Legal system of Norfolk Island is based on English common law and the laws of Australia.

Norfolk Island is an external territory of Australia, governed in accordance with the Norfolk Island Act 1979. In 2015, changes were made to the legal and administrative mechanisms of Norfolk Island.

Since July 1, 2016, the rules for registering commercial enterprises that apply on the mainland have been applied on Norfolk Island.

Company registration is administered by the Australian Securities and Investments Commission (ASIC).

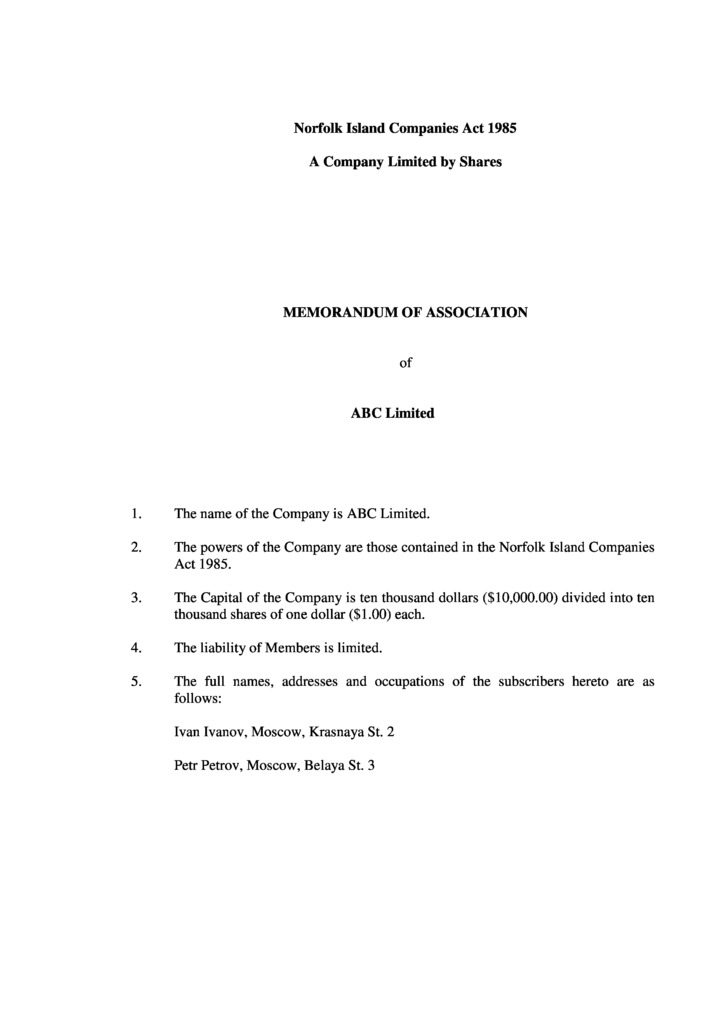

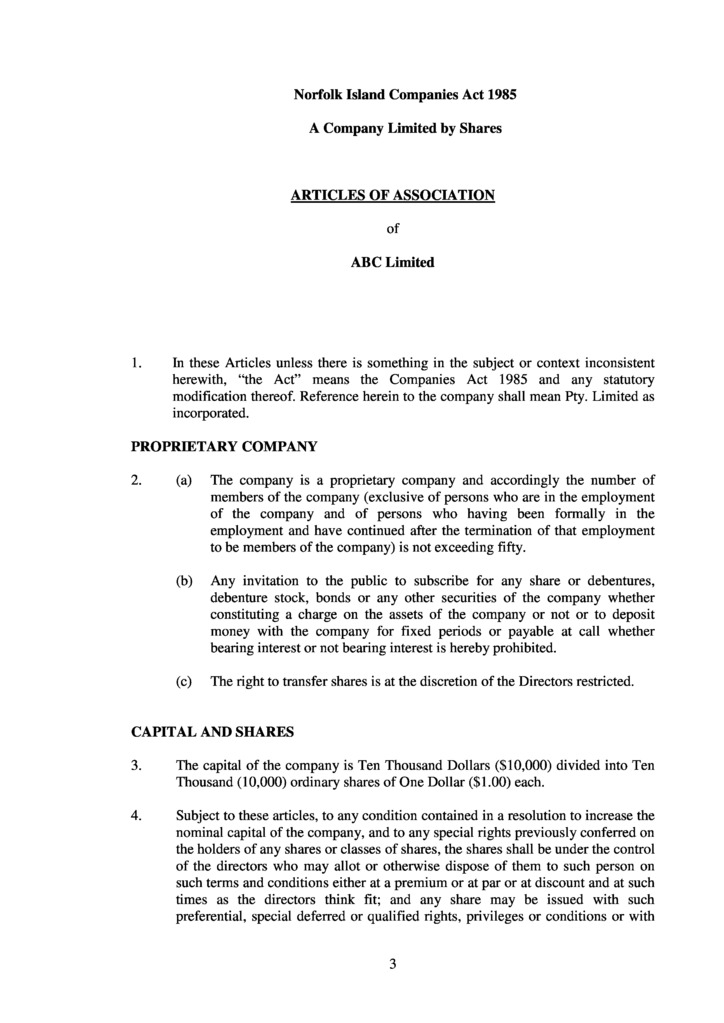

The main organizational and legal forms of companies on Norfolk Island (in accordance with the Companies Act 1985) are:

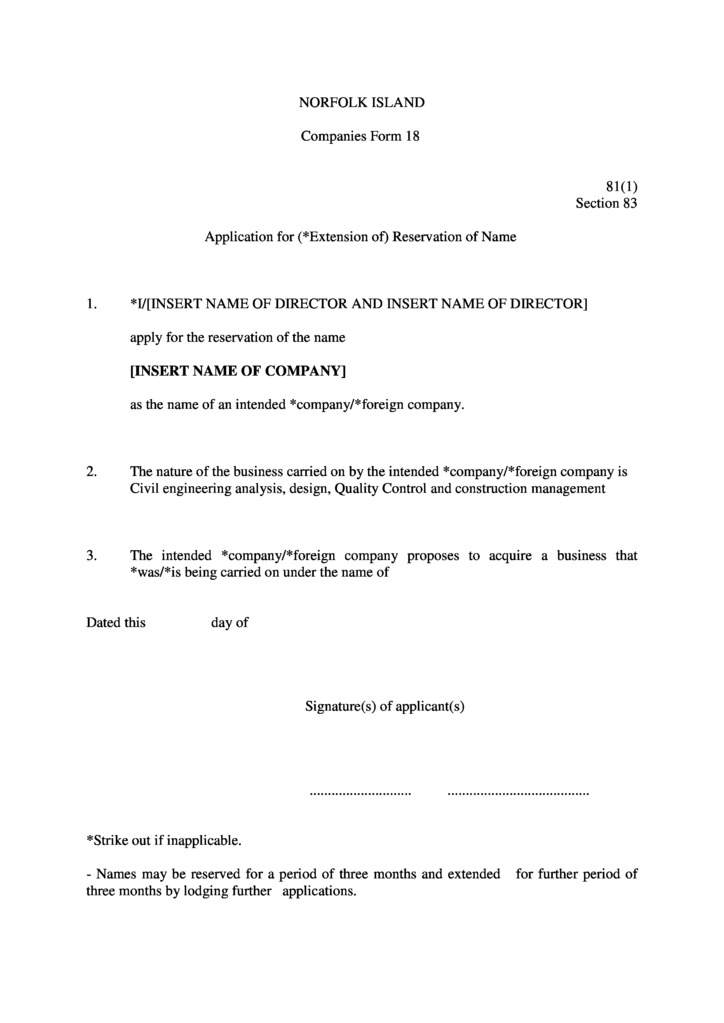

In Norfolk, the following requirements apply to company names:

1. Verification and selection of an acceptable company name and structure.

The company name can be registered with the Australian Securities and Investments Commission.

2. Payment for services.

3. Preparation of documents for submission to the Registry.

Required documents:

4. Company registration.

Registration takes approximately 5 business days from the date of submission of all necessary forms and documents to the Registry.

The Australian Securities and Investments Commission assigns each Australian company a unique number - Australian Company Number (ACN).

5. Obtaining unique numbers for business identification.

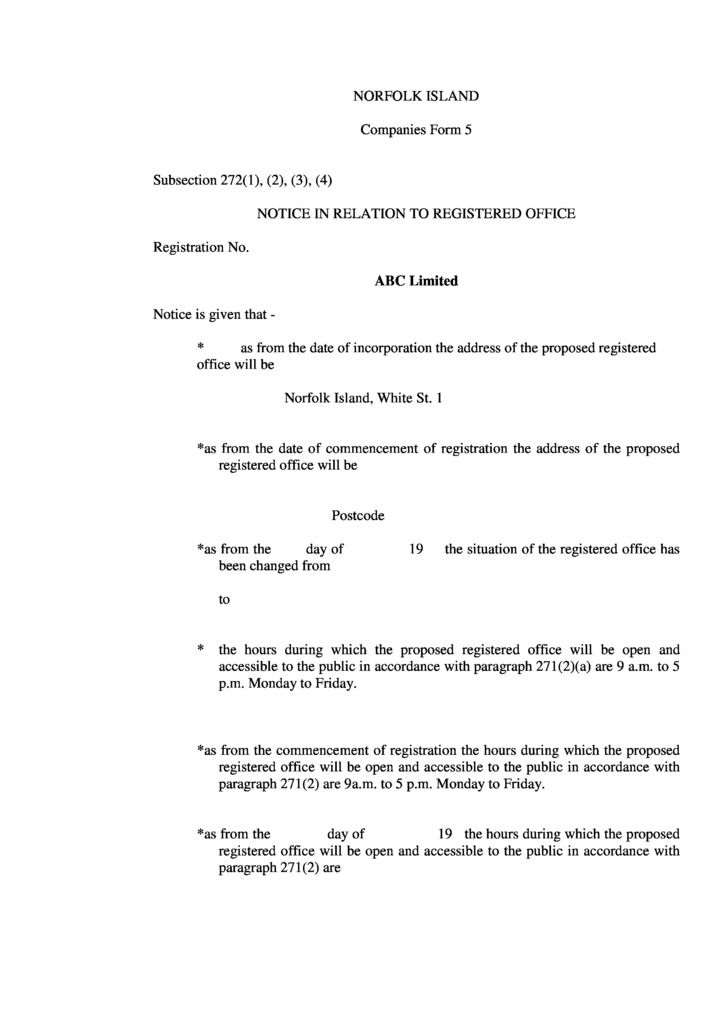

A company in Norfolk must have a registered office within Norfolk. The office must be located in a building and must be open to visitors. Any change to the registered office must be notified to the Registrar within 7 days of the change.

All registers, including the register of shareholders, register of directors, etc., must be kept at the registered office.

There are no mandatory requirements for the presence of a company seal.

The redomiciliation of companies to or from Norfolk is permitted.

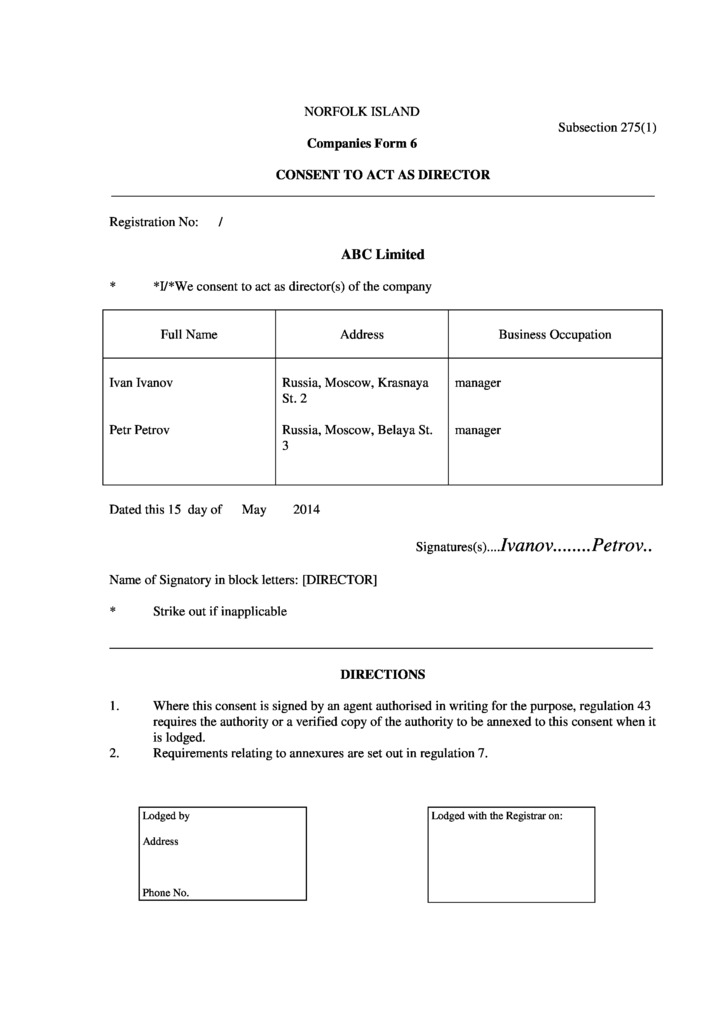

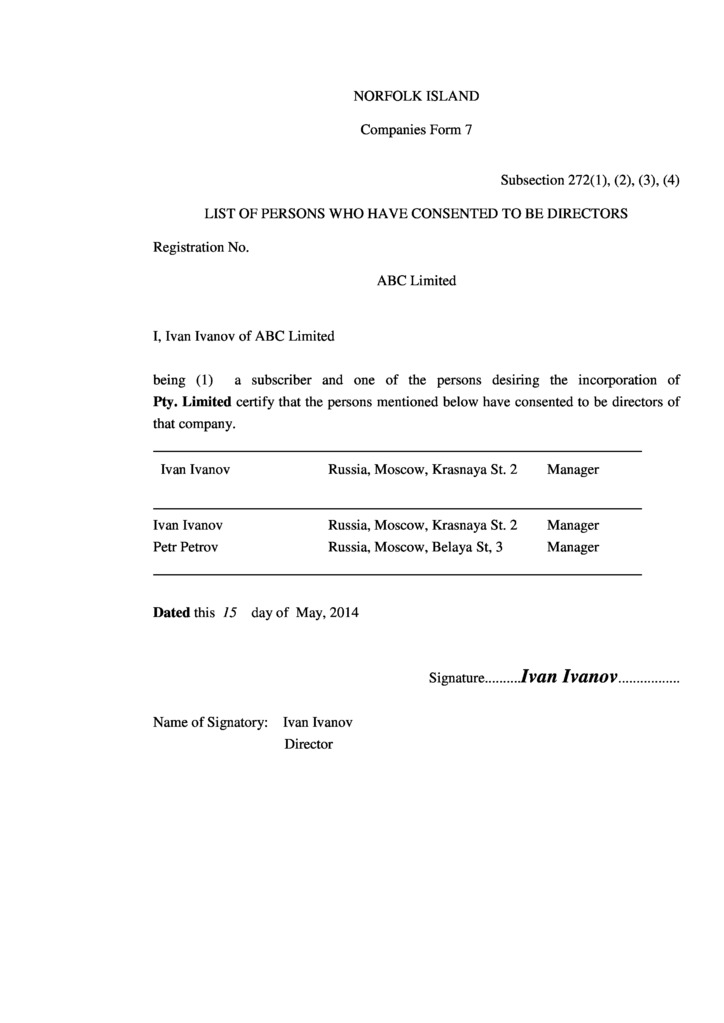

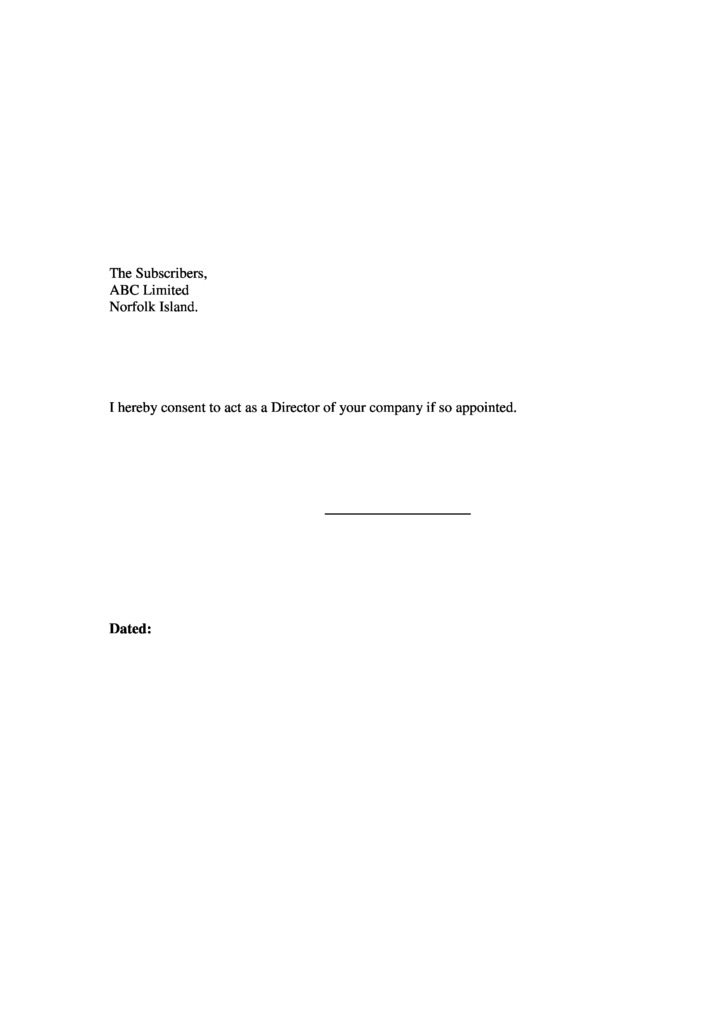

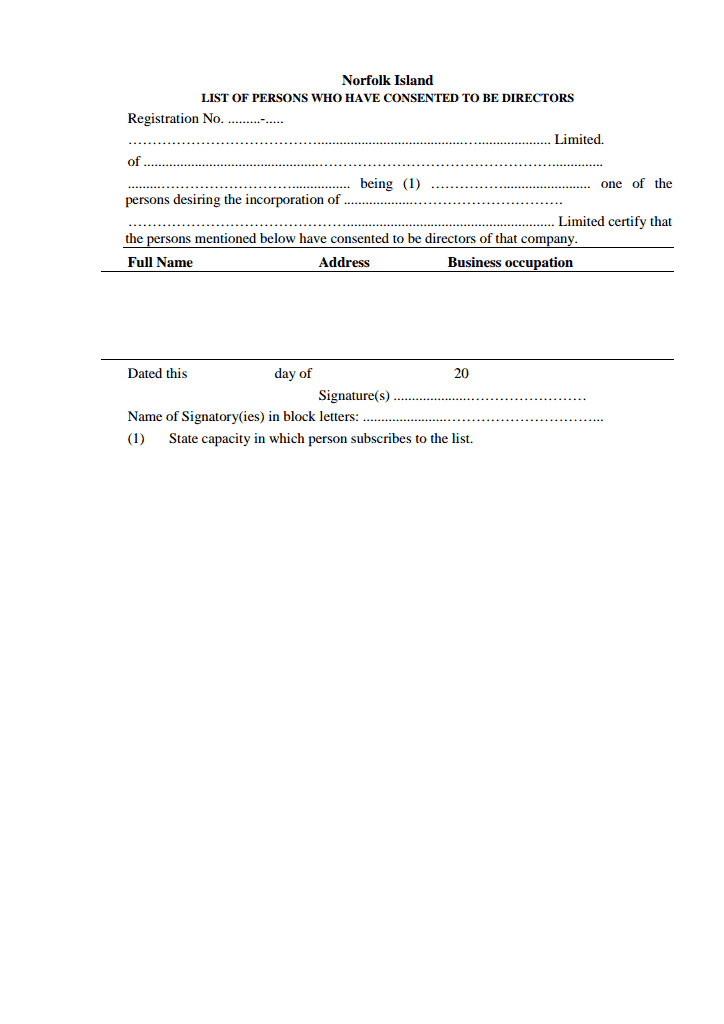

A private company in Norfolk must have at least one director. The director must be a resident of Australia.

Only a person who has reached the age of 18 can be appointed as a director of the company.

The company must notify the Securities and Investments Commission within 28 days of the appointment of a director or deputy director.

Information about directors is publicly available. A nominee service is possible.

Director meetings must be held annually. The venue may be Norfolk or any other location.

Private companies in Norfolk are not required to have a secretary, but if they have one or more secretaries, at least one of them must be an Australian resident.

The secretary is appointed by the director.

A person who has reached the age of 18 may be appointed as secretary.

The company must notify the Securities and Investments Commission within 28 days of the appointment of the secretary.

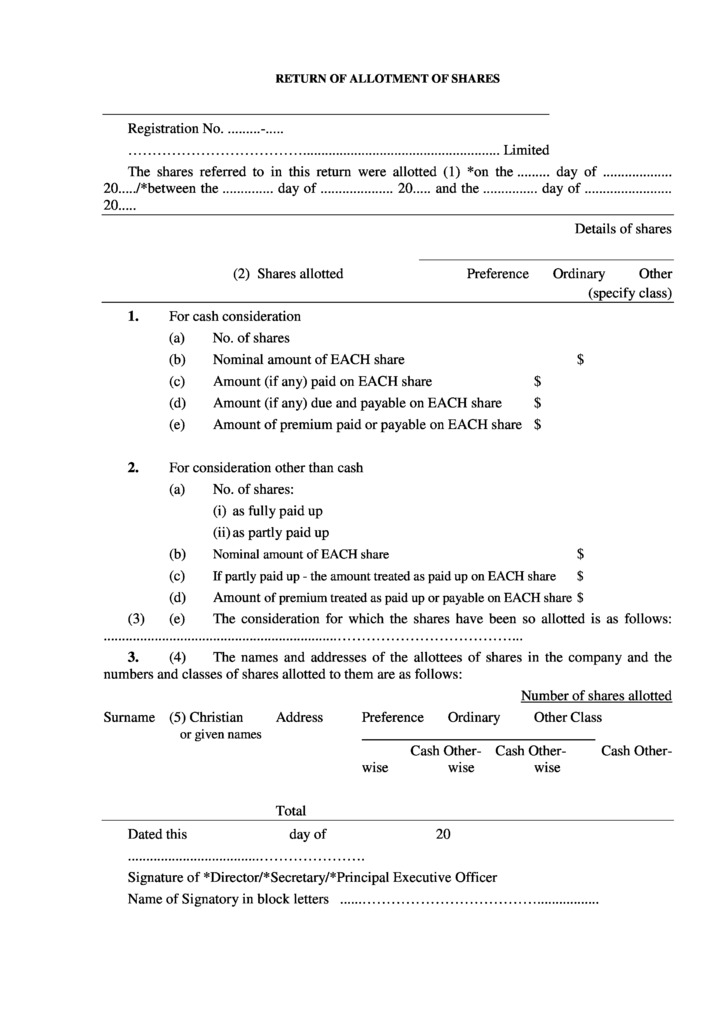

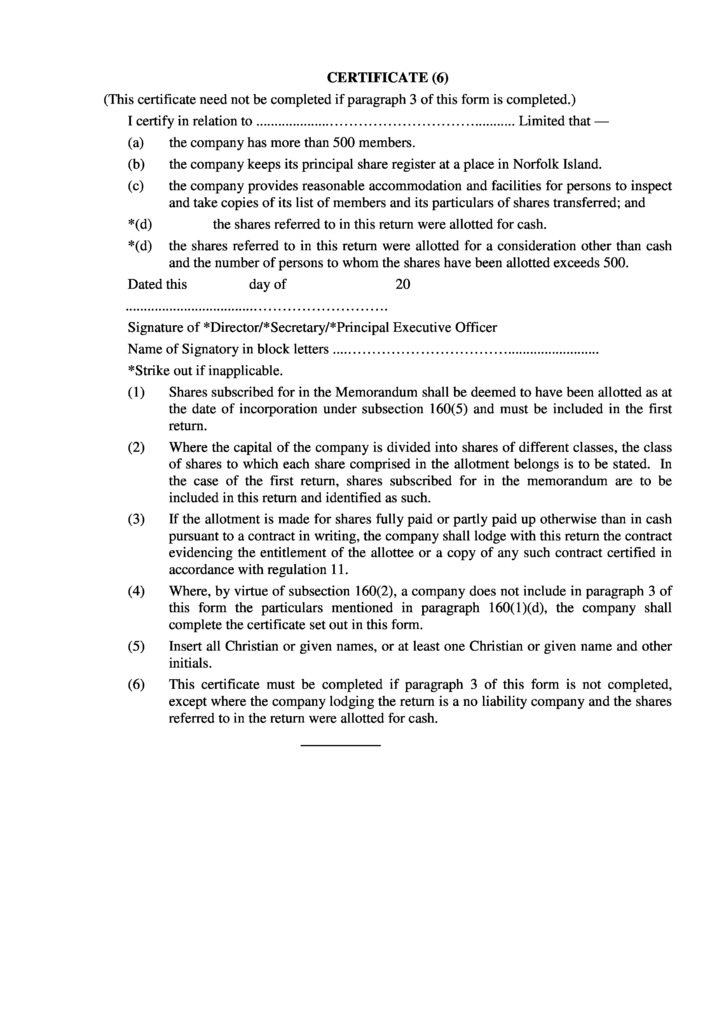

A private limited liability company must have at least one shareholder. The Securities and Investment Commission may file a petition with the court to liquidate the company if it has no shareholders.

A company must have no more than 50 shareholders who are not employees if it:

Shareholders may be individuals or legal entities. There are no residency requirements.

The company must maintain a register of shareholders, which must contain the names and addresses of the shareholders, as well as the number of shares held by each shareholder. The register of shareholders is publicly accessible.

Australia is currently considering reforming its ultimate beneficial owner (UBO) disclosure regime with a view to enhancing corporate transparency and bringing it into line with international standards, such as those set by the FATF.

There are no minimum requirements for the authorized capital of a private limited liability company.

Bearer shares and shares without par value are prohibited.

Price6 000 USD

(including incorporation tax and state registry fee)

Priceincluded

(Stamp Duty) and Companies House incorporation fee

Price5 000 USD

(including registered address and registered agent)

Price250 USD

DHL or TNT, at cost of a Courier Service

Pricefrom 750 USD

Paid-up “nominee director” set includes the following documents

Paid-up “nominee shareholder” set includes the following documents

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 USD

Price150 USD

Price200 USD

Price450 USD

Price100 USD