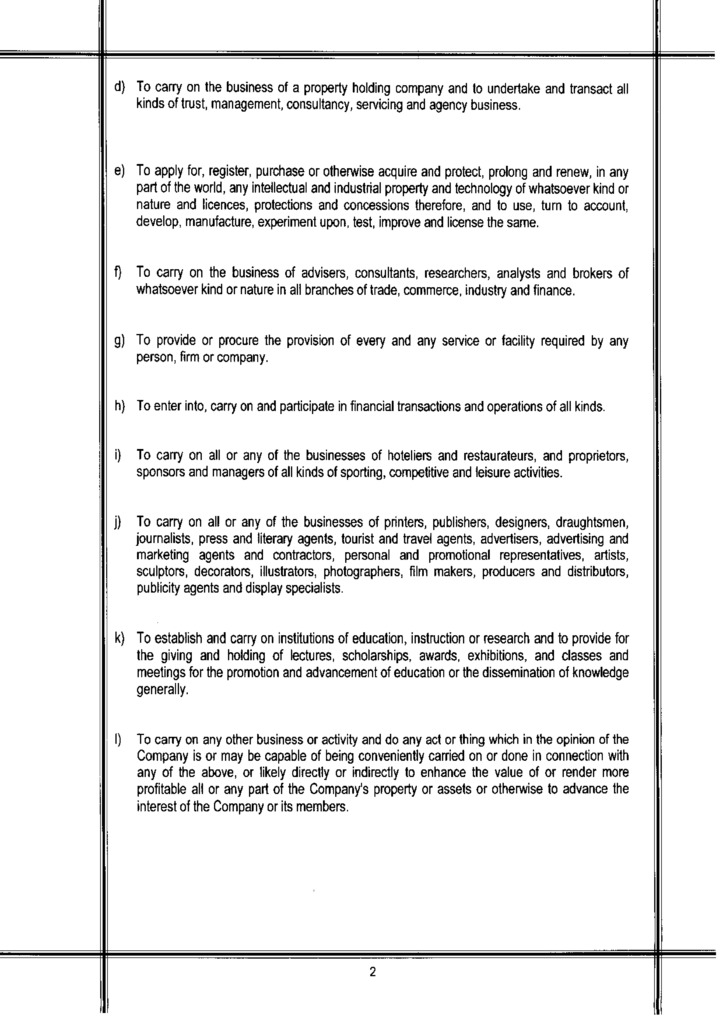

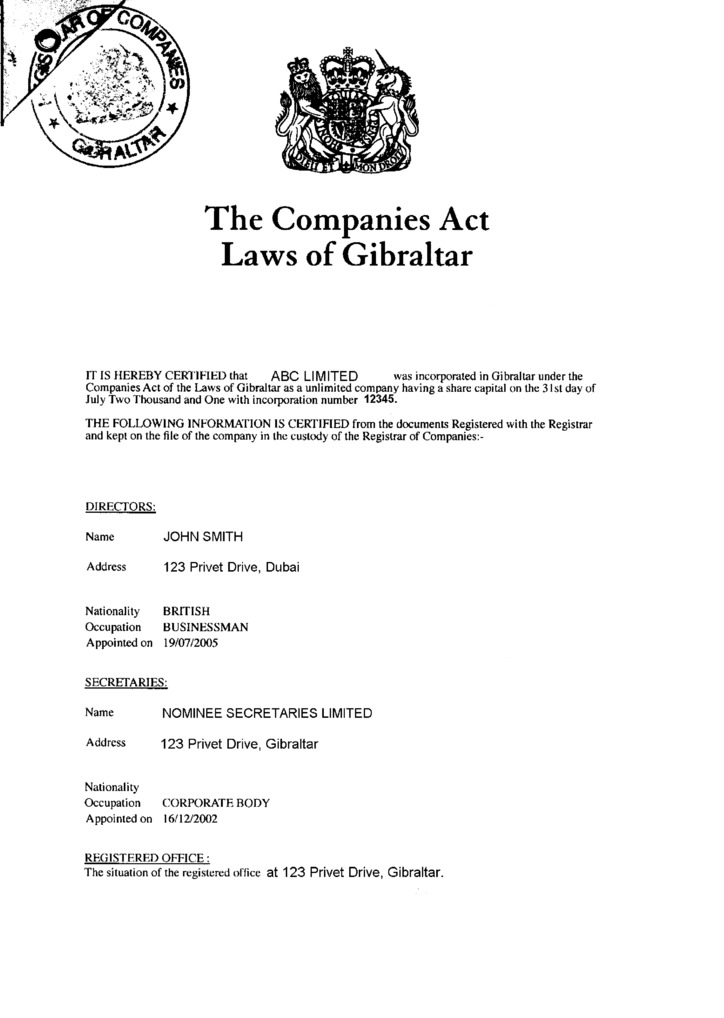

Registration of Gibraltar companies is regulated by The Gibraltar Companies Act (1930).

To incorporate a company in Gibraltar it is required:

Once incorporated, a Certificate of Incorporation is issued.

It is possible to buy a shelf company of this type or to incorporate a new one. The standard incorporation time for Gibraltar companies is 5 days.

A Gibraltar Non-Resident Company is required to have a registered office in Gibraltar. At the registered office address the Company should keep its register of directors and shareholders, minutes and resolutions, share transfer documents, administrative and book-keeping records.

By law every company in Gibraltar must have resident or registered agent.

Under Gibraltar law, a company is not required to have a corporate seal.

It is permitted to redomicile the companies both to and from the Gibraltar, according to the Companies (Redomiciliation) Regulations 1996 ("the Regulations").

Το redomicile into Gibraltar, the company must be domiciled in a country recognized by Gibraltar for this purpose. The Regulations allow for redomiciliation from within the EEA and countries which are members of the British Commonwealth as well as from most other offshore centres.

However, not all of the territories falling into the above categories will accept the redomiciliation of their companies to Gibraltar if there is no a reciprocal measure on the Gibraltar legislation. Therefore, every application for redomiciliation by a company to Gibraltar has to be assessed on a case by case basis. Examples of such territories are:

Requirements to the company under re-domiciliation:

Conditions for the company under re-domiciliation:

The renewal date is 13 months after incorporation and annually henceforward.

There are two types of winding up:

I. Compulsory under an order of the court:

Under Section 220 of the Companies Act the company or any creditor, or any member may petition the court to wind up a company on the grounds specified in Section 220. The two most important grounds are:

The liquidator is appointed by the Court and must act under its supervision and under that of a committee of inspection appointed by the creditors and members.

ΙΙ. Voluntary under a resolution of the company of which there are two types:

(a) Members voluntary winding up.

Basic requirements which allow a company to be placed in Voluntary Liquidation by its Members:

If the company is not in good standing the Registrar will not be able to give effect to the voluntary liquidation as he is not able to ascertain if the appointment of the directors swearing the declaration of solvency is still valid.

(b) Creditors Voluntary Liquidation

If the directors cannot make a declaration of solvency they make a financial report to the creditors and the creditors have the choice of appointing the liquidator. The fact that a voluntary winding up has commenced does not prevent the court from making an order for a compulsory liquidation. Under Section 331 of the Companies Act, the Registrar has a discretionary power to strike off any Company from the Register (no assets or liabilities). The procedure can be instigated by the Registrar or it can be requested by the Secretary or an officer of the company on behalf of the Company.

The new section 267A of the Companies Act allows the Registrar to strike from the register of companies any company, which has not filed annual returns in the previous three calendar years without recourse to the notification procedure of section 331. Since striking off a Company is at the Registrar's discretion, no assurances can be given as to when the procedure of striking a Company off the Register will be completed. In case of striking off, the fact that the Company has been dissolved does not annul the liability of every director, managing officer and member or shareholder; it will continue and may be enforced even after the Company has been struck off.

Pursuant to Sec 332 the Registrar has a discretionary power to restore a company to the Register of Companies within 10 years of the company being struck off.

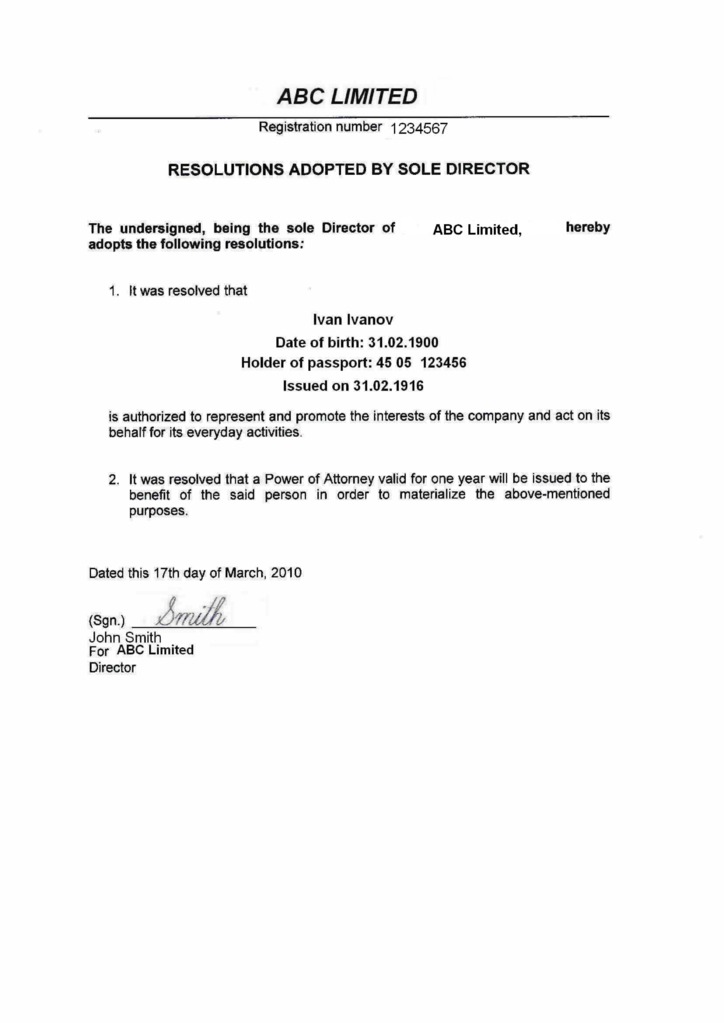

The minimum number of directors is one, who may be natural persons or a body corporate. They may be of any nationality, and need not be resident of Gibraltar. Details of the directors appear on the public file, but confidentiality can be preserved by the use of third party directors.

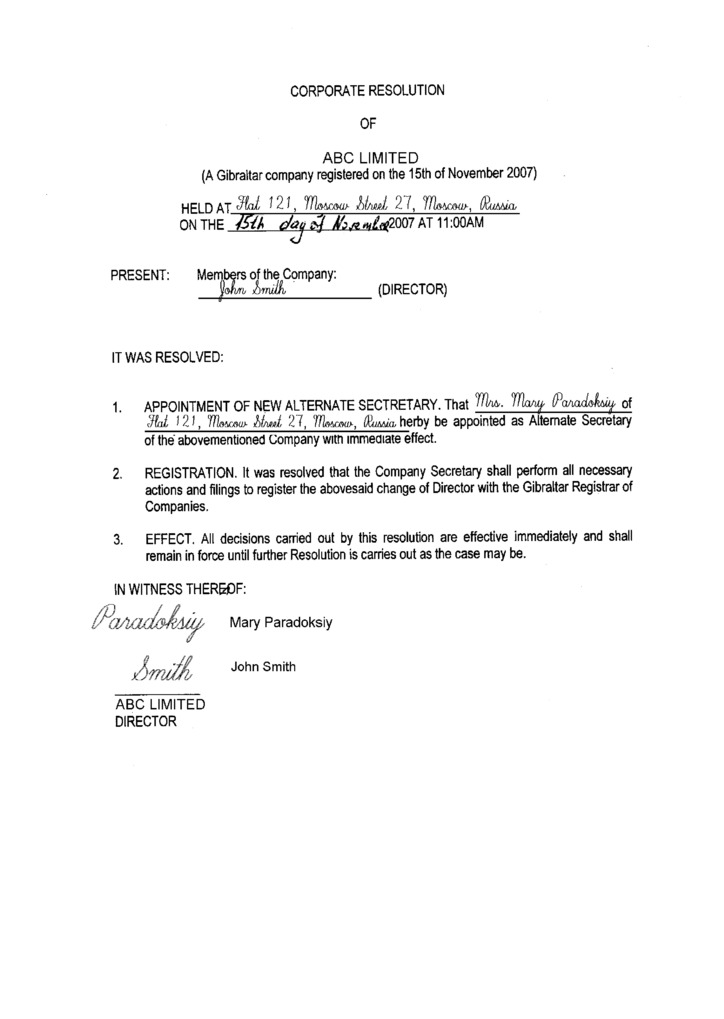

All Gibraltar companies must appoint a resident company secretary to act as registered agent, who may be a natural person or body corporate. A sole director may not be a company’s secretary.

The minimum number of shareholders is one and should be a non resident of Gibraltar. Shareholders can be natural persons or body corporate.

The names of the shareholders are required to be listed on the Annual Return and Incorporation documents.

General meetings are to be held annually, outside Gibraltar.

The details of the beneficial owner are only disclosed to the service provider and are kept in strict confidentiality.

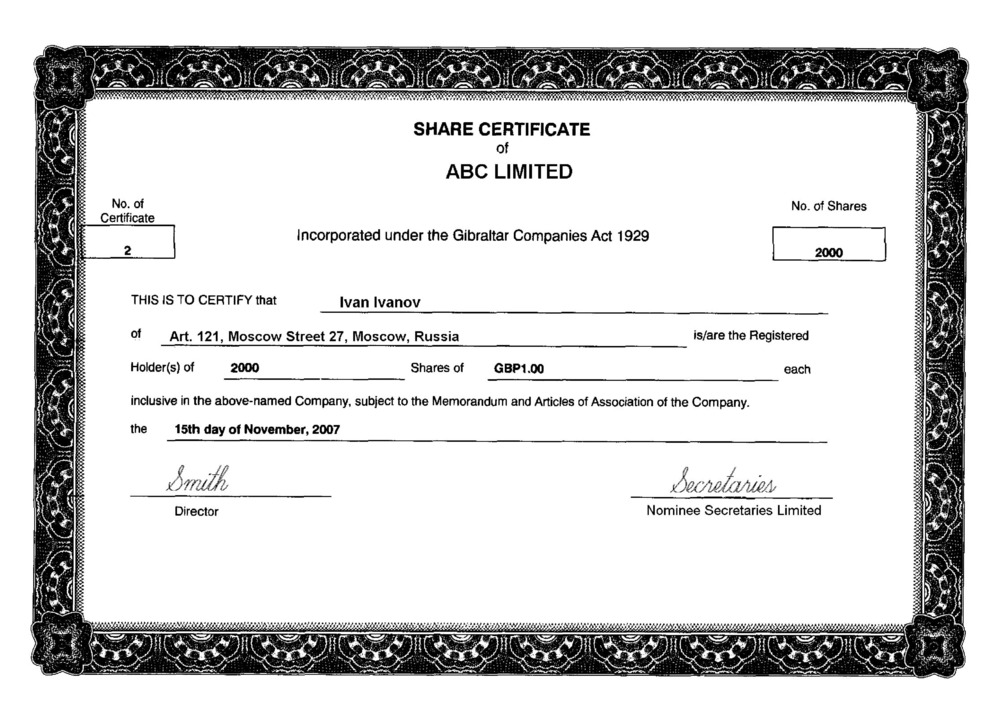

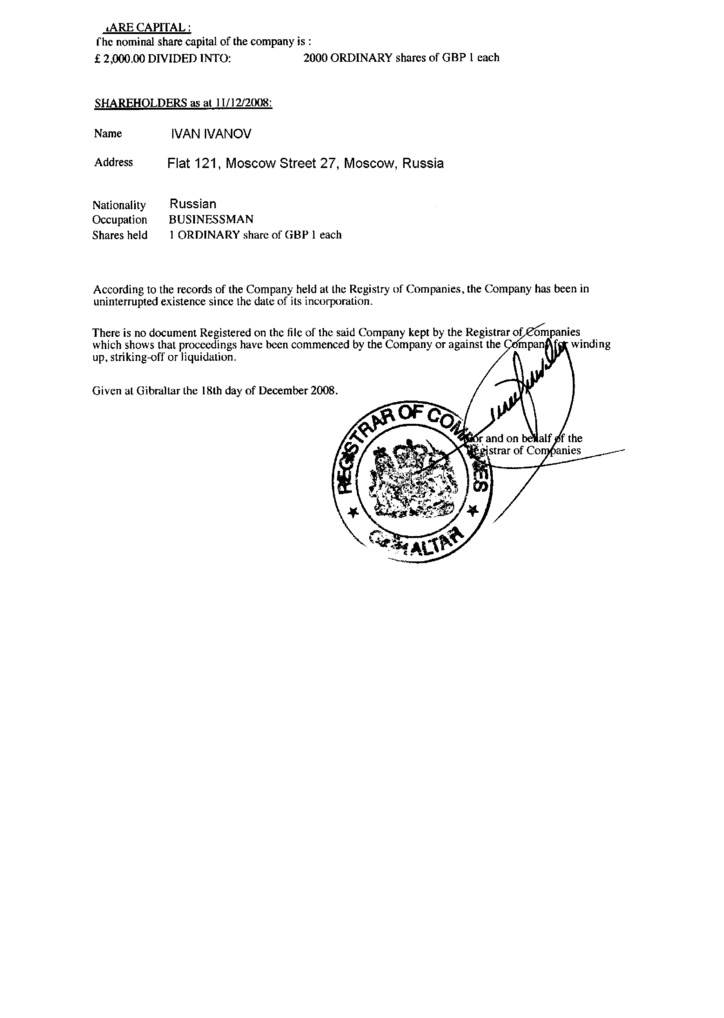

The share capital of a Non-resident company may be denominated in any currency. The minimum authorized share capital is not limited, but normally companies with an authorized capital of G£ 2'000 are incorporated, as the minimum tax on share capital at the incorporation is G£10 (i.e. 0.5 % of GPB 2000), divided into 2000 shares of G£1 each. Minimum paid up capital is G£1. There are no payments deadlines or requirements to pay the authorized capital. Usually it is paid within 1-2 month after registration and once account is opened. As for the issued share capital, it is paid once shares are issued. Shareholders are liable to pay for any unpaid share capital in the event of the company being insolvent. Authorized share capital must be above or equal to the issued share capital. For example, the Gibraltar company can be incorporated with an authorized share capital G£10,000 divided into 10,000 shares of G£1.00 and only 2 shares can be issued and the remaining (without any obligation) can be issued by the Board of Directors of the company at any time if they wish so.

Bearer Shares are not permitted.

Price3 465 USD

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and incorporation fee

Price2 450 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 750 USD

Price705 USD

Paid-up “nominee director” set includes the following documents

Price530 USD

Paid-up “nominee shareholder” set includes the following documents

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

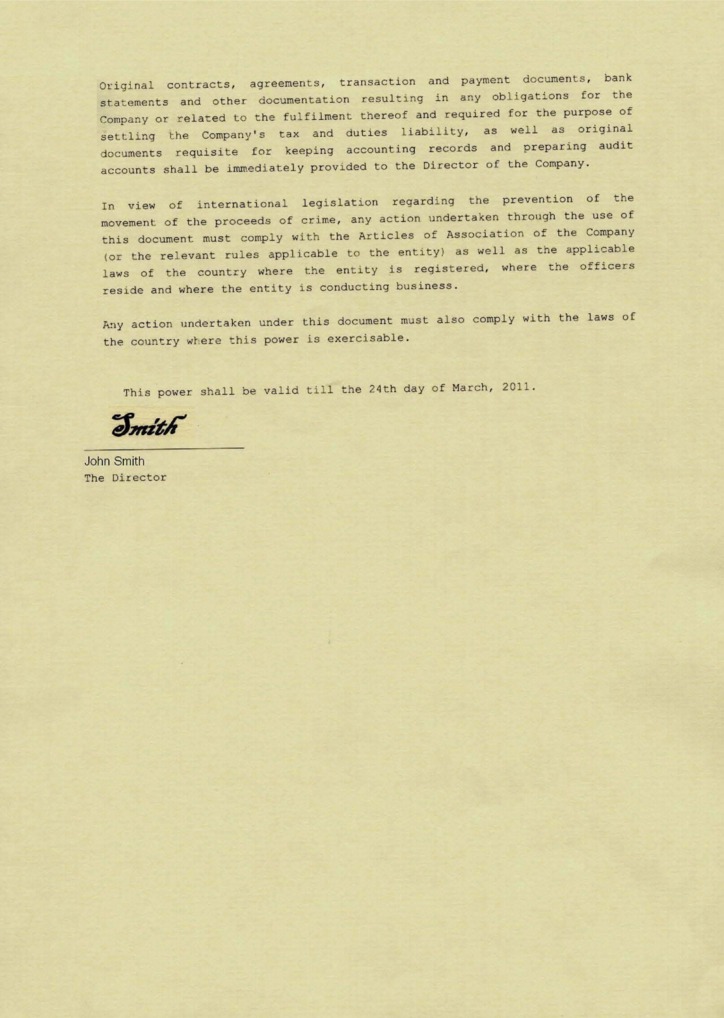

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price250 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price350 USD

Price100 USD