Luxembourg is a civil law jurisdiction. Its legal system is similar to the French Napoleonic Code, except for the commercial and penal divisions, which are similar to their Belgian counterparts. The tax law in principal is based on German tax legislation.

The principal forms of business organization in Luxembourg are:

The most common structures are Private Limited Company (société à responsabilité limitée, Sarl) and Public Company Limited by Shares (société anonyme, SA).

The name of a public company must contain the French words Société Anonyme (or its abbreviation SA) or the German word Aktiengesellschaft (or its abbreviation AG). The name must be different from that of any other company. If it is identical, or if the similarity can lead to error, any interested party may cause it to be changed and may, as the case may be, claim damages. Therefore an enquiry must be made to the Register of Commerce and Companies (Registre du Commerce et des Sociétés) to make sure the proposed name is not used by any other company, and the Register would issue a certificate to confirm the availability of the name. The company name can be in any language using Latin alphabet, but the Register of Commerce and Companies may request a French or German translation if a foreign language is used. Names in Cyrillic alphabet are not allowed. The following elements in the name, their derivatives or foreign language equivalents require consent or a license: Bank, Building Society, Savings, Insurance, Assurance, Reinsurance, Fund Management, Investment Fund, as well as any other names that may suggest association with the banking or insurance business, or government patronage.

To register a company in Luxembourg it is required:

1) to choose a company name and check it for availability with Trade and Companies Register;

2) to get a business permit (this step is required if the company is to do special types of business requiring license) – is granted within a week upon application receipt;

3) to register a company with the Register:

Required documents:

4) to register with the Joint Social Security Administration within 8 days of entry into service of the 1st employee hired;

5) to register with the tax authorities to obtain VAT number.

Besides, it is possible to buy a shelf company of this type or to incorporate a new one, though it should be noted that due to the costs associated with incorporation and the paid up share capital requirements, shelf companies are not widely available.

Luxembourg companies must have a registered office (seat) in Luxembourg. This can be an address provided by a domiciliation agent in Luxembourg. Under the law of 31 May 1999 regulating the domiciliation activity only a member of one of the following regulated professions, established in Luxembourg, may act as a domiciliation agent: credit institution or other professional of the financial sector or insurance sector, lawyer, independent auditor, qualified accountant. The company must keep at the registered office the share register.

There are no statutory requirements for a Luxembourg company to have a seal.

Luxembourg companies may open accounts with banks both within and outside Luxembourg.

There are a number of restrictions on the activities of Luxembourg companies. They cannot undertake any business in financial sector (as banks, investment firms, financial advisors, brokers etc) or carry out insurance or reinsurance business, unless a special license is obtained.

Companies are renewed annually and the renewal normally includes: payment of fees for nominee directors and shareholders (if any), and the registered office.

The redomiciliation of companies is permitted both to and from Luxembourg.

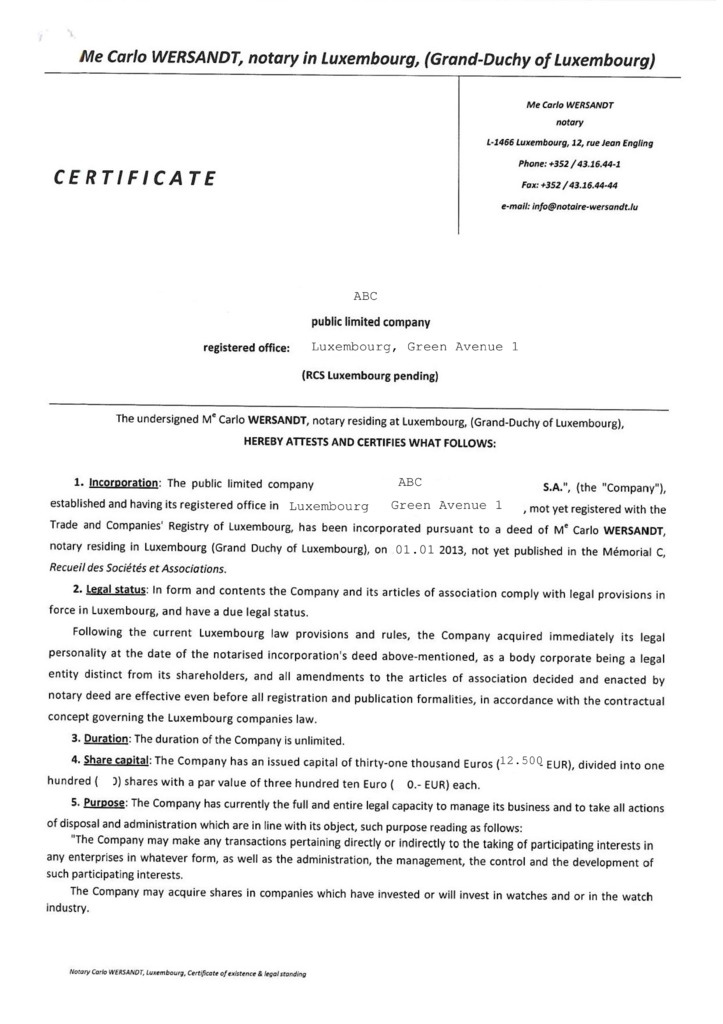

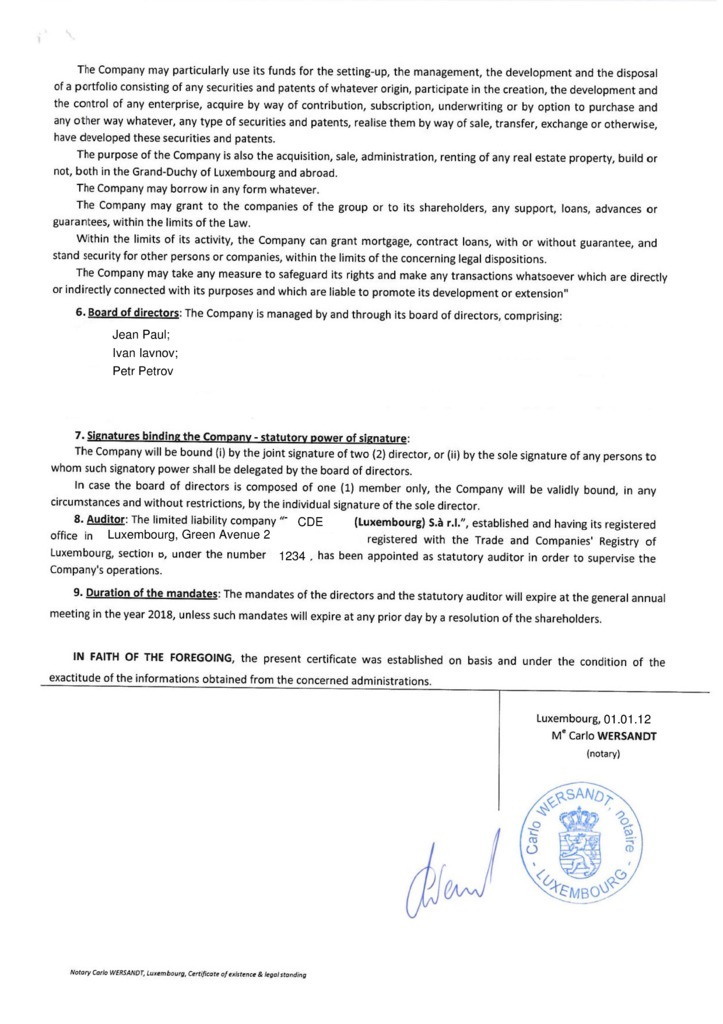

Traditionally, the public company has a one-tier management structure and is governed by the board of directors. The members of the board are appointed by the general meeting of shareholders (however, the first appointment may be made in the articles of incorporation of the company) for a maximum term of six years. The board should consist of at least three members (unless there is only one shareholder, in which case the minimum number of directors is one) who can be natural or legal persons, resident or non-resident. Board meetings of the company may take place both in and outside Luxembourg.

Director’s details are disclosed to the local agent and appear on public file.

However, following the 25 August 2006 amendment to the company law, the public company can now choose between the traditional one-tier structure with a board of directors, or the new two-tier structure with a management board and a supervisory board.

The public company with the new two-tier governance structure is managed by its management board which should consist of at least two members of any nationality or residence. The management board may consist of less than two persons only if the company’s share capital is less than EUR 500,000 or in the case of a single-shareholder company.

The members of the management board are appointed and revoked by the supervisory board or, if the articles of incorporation provide for it, by the general meeting of shareholders. The management board can execute all acts necessary in order to achieve the corporate object of the company, except for the powers explicitly vested in the supervisory board and to the shareholders meeting. At least every three months, the management board has to provide the supervisory board with a written report on the company’s state of affairs.

The supervisory board of the company consists in principle of at least three members who are appointed (and can be revoked) by the general meeting of shareholders for a period of up to six years but may be re-elected. The supervisory board of a single-shareholder company may have a single member. The supervisory board is in charge of the permanent control and supervision of the company and has the right of inspection of any of its corporate documents, but it shall not interfere with the management of the company. The same person cannot be both member of the supervisory board and of the management board.

Instead of the board of directors, SARL has managers who are appointed by the members for an unlimited or limited period of time. SARL requires the minimum of one manager that can be a natural or legal person and need not be a Luxembourg national or resident. Board meetings of the company may take place both in and outside Luxembourg.

Manager’s details are disclosed to the local agent and appear on public file.

Luxembourg companies are not required to appoint a company secretary.

No statutory auditors are required unless the SARL has more than 25 members.

SARL can be formed by one single shareholder that can be an individual or a company of any nationality or residence. The maximum number of shareholders is 40.

General meetings are to be held annually at the time determined in the articles, if the company has more than 25 shareholders.

Shareholders’ details are disclosed to the local agent and appear on the public file.

In November 2022, Luxembourg decided to temporarily suspend public access to the register of beneficiaries pursuant to the Court of Justice of the EU (CJEE) decision in consolidated cases C-37/20 and C-601/20 of November 22. The Court ruled that Article 1, paragraph 15(c) of Directive (EU) 2018/843 of the European Parliament and of the Council of 30 May 2018, which provides for access to information on the beneficiaries of legal persons to any member of the public, was invalid as it constituted a serious interference with the fundamental rights to respect for privacy and to the protection of personal data enshrined in Articles 7 and 8 of the EU Charter of Fundamental Rights.

Luxembourg passed the Law on the Creation of the Register of Beneficiaries (Registre des Bénéficiaires Effectifs, RBE) in 2019, according to which all legal entities registered in the Luxembourg registry of companies (Registre de Commerce et des Sociétés, or RCS), including investment funds, must contribute to this Register and regularly update information about their beneficial owners.

All forms and types of entities are covered, including companies and partnerships, whether or not they are subject to special regulation, as well as Luxembourg investment funds.

Obligations to provide information to the register of beneficiaries are imposed on companies and their management bodies (directors or managing partners) and the beneficiaries themselves. The law also requires all Luxembourg organizations and individuals subject to the Anti-Money Laundering Act (banks, financial sector professionals, notaries, lawyers, etc.) to notify the RBE within 30 days if they decide that the information provided is incomplete or erroneous.

The following information is submitted to the RBE: full name; nationality; Date and place of birth; place of residence or office address; national identification number; nature and degree of participation. Data is entered into the Register within a month from their update in company files.

Access to the register of beneficiaries is public: not only law enforcement agencies (including the prosecutor's office, financial intelligence units, tax authorities, etc.), but also private individuals can obtain information from it. The authorized bodies have full access to the information in the Register, and the address and TIN of the beneficiaries are not available to individuals.

The share capital of the private company is normally expressed in EUR, but can also be denominated in any other hard currency. The minimum capital is EUR 12 394,68 which must be fully paid up and subscribed. Usually the authorized share capital is EUR 12 500 divided into shares of CHF 100 each. Bearer shares and shares with no par value are not permitted.

A Société de Participations Financières (SOPARFI) is a holding financial company and is rather a status than a corporate form. In fact, SOPARFI can adopt various corporate forms: public company limited by shares (Société Anonyme, “SA”), private limited company (Société à Responsabilité Limitée, “SARL”), partnership limited by shares (Société en Commandite par Actions, “SCA”) and European company (Société Européenne, “SE”), but, in practice, it is generally incorporated in the form of a SA due to its operating flexibility.

The activities of SOPARFI are not limited to holding and management of shares only. Upon authorisation from the Ministry of Middle Classes it can also carry out any commercial activity that is directly or indirectly connected with the management of its holdings. If the SOPARFI undertakes a commercial activity it is subject to the normal rate of corporate income tax and municipal business tax. Corporate income tax rate is 20% for income below EUR 15 000, and 21% for income above EUR 15 000. Municipal business tax depends on the municipality where SOPARFI is located. For example, in the city of Luxembourg it is 6.75%. However, if SOPARFI carries on holding activity only, it can take advantage of Luxembourg double tax treaties network and EU directives.

SOPARFI enjoys the following tax benefits:

1. Exemption from corporate tax and municipal business tax of dividends paid by subsidiaries, if the following conditions are met:

2. Exemption from or reduced rate of withholding tax on dividends.

Dividends distributed by SOPARFI to its shareholders are in principle subject to a withholding tax of 15%. This rate can be reduced under the double tax treaties signed with the respective countries of residence of the shareholders. However, dividends may benefit from a full exemption if the following conditions are met:

Besides, there is no withholding tax on interest paid by the SOPARFI to its shareholders (except in case the SOPARFI offers its securities to the public), nor on liquidation proceeds distributed to the shareholders further to the liquidation of the SOPARFI.

3. Exemption of transfer capital gains, if the following conditions are met:

On 13 February 2007, the Luxembourg Parliament adopted a law on Specialized Investment Funds (SIF). The new law replaces the law of 19 July 1991 on Undertakings for Collective Investments dedicated to institutional investors. The innovations of the law include: extended definition of eligible investors, flexible valuation rules, unlimited range of eligible assets, simplified approval process, no limitations on promoter or manager, light reporting requirements and attractive tax regime.

There are three categories of eligible investors (i.e. investors authorised to invest in the SIF): institutional investors; professional investors; and well-informed investors who have adhered in writing to the status of well-informed investors and who have either a minimum investment of EUR 125,000 in the SIF or a positive assessment from a credit institution or another financial sector professional certifying their aptitude to appraise the contemplated investment and the risks attaching thereto. This last category gives sophisticated individual investors (including high net worth individuals) access to the SIF.

The submission to the SIF regime must be opted for by inserting a mention to that effect in the constitutive documents or offering documents. However, existing 1991 UCIs are automatically governed by the SIF Law without any formalities.

The SIF can be incorporated in a contractual form (as a Fonds Commun de Placement, or FCP) or a corporate form: as a Variable Capital Investment Company (Société d’Investissement à Capital Variable (SICAV)) or as a Fixed Capital Investment Company (Société d’Investissement à Capital Fixe (SICAF)). Should the SIF be incorporated as a SICAV/SICAF, it could be incorporated as a Public Limited Company (société anonyme), a Limited Liability Company (société à responsabilité limitée), a partnership limited by shares (société en commandite par actions) or a cooperative organized under the form of a Public Limited Company (société coopérative organisée sous la forme d’une société anonyme). The SIF must be capitalized with at least EUR 1 250 000. This minimum capital must be reached within 12 months from the date of the authorization from the Luxembourg supervisory authorities of the financial sector (so-called CSSF). Although the SIF has to value its assets at fair value, the bylaws or management regulations can determine how this value will be computed. Therefore, other valuation criteria like those set by professional associations (EVCA, RICS etc.) may be used.

The SIF may invest in all types of assets including equity, debt, real estate, financial derivatives, hedge and private equity investments. The SIF is required by the law to comply with the principle of risk diversification. However, the concept of risk diversification being not detailed in the law, the CSSF issued a circular providing guideline as to the minimum level of risk diversification that must be ensured by the SIF. Under the circular, the SIF cannot invest more than 30% of its assets in a same investment line. This restriction is however waived for investments in collective investment schemes that are subject to risk diversification requirements that are equivalent to those applicable to the SIF.

The SIF is a regulated vehicle subject to the permanent supervision of the CSSF. However, the activities of the SIF can start without a prior approval from the CSSF provided the request for the authorization is filed within the month following the set up of the SIF. It must be noted that although the CSSF does not carry out an in-depth review of all materials, the CSSF has to approve the bylaws/management rules, the directors/managers (must be experienced and reputable) and the choice of the depositary bank of the SIF. The SIF must entrust the custody of the assets to a depositary bank resident in Luxembourg. The annual accounts of the SIF must be audited by a Luxembourg independent auditor. No promoter is required for the set up of the SIF. The SIF must establish an offering document (sales prospectus) and an annual report. The annual report must be presented to the investors at the latest 6 months following the end of the financial year and must include a balance sheet or a statement of assets and liabilities, a profit and loss account, significant information on the financial year as well as additional information for the assessment. Under a CSSF circular, the SIF must also publish a monthly report. In practice, however, if the SIF does not calculate a Net Asset Value each month, the report can be based on the previous available report. The SIF is free form the obligation to consolidate the companies that are held in the portfolio for investment purposes. Besides, there is no requirement to publish the Net Asset Value.

The SIF is exempt from taxes on incomes and gains and from withholding taxes on distributions. The only taxes for which the SIF will be liable are: annual subscription tax of 0.01% on its Net Asset Value (however exemptions from the subscription tax may apply depending on the underlying investments) and fixed capital duty of EUR 75 levied upon incorporation.

Société d’Investissement en Capital à Risque (SICAR), which means ‘an Investment Company in Risk Capital’, was introduced by the law 15 June 2004 and is a regulated vehicle mainly intended for investments in venture capital and private equity in general.

There are three categories of eligible investors (i.e. investors authorized to invest in the SICAR): institutional investors; professional investors; and well-informed investors who have adhered in writing to the status of well-informed investors and who

The submission to the SICAR regime must be opted for by inserting a mention to that effect in the constitutive documents.

The SICAR must be incorporated in one of the following legal forms: public limited liability company (société anonyme), private limited liability company (société à responsabilité limitée), partnership limited by shares (société en commandite par actions), co-operative company in the form of an public limited liability company (société coopérative organisée sous la forme d’une société anonyme) or limited partnership (société en commandite simple). Besides, it must be noted that the SICAR may be set up as an umbrella vehicle with multiple compartments with strict segregation of assets and liabilities between compartments. The SICAR must be capitalized with at least EUR 1 000 000 which can be the subscribed capital increased by the share premiums. Subscription must be made 12 months following the authorisation of the SICAR by the Luxembourg supervisory authorities of the financial sector (so-called CSSF). Unlike regular companies, the SICAR may opt for variable share capital allowing variation in share capital without need to respect any formalities. The SICAR has to value its assets at fair value in accordance with the methodologies set out in its articles of incorporation. Generally, valuation principles established by specialized professional bodies are used. Computation of a periodic NAV may be required by investors if necessary.

The SICAR must invest in assets representing “risk capital” with the aim of rewarding investors in proportion for the risk they bear. The concept of “risk capital” being defined in a broad manner by the Law as the direct or indirect contribution of assets to entities in view of their launch, their development or their listing on a stock exchange, the CSSF issued a circular in order to provide with guidelines as to the eligible assets. In principle, all types of assets (e.g. securities, debt instruments, hybrid instruments, real estate…) should be eligible provided the investment is risky and made with intent to develop or create value. It must be noted that unlike investment funds, the SICAR is not required to diversify its risks. It can invest in only one target.

The SICAR must be authorized by the CSSF prior to starting its operations. Once authorized, the SICAR is subject to the permanent supervision of the CSSF. However, it has to be mentioned that the SICAR benefits from a “light” regulatory regime, resulting from the fact that the SICAR is dedicated to well-informed investors who are deemed to be able to value the risks involved in their investments. Besides, it must be noted that although the CSSF does not carry out an in-depth review of all materials, the CSSF has to approve the offering document, bylaws/management rules, the directors/managers (must be experienced and reputable) and the choice of the depositary bank of the SICAR. The SICAR must entrust the custody of the assets to a depositary bank resident in Luxembourg. The annual accounts of the SICAR must be audited by a Luxembourg independent auditor. The SICAR must establish an offering document (sales prospectus) and an annual report. The annual report must be presented to the investors at the latest 6 months following the end of the financial year. The annual report must include a balance sheet or a statement of assets and liabilities, a profit and loss account, significant information on the financial year as well as additional information for the assessment.

The taxation of the SICAR depends on the legal form. From the five corporate forms available, four are taxable entities (SA, SARL, SCA and SCoSA) and one is tax transparent (SCS).

The SICAR that takes the form of an SA, SARL, SCA or SCoSA is, as a general rule, fully subject to corporate income and municipal business tax at the aggregate rate of 28.59%. However, in practice the SICAR avoids substantial taxation in Luxembourg as it is allowed to exempt from its taxable base all income and gains deriving from:

As a result, the SICAR is only taxable on ancillary income. Besides, it must be noted that the SICAR is exempt from net wealth tax and withholding taxes on dividends, interest and liquidation proceeds. The Luxembourg tax authorities do not require from the SICAR to respect a debt-to-equity ratio (no thin capitalisation rules).

The SICAR that takes the form of the SCS is deemed transparent (i.e. look-through) for Luxembourg tax purposes. Income generated by the SICAR is therefore deemed having been directly earned by the partners in proportion to their respective participation in the limited partnership. Consequently, they will be taxed according to the rules applicable in their country of residence.

Price13 750 EUR

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and Commercial Registry incorporation fee

Price11 090 EUR

including registered address and registered agent, NOT including Compliance fee

Price250 EUR

DHL or TNT, at cost of a Courier Service

Pricefrom 700 EUR

Price3 960 EUR

Paid-up “nominee director” set includes the following documents

Paid-up “nominee shareholder” set includes the following documents

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR