The civil law system of Slovakia is based on Austro-Hungarian codes. The legal code was modified to comply with the obligations of Organization on Security and Cooperation in Europe (OSCE) and to expunge the Marxist-Leninist legal theory. Slovakia accepts the compulsory International Court of Justice jurisdiction with reservations.

The principal forms of business organization in Slovakia are:

The most common structure in Slovakia is the limited liability company.

There is a range of requirements to the company name in Slovakia:

The following steps are required to incorporate a company in Slovakia:

The formation of a new company in Slovakia takes about 2 weeks.

The company in Slovakia must lawfully use premises for the purpose of maintaining its registered office. The registered office must be stated in the Foundation Deed and supported in the application for the registration of the company in the Commercial Register with evidence of the title of the company to its premises (such as an ownership deed for the premises, a lease agreement or a declaration of the owner of the premises allowing the company to register its office therein). Often at the time of its foundation, a company uses temporary (virtual) premises/office and obtains permanent premises at a later stage.

There are no statutory requirements for a company in Slovakia to have a seal.

The redomiciliation of companies to or from Slovakia is permitted.

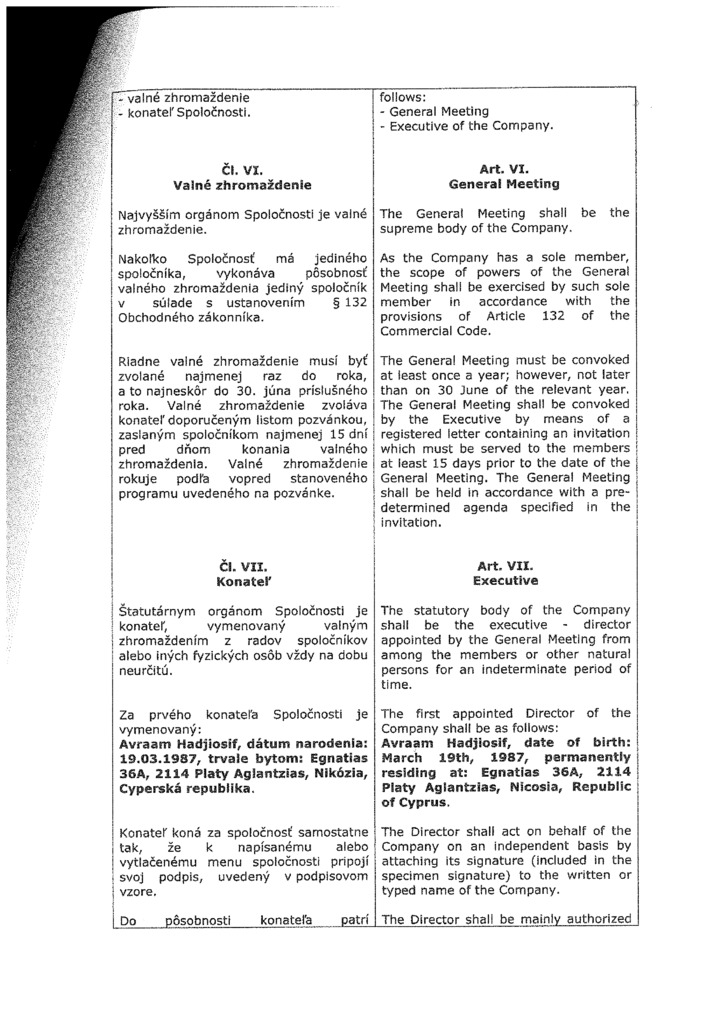

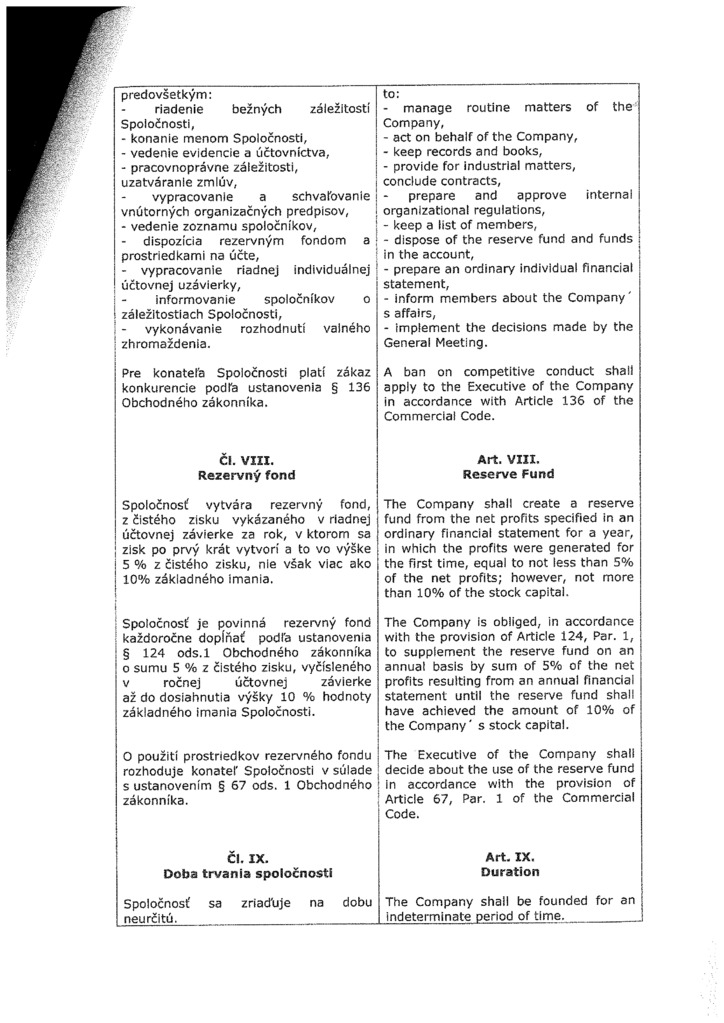

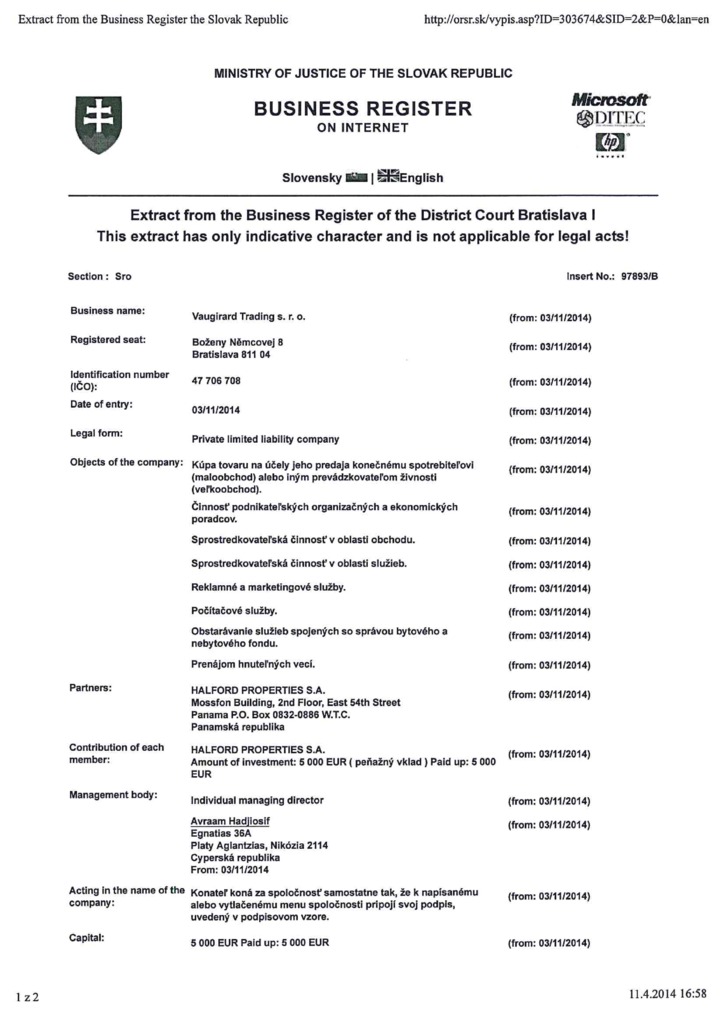

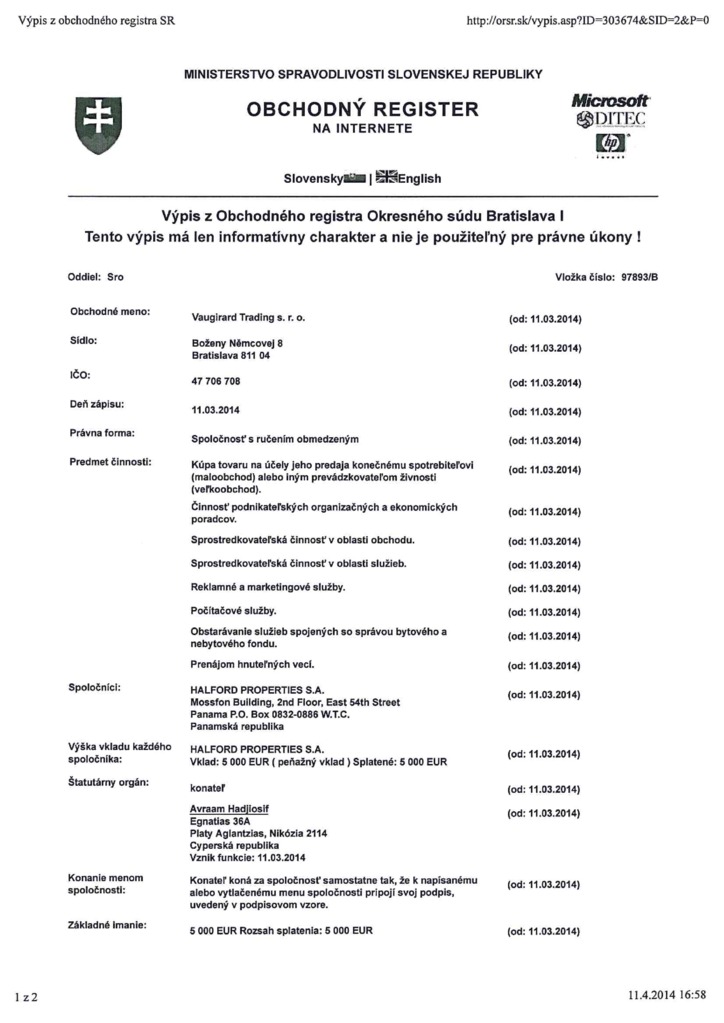

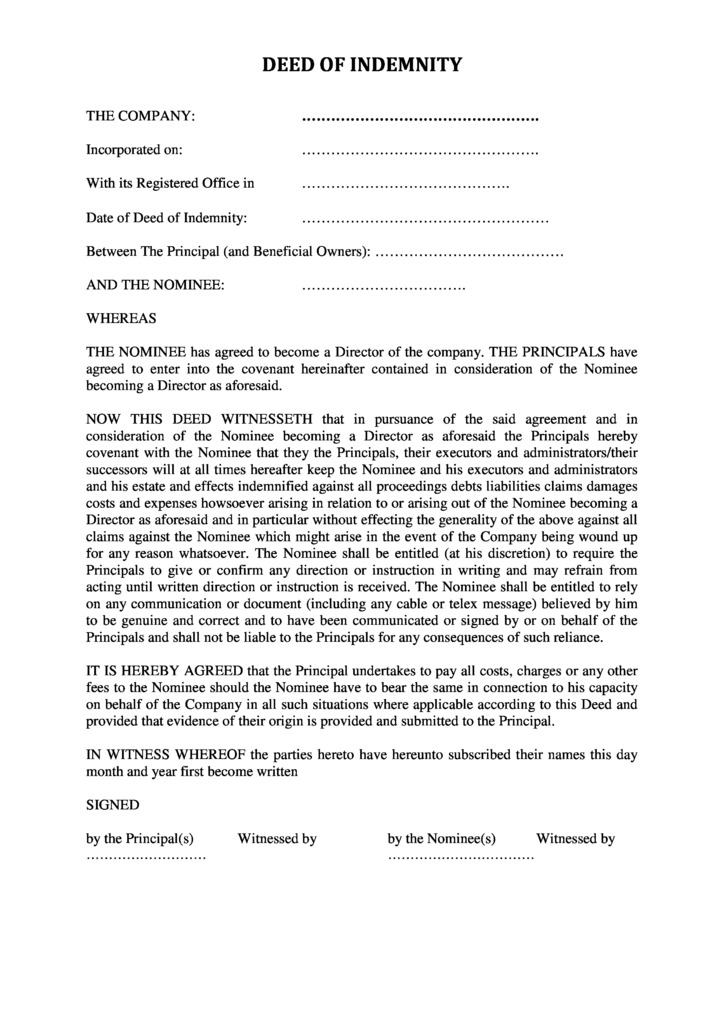

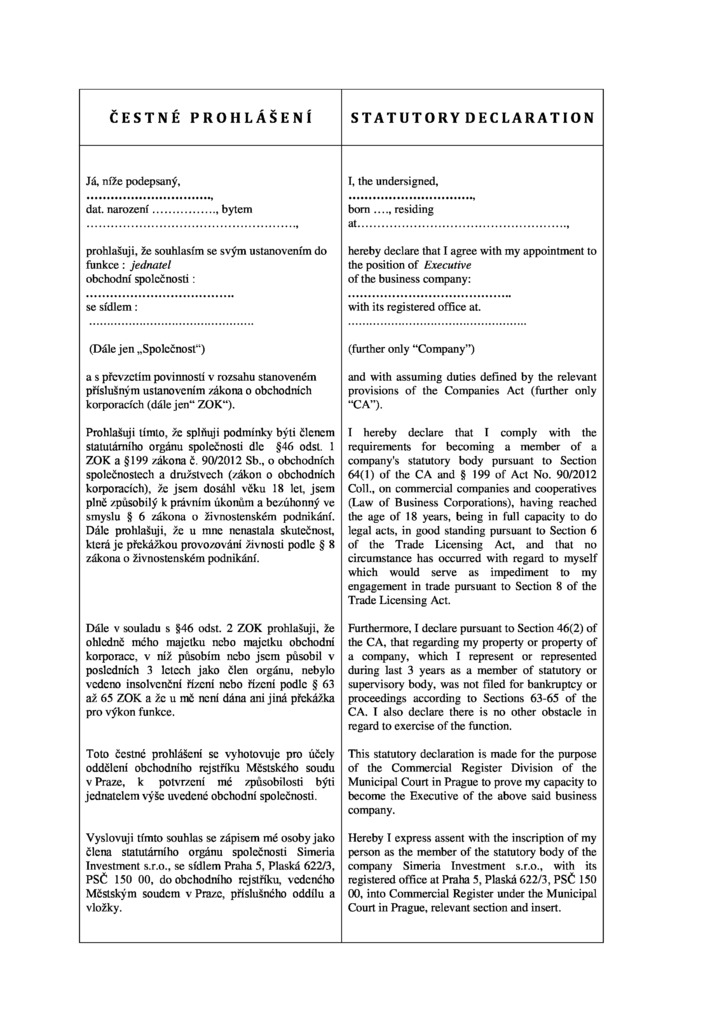

Every company in Slovakia must have at least on director (executive). The general meeting appoints one or more executive directors as the statutory body of a company in Slovakia; only an individual can be appointed an executive director. Although there are no nationality requirements for Executives, a non-EU or non-OECD citizen must have a residence permit in Slovakia. Executive directors decide on all matters of the company not vested to its general meeting, act on behalf of the company and represent the company in relations with third persons.

Directors’ information appear on public profile.

Directors should hold Board’s meetings at least once a year. The place of the meeting can be in Slovakia or anywhere else.

Slovak companies are not required to appoint a company secretary.

Each company in Slovakia must have minimum one shareholder (but no more than 50). There is no restriction on the nationality or residency of the shareholders. The shareholders can be individuals or legal persons.

An LLC with only one member (shareholder) may not be the sole founder or member of another LLC. This rule also applies to foreign entities. In addition, the LLC may not be established by a person having outstanding tax or customs liabilities.

The general meeting of shareholders is the supreme body of an slovakian company empowered to decide on all matters vested to it by law or by foundation agreement; general meeting may reserve by itself the right to decide on certain matters. The general meeting decides in most matters by a simple majority of votes of shareholders present at the meeting. In certain most important matters stipulated by law (such as adopting and amending the foundation agreement or increasing or decreasing the registered capital) a two-third majority is required; foundation agreement may stipulate a higher majority for approval of certain decisions.

In 2018, legislation came into force in Slovakia requiring companies to report information on their ultimate beneficiaries to the Trade Register from the end of 2019.

Information on ultimate beneficiaries is classified and is available to public authorities (Financial Police, Ministry of Finance, National Bank of Slovakia, National Security Authority, etc.) and private persons (banks, auditors, accountants, tax consultants, etc.).

Data to be submitted about the beneficiary: full name; identification number (rodné číslo) or date of birth if no identification number has been assigned; address of permanent residence; citizenship; type and number of ID card; data confirming the status of the beneficiary.

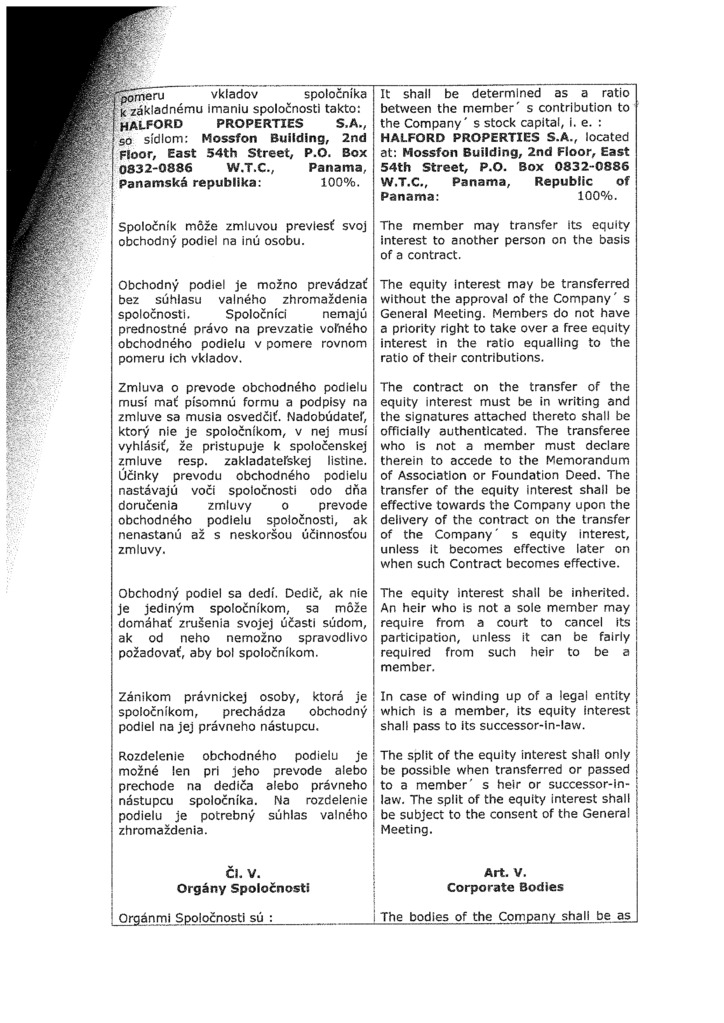

The minimum registered capital for an LLC is EUR 5,000 and the minimum contribution by one member (shareholder) is EUR 750. The registered capital must be paid up within the time period set out by the Foundation Deed, however at the latest within five years from the date of incorporation.

If the LLC is founded by a single founder, 100% of the registered capital must be paid up before submission of the petition for registration with the Commercial Register. If the LLC has more than one founder, at least 30% of the contribution of each member to the registered capital of the company and overall at least 50% of the minimum registered capital (EUR 5,000) has to be paid up prior to the submission of the petition for registration with the Commercial Register.

As opposed to shares in a joint stock company, ownership interests are not securities and no share certificates are issued. Further, they are not publicly tradable.

LLC ́s members and their ownership interests are listed in the Commercial Register.

An LLC must create a reserve fund whose amount must eventually be at least 10% of its registered capital. The reserve fund may either be created at the time of the establishment of the LLC or as soon as it records profits. In the latter case, the contribution to the reserve fund must amount to at least 5% of the company’s net profits (until it amounts to 10% of its registered capital).

Price6 950 EUR

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Stamp Duty and Commercial Registry incorporation fee

Price3 340 EUR

including registered address and registered agent, NOT including Compliance fee

Price250 EUR

DHL or TNT, at cost of a Courier Service

Pricefrom 750 EUR

Paid-up “nominee director” set includes the following documents

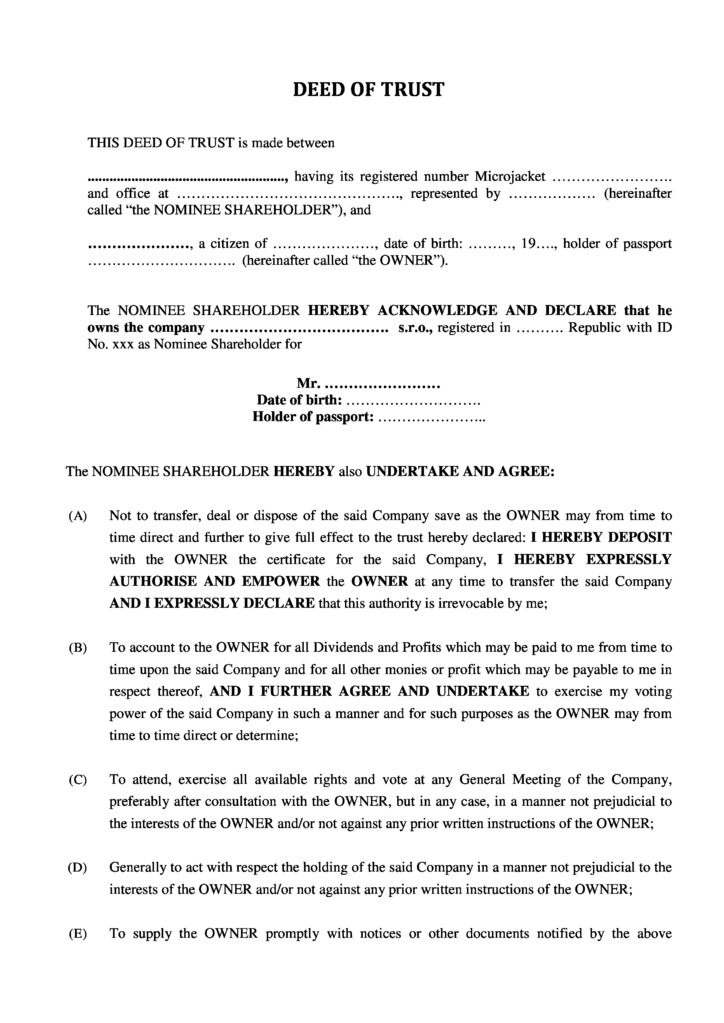

Paid-up “nominee shareholder” set includes the following documents

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

Price350 EUR

simple company structure with only 1 physical person

Price150 EUR

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

Price200 EUR

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

Price450 EUR

Price100 EUR