Under the Commercial Code, the following types of commercial entities may be established in Macau to carry on business:

The most common form of business vehicles for foreign companies wishing to carry on business is Limited Liability Company by Quotas.

There are the following requirements for the company name:

To register a company in Macau, you need to go through the following procedure:

1. Apply for a company name and scope of business at the Commercial Registry Office and get Certificate of Admissibility of Trade Name.

2. Prepare Articles of Association with local lawyer and notarize it with registered notary (Chinese version is required) within 60 days after receipt of Certificate of Admissibility of Trade Name;

3. Company registration at the Commercial Registry Office within 15 days after getting notarized Articles of Association:

Required documents:

4. Apply for Declaration of Initiation of Activity at the Financial Service office:

Required documents:

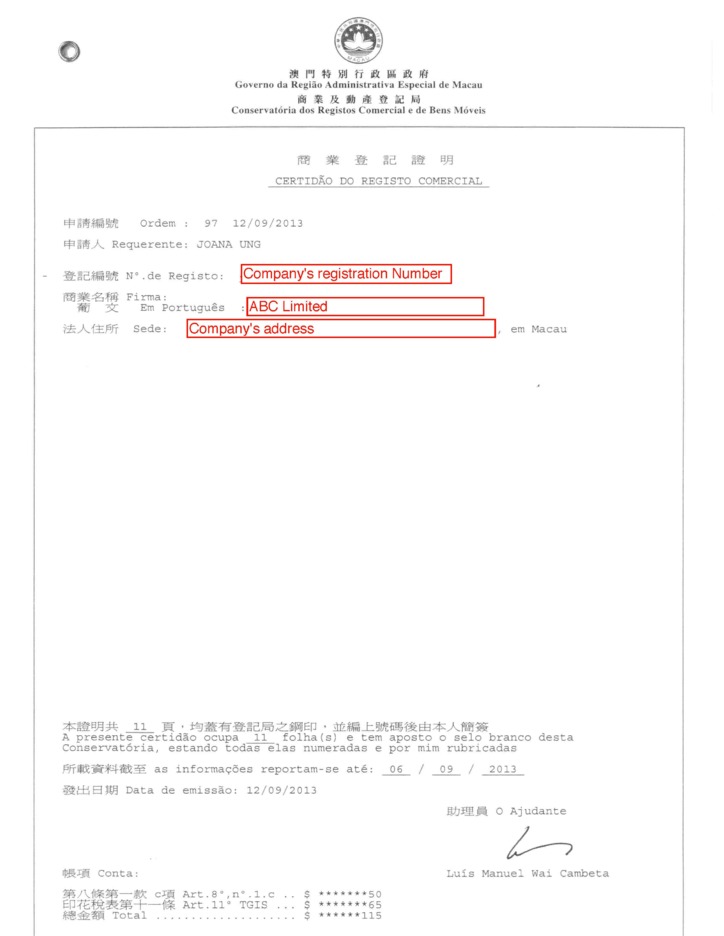

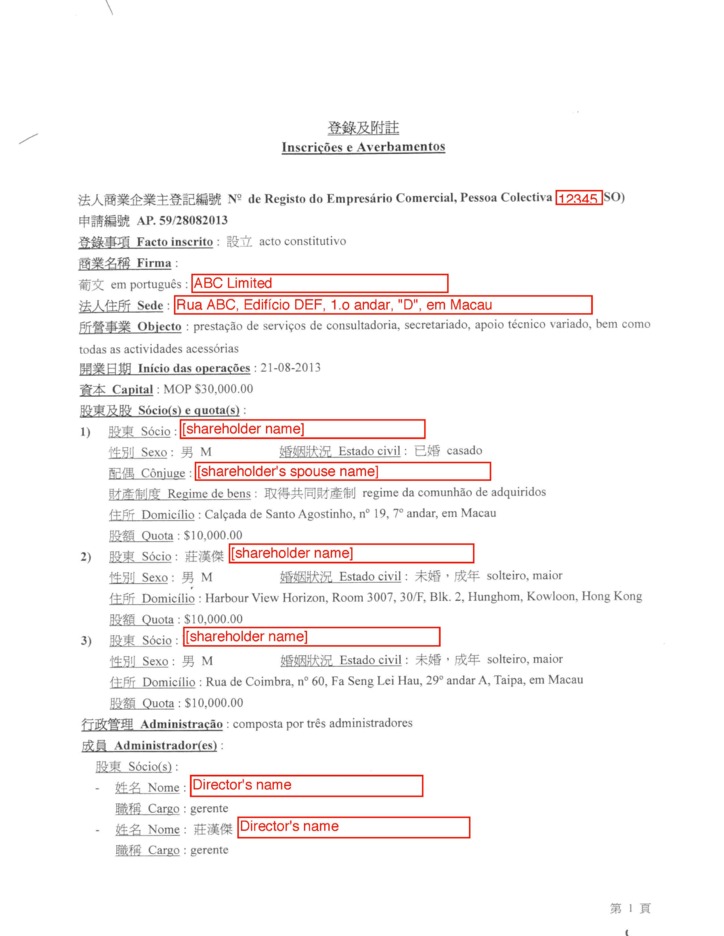

After completion of company registry, employers should fill in the M/2 form and submit it to the “Finance Services Bureau - Professional Tax Division” within 15 days of any employment. The Employer is also responsible for the enrolment of himself and for his employees to the "Social Security Fund". Besides, the company should file Fixed Asset Listing, Balance Sheet and Meeting Minutes Book after commencing operation. The Business Registry will then issue a certificate of incorporation, certifying the name, date of incorporation of the company, object of activity, shareholders, company capital, division of company capital, and representation of the company.

Macau companies must maintain a registered office in Macau. It should be a real address, not a PO Box. The administration of the company can freely move the registered office within the Territory.

Although the commercial code does not require a company seal, mandatory forms for social security, finance services and other public departments require that a company chop is placed next to the legal representative’s signature making it mandatory. The seal should have a company name engraved on it.

The redomiciliation of companies either to or from Macau is not permitted.

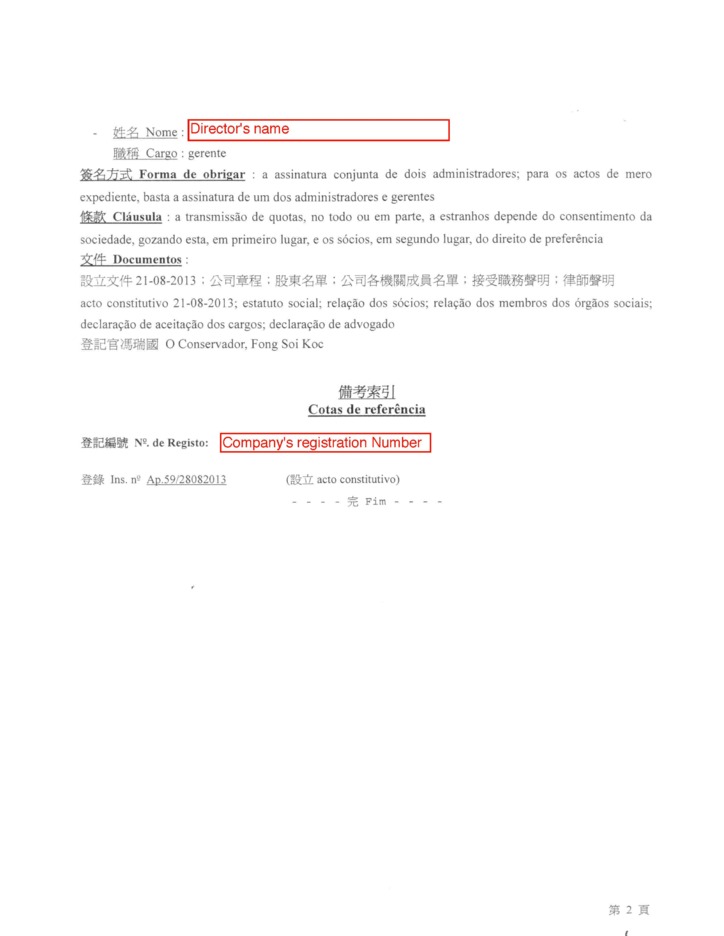

A Macau company is required to have a minimum of one director. Directors are elected by shareholders for an undetermined term if otherwise is required by the Articles of Association. Directors can be non-residents and non-shareholders. Director can be a corporate, but in this case he should appoint an individual as his representative. However, in practice it is not recommended to appoint a corporate as a director, as it requires to do a lot of documents in case of any stuff change in the structure of a company. Directors can be removed by shareholders’ decision.

Information on directors is disclosed to a local agent, and the Business Registry keeps a public record of their names, addresses and business titles. The articles of association can create a board of administration made of at least three members; except if there is a provision of the articles of association to the contrary. Board meeting can be held anywhere in Macau, as long as the place of meeting is specified in the meeting notice.

In Macau a company secretary must be nominated for limited liability company by shares, companies with more than 10 shareholders or quota holders, if they issue bonds or if their capital is above the limit defined by Executive Order of the Chief Executive. All other companies can also nominate a company secretary if desired.

A director or an employee of the company can be nominated as a company secretary. The Business Registry will keep a public record of the name and address of the company secretary.

Macanese companies may have at least two or maximum 30 shareholders. Shareholders can be individuals and corporates, residents and non-residents. The name, address and shareholding of the company shareholders are disclosed to the local agent and filed on public record at the Business Registry.

General Meetings are to be held annually within three months immediately following the end of each accounting period anywhere within Macau SAR as long as place of meeting is specified in the meeting notice.

Information on beneficiary is not disclosed.

Capital in Macau limited company is represented by quotas which are not evidenced by share certificates, but represent a percentage or fixed amount. Minimum paid-up share capital to incorporate a company is MOP 25 000. It should be paid fully upon registration. The amount exceeding minimum can be paid within 3 years, but this amount should not exceed 50% of company capital. If one of the shareholders does not fulfil obligations on capital payment, the rest shareholders are obliged to pay the rest part in proportion to their quotas in the company.

Shares with no par value and bearer shares are not permitted.

Until 2021, Macau had an offshore regime that provided certain benefits to companies. As of today, this regime has been abolished.

Macau is the only place in the People’s Republic of China, where Chinese can gamble legally. There are 33 casinos in Macau, and the income from the business amounted USD 23,5 milliards in 2010, what is 4 times higher than in Las Vegas. It is Macau’s biggest source of revenue, making up 70% of government income.

Gambling in Macau is regulated by Law 16/2001 (regime jurídico da exploração de jogos de fortuna ou azar em casino), adopted in August 2001. It replaced the monopoly system to generate competition, and casino operating concessions were granted through bid. Today there are 6 operating concessions (and subconcessions) which belong to:

It means that chances to enter the gambling market are very slim. Maybe the only opportunity is to buy a stock of shares from one of the operators. However, there are no such offers, so in fact the mark here is almost closed for the newcomers. There are also monopoly concessions for pari-mutuels (horse and dog racing).

Licensing procedure and all the following activity are strictly regulated including taxation and financial statements. Besides, a detailed agreement is to be signed with each operator. The Gaming Inspection and Coordination Bureau (known as DICJ) is the main government unit that oversees the operation of different gaming activities.

From the perspective of company law, gaming concessionaires must be public companies, to which special rules apply, in addition to the general rules stated in the Macau Commercial Code. Except from other numerous requirements gaming concessionaires are subject to a principle of full disclosure, including information on shareholders and financial statements.

The law mentions 24 legal forms of gambling (blackjack, baccarat, roulette, boule, Sic bo, Fan Tan, keno, etc.).

The taxation of casino sub/concessionaires is made of a fixed part and a variable part. The variable part falls on the gross gaming revenue. The tax rate is currently of 35%, plus two contributions of up to 2% and 3% for social and economic purposes. The maximum tax is therefore 40%. In addition, a fixed premium is also payable, plus a premium per VIP table, other table, and slot machine. Gaming promoters pay taxes on commissions received.

At the present time, Macau does not license online gaming operations. Online form of gambling has the same fate as the offline one – it's forbidden. At some stage the national lottery tickets were sold online, but after the emergence of scam websites selling fake tickets, the idea was dismissed.

The total amount of core services include incorporation services, legal services and delivery of documents by courier mail

Price16 500 USD

including incorporation service and first year servicing, NOT including Compliance fee

Price1 300 USD

depends on registered capital amount, if the minimum amount is registered, registration fee is 100 US dollars

Price4 050 USD

including registered address and registered agent, NOT including Compliance fee

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 750 USD

Price705 USD

for 1 year, not including POA

Price530 USD

Company’s tax residence certificate for access to double tax treaties network

issued by tax authorities after company registration (M1 form) or in a year after rigistration (M8 form) indicating a company name, tax number and tax exemption.

This document plays a role of Certificate of Incumbency and Certificate of Good Standing if such are needed due to the non-existance of both certificates in Macau

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

simple company structure with only 1 physical person

Price150 USD

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 USD

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 USD

Price100 USD