The legal system of Switzerland is based on civil law system.

The main source of law is Constitution of 1874.

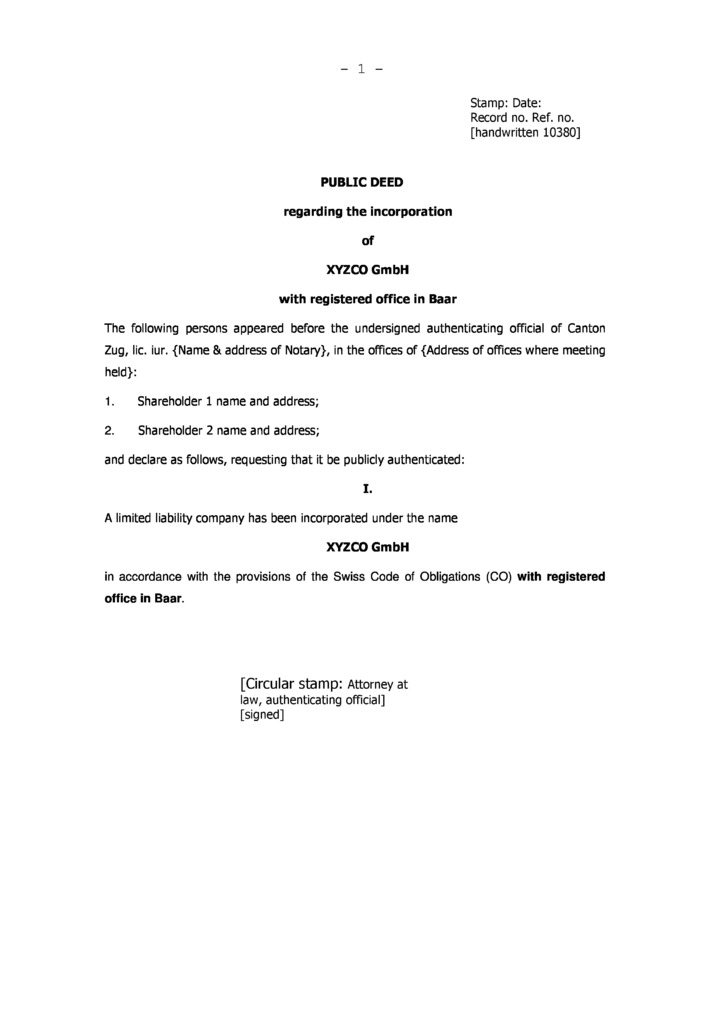

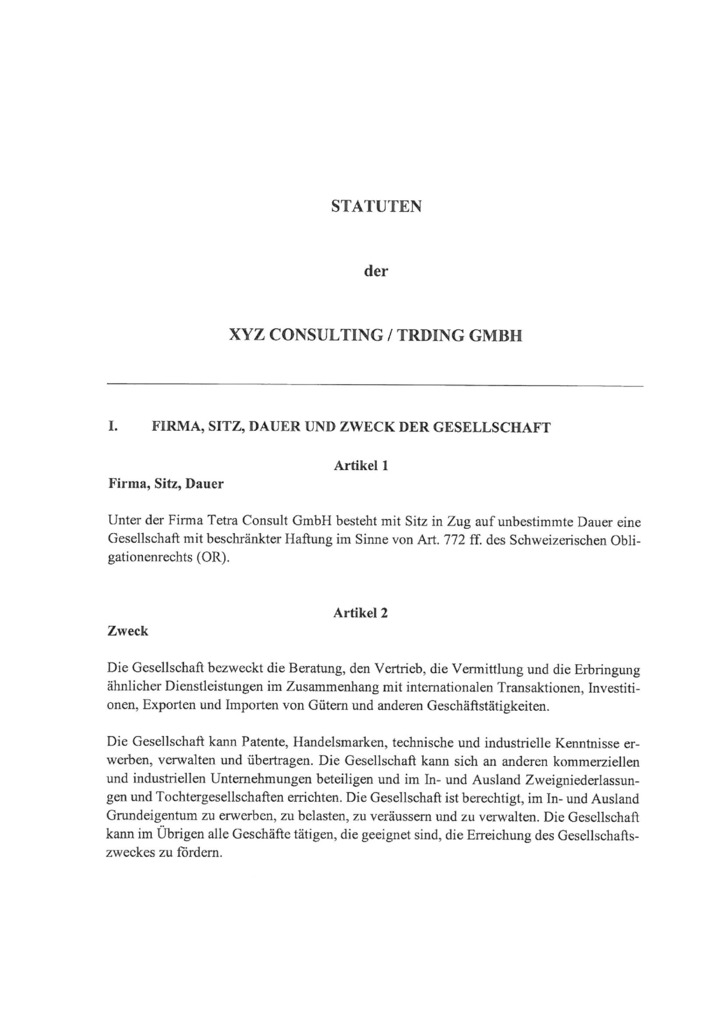

The Swiss Limited Liability Company is governed by the Swiss Code of Obligations (1912) revised in 2011.

The principal forms of business organization in Switzerland are:

The most common structure is the private limited liability company (GmbH).

When planning to incorporate your company in Switzerland, you can use the Zefix website (www.zefix.admin.ch) to check whether you can use your company name – or any alternative. Zefix is the central company index of Switzerland which belongs to the Commercial Registry.

The company or business name under which a commercial enterprise is operated can be freely chosen, as long as it complies with legal regulations.

Stock corporations (AGs) and limited liability companies (GmbHs) must specify the legal form as part of the company name - GmbH (or its equivalent in French or Italian). However, it is also allowed to register the business name with the suffix “Ltd”, but therefore, business name for both countries have to be registered (e.g.: RealEstate33 GmbH [RealEstate33 Ltd]). The problem is that by registering only the company name with the suffix “Ltd” people would think that the company is incorporated in the UK or another country, where the suffix “Ltd” is obligatory or common.

Certain words such as Switzerland, International, European, Insurance, Reinsurance, Fund Management, Bank, Collective Investment Schemes are sensitive and may have different capital requirements.

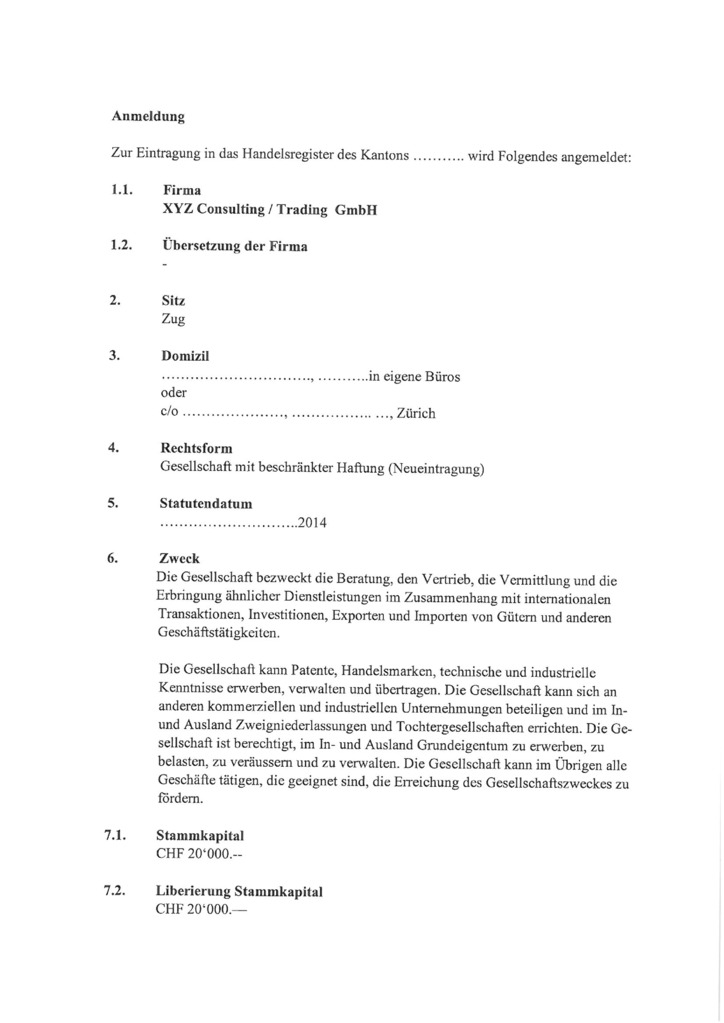

The following steps are required to incorporate a GmbH in Switzerland:

1. It is necessary to determine:

2. Рay for the services.

3. Submit the apostilled documents of the beneficiary(ies) and the power of attorney required for company registration.

4. Verification of the company name at the Chamber of Commerce.

Once the name of the future company passes the check at the Chamber of Commerce, you can proceed to the preparation of documents for registration.

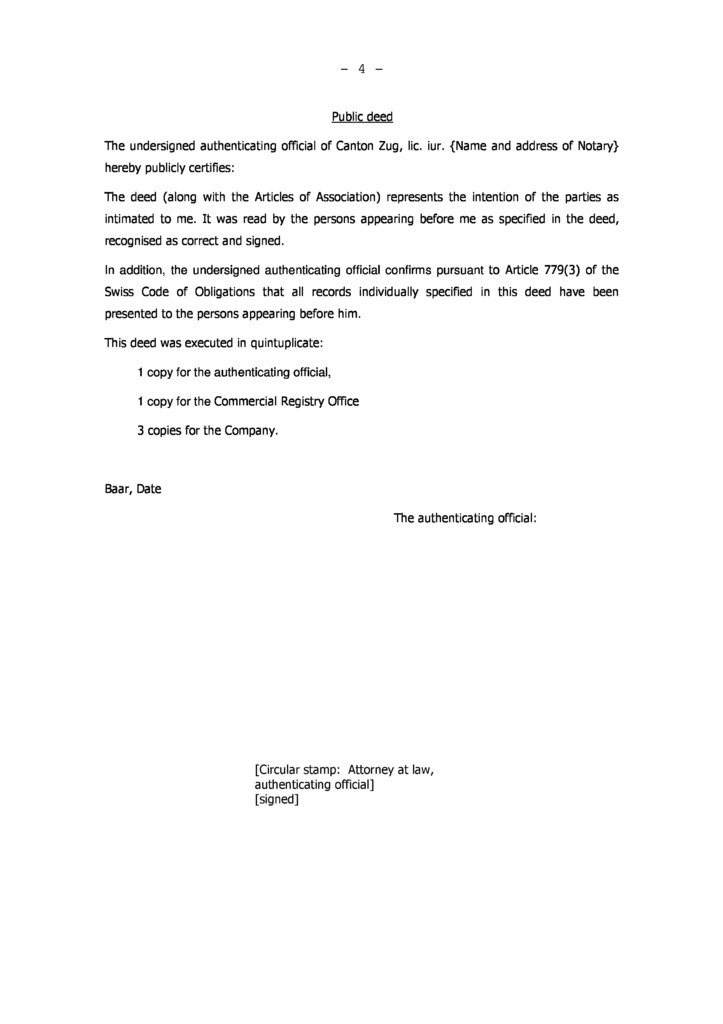

5. Draw up and sign the Memorandum of Association in the presence of the notary, who will notarize the personal corporate signatures on the application and certify the Memorandum of Association and the Deed of Incorporation.

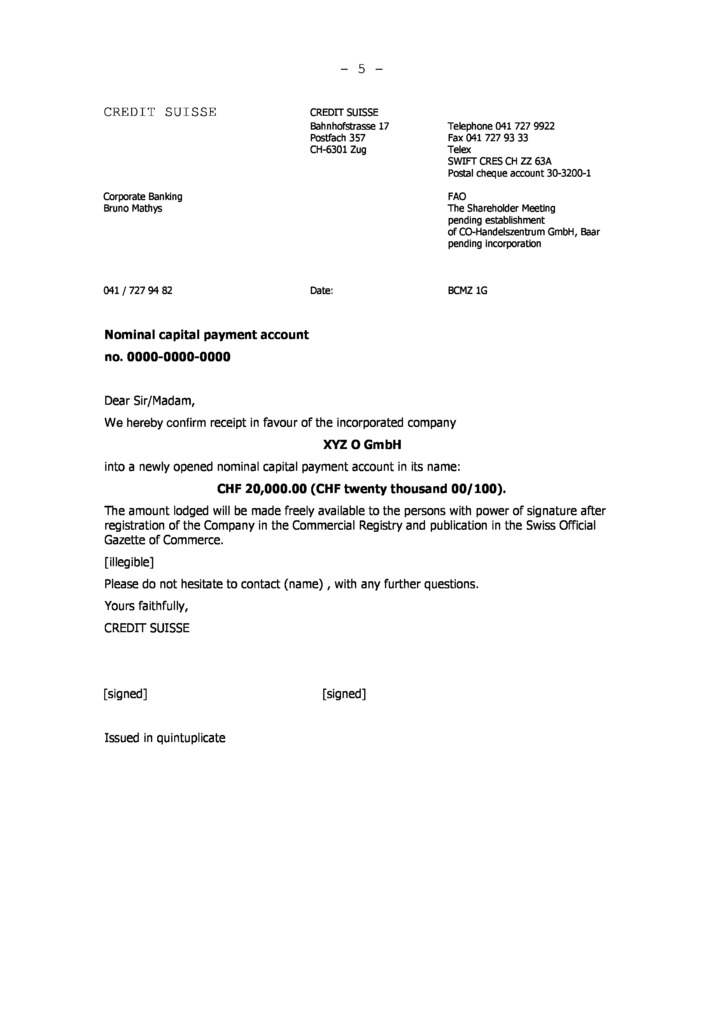

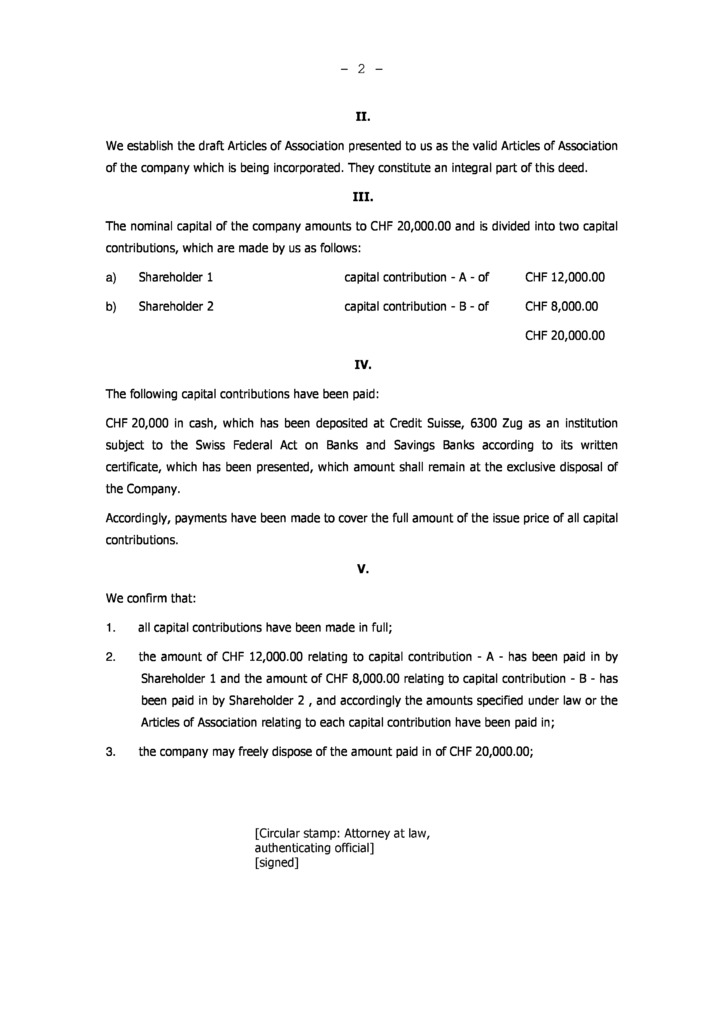

6. Make payment of the share capital to the bank in an escrow account.

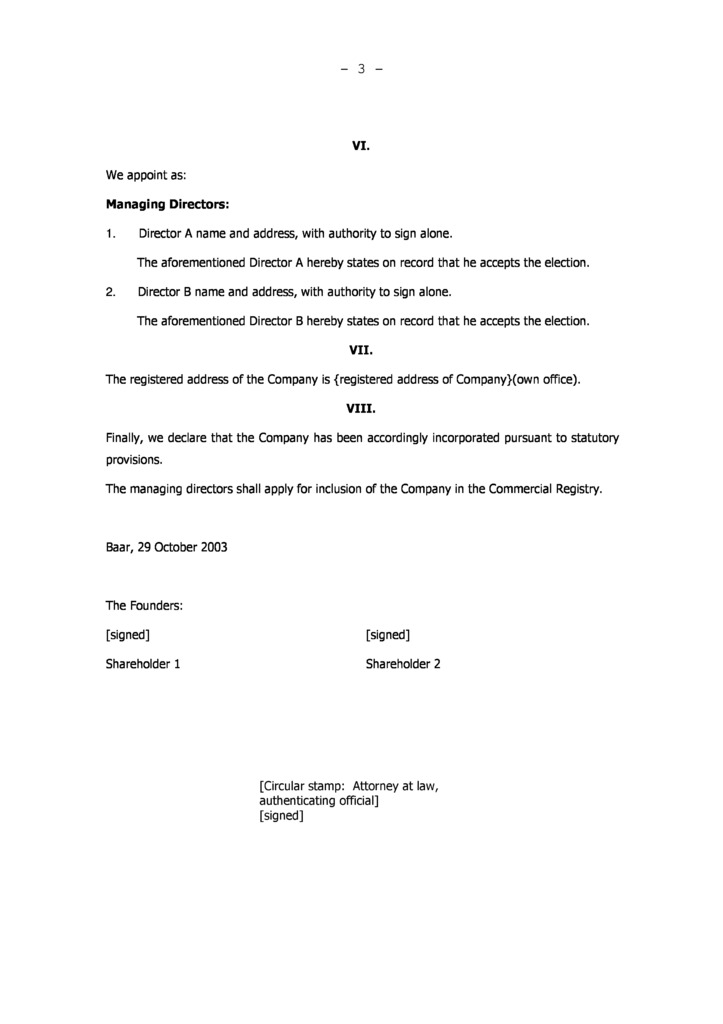

7. Submit the deed certifying the memorandum of incorporation to the local registry of companies to obtain a certificate of incorporation.

8. Pay the Stamp Duty when the taxation amount is received by mail (1% of the capital, with the first CHF 1 000 000 being exempt from the duty).

9. To register for VAT within 30 days after the grounds for VAT taxation appear. Applicable if the threshold is CHF 100 000 or the company has import and export operations.

10. Register employees with the social security system (federal and cantonal authorities) (if applicable).

Setting up a new GmbH generally takes about 3 weeks after the necessary documents have been submitted. These deadlines can be shorter in simpler cases, depending on the canton.

In general, no approvals from special bodies, chambers of commerce or professional associations are required to register a GmbH. However, doing business in a specific or professional area may require a special license or diploma. All sectors of business are open to foreign investment, there is no requirement for a certain percentage of Swiss residents.

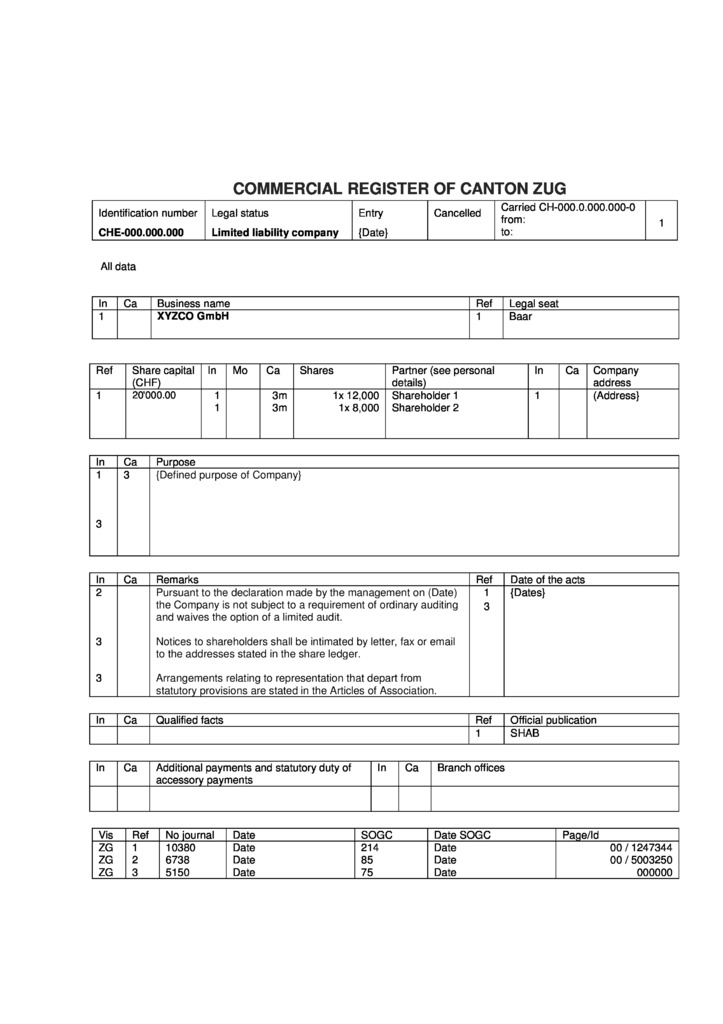

The commercial register includes all commercial enterprises doing business in Switzerland. It specifies each company’s extent of liability and its authorized representatives. Its central focus is its public disclosure role.

Announcements about the registration and removal of companies from the register are published in the Swiss official Gazette of Commerce (SOGC).

Every business must have an address in Switzerland at which the registered offices can be contacted. This address must contain the following:

A differentiation must be made as to whether the address is the own office of the company or simply a “c/o” address. Own office would be a location which a legal entity owns or leases and where it conducts most of its administrative business where the receipt of any kind of correspondence is possible. As long as these requirements are not met, the address must be considered a c/o address. A PO Box cannot be considered a domicile in the legal sense.

Register of shareholders and directors, minutes of shareholders’ and directors’ meetings, accounting records should be kept at the registered office.

There are no statutory requirements for a Swiss company to have a seal.

The redomiciliation of companies to or from Switzerland is permitted.

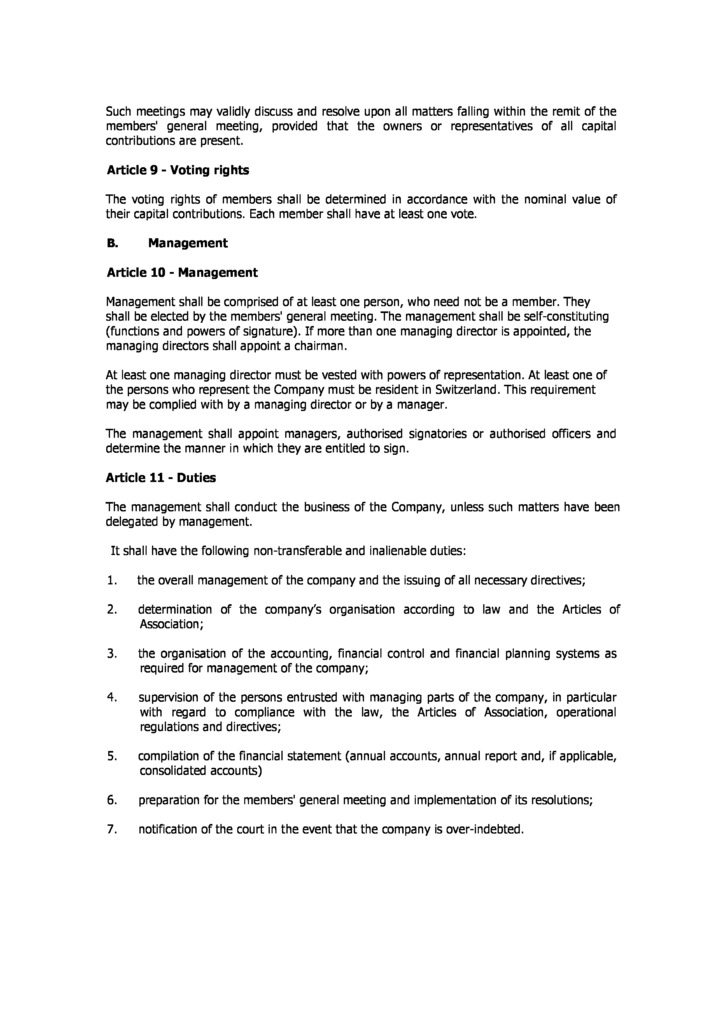

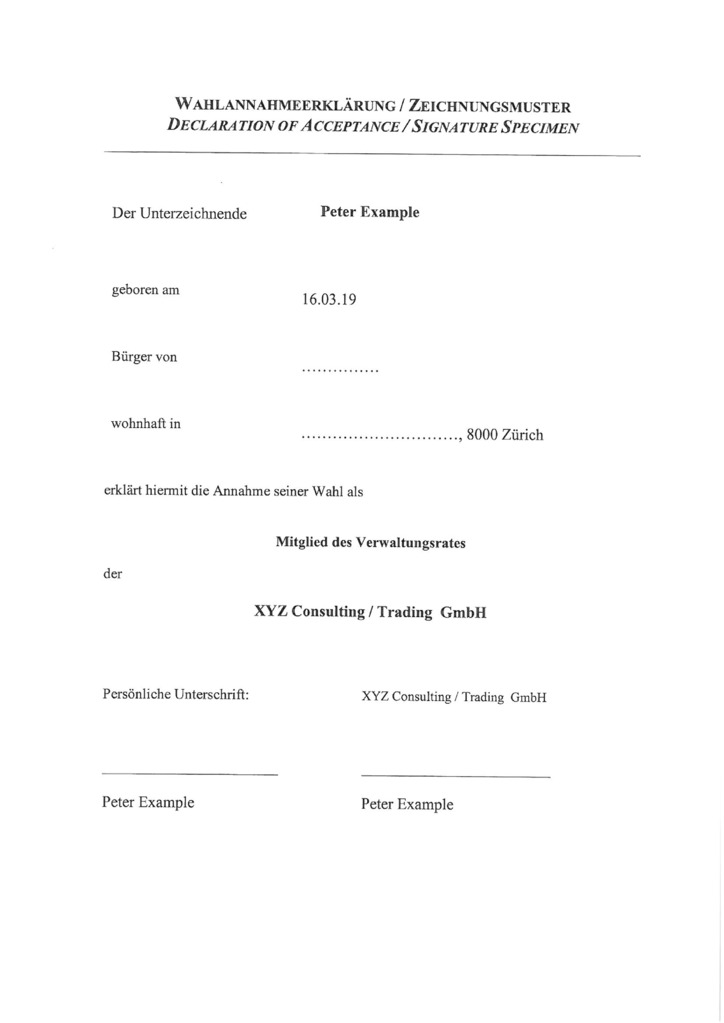

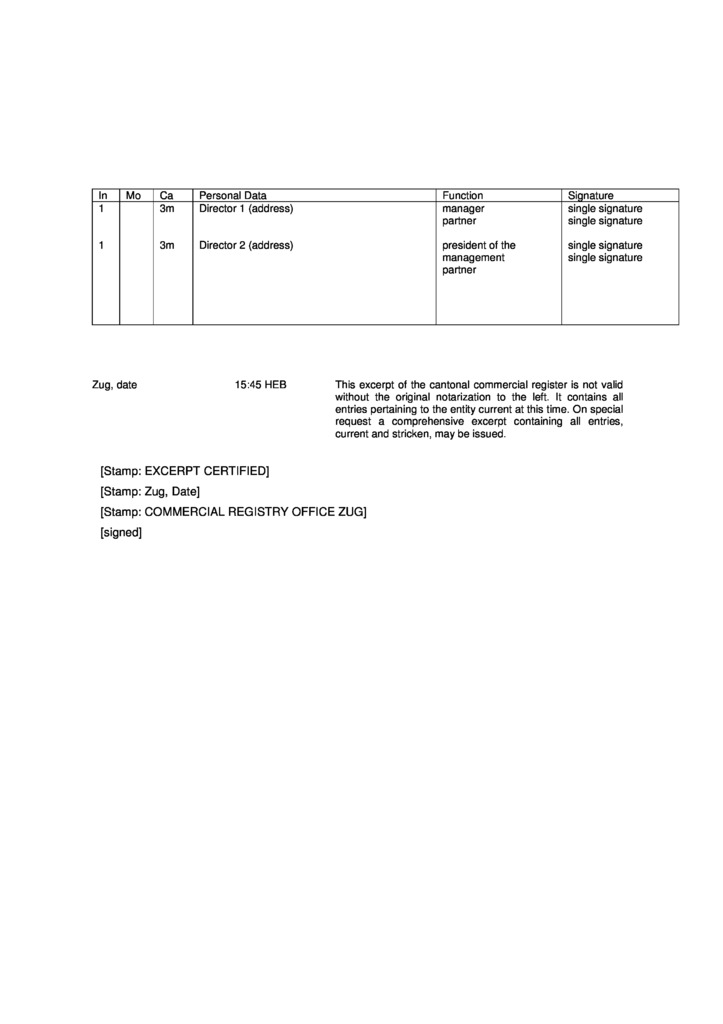

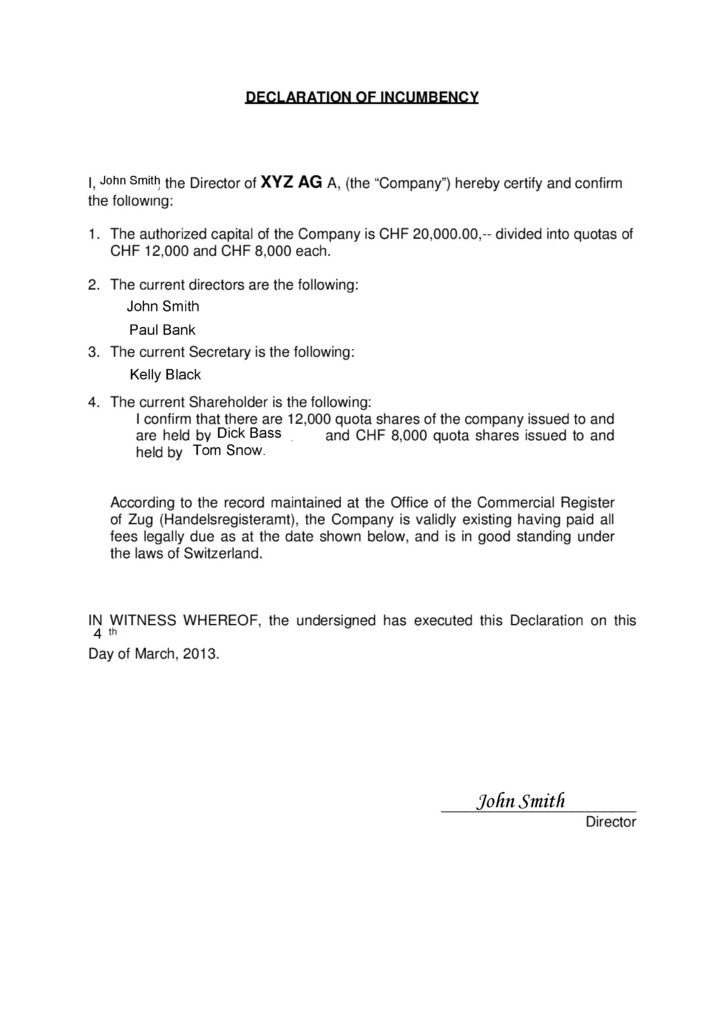

The minimum number of directors of a Swiss GmbH is one, and at least one director must be resident in Switzerland. If there is more than one director, the majority of the board of directors must be Swiss residents. There are no other restrictions on the nationality or residency of the directors.

Corporate directors are not allowed.

Since a board of directors is not required, there are no requirements to the meetings of board of directors.

Directors’ information appears on public record.

Swiss companies are not required to appoint a company secretary.

Swiss GmbH can have one or more shareholders, which can be individuals or legal entities, residents or non-residents of Switzerland.

The data of the shareholders of GmbH is entered into a public register.

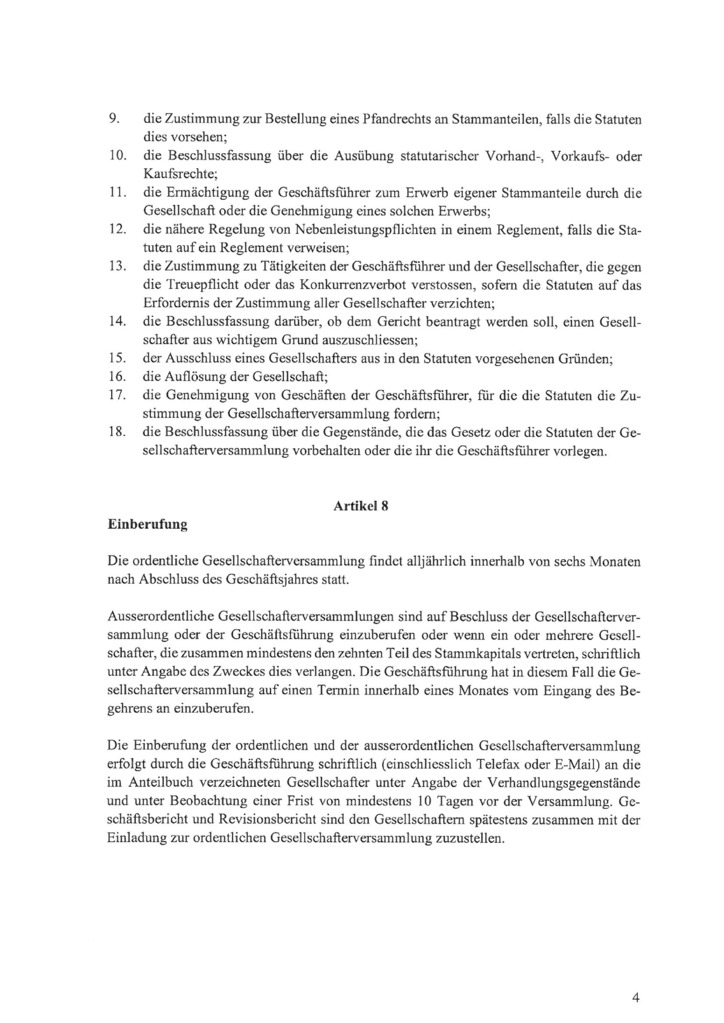

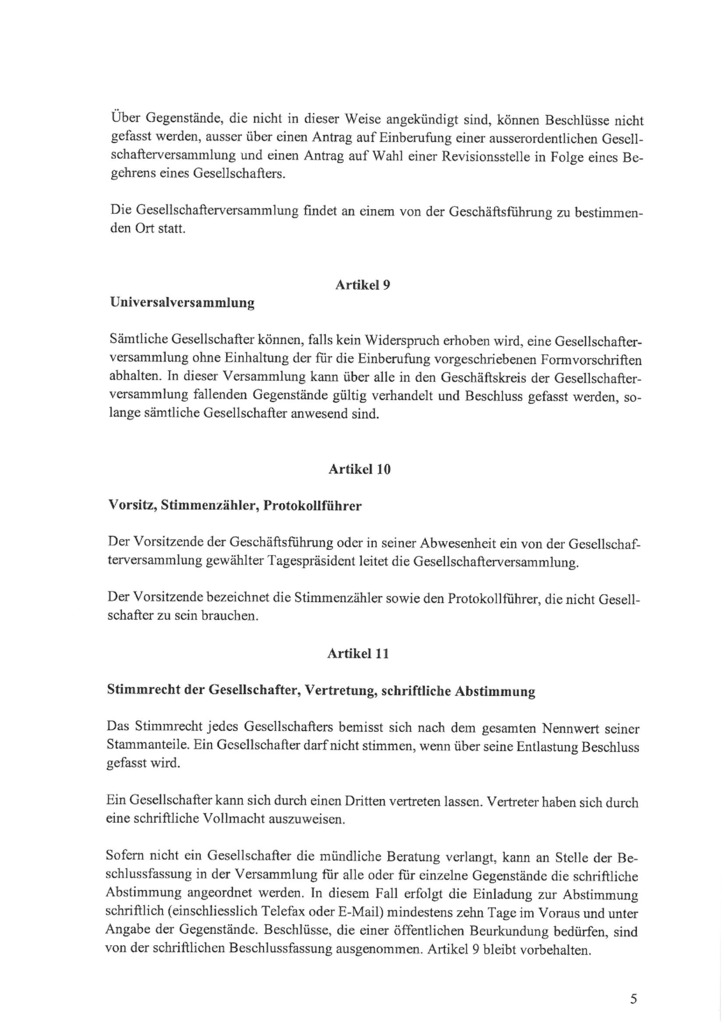

An Annual General Meeting of the shareholders must be held within 6 months of the end of the financial year. Generally 20 days notice must be given of an intended meeting unless all appropriate parties are represented directly or by proxy. Meetings may be in or outside of Switzerland.

Since 2015, Swiss companies have been required to keep a register of their beneficiaries. The register contains the names and addresses of the beneficiaries. Such registers are kept in such a way that they are always available for verification within Switzerland.

Since 2021, the identification of beneficiaries of trusts and funds has been introduced.

The minimum capital for a Swiss GmbH is CHF 20 000 and the maximum is CHF 2 000 000. The share capital must be paid in full at the time of registration.

The share capital of a Swiss Limited Liability Company can be denominated in any currency. It must be deposited in a Swiss bank (blocked account for company foundation).

Each shareholder has an interest in the nominal capital in the form of one or more nominal shares having a nominal value of at least CHF 100.

The Anglo-Saxon trust law has not been adopted into the Swiss legislation. There is no Swiss substantial law on trusts and no such thing as a Swiss domestic trust. Therefore, a trust can only be established according to foreign law, whereby the settlor may choose the governing law. However, despite the lack of substantial trust provisions, Swiss courts have been dealing with trusts for many years.

Switzerland being one of the largest trust administration centers in the world recognized eventually the Hague Convention on the Law Applicable to Trusts and on their Recognition of 1st of July 1985 with effect as of 1st of July 2007 (the "Hague Convention"), resulting in the recognition of trusts as a legal structure sui generis and in the enforcement of foreign trusts.

Since 2007 it is possible to hold Swiss property in trust. In such a case, generally the trustee is the owner of the real property and is to be registered in the land register. While EU/EFTA nationals residing in Switzerland can acquire real estates without prior authorization, third-country nationals are still submitted to a preliminary administrative authorization. If the trustee or the beneficiaries qualify as a person abroad, in principle the transfer is subject to authorization.

According to the Circular No. 30 the trust assets and the trust income will either be taxed by the settlor or the beneficiaries. Hence, a Swiss trustee is never subject to tax for the trust assets and the trust income. The trustee is regarded as the formal owner but not the beneficial owner of the trust assets.

Swiss law differs between revocable, irrevocable fixed-interest trusts and irrevocable discretionary trusts.

If a trust is qualified as a revocable trust, then the settling of the trust does not cause any change from a fiscal perspective. The settlor remains taxable and distributions to beneficiaries are treated as gifts from the settlor.

In the event of the settlor's demise, the trust becomes (for tax purposes) an irrevocable trust. Some tax authorities conclude that with the settlor's demise the settlor made a donation to the trust or the trustee and there is, therefore, an inheritance. The taxation is differs from canton to canton. Some cantons apply the highest inheritance tax rate and others take the relationship between the settlor and the beneficiaries into account and only then determine the tax rate. In most cantons the tax rate is zero if the heirs are direct descendants of the settlor. Other cantons do not follow the inheritance road but focus on whether the beneficiaries have substantial influence over the trust assets. If so, then the trust will still be treated transparently, meaning the trust assets and trust income will be taxed by the beneficiaries.

Under Circular No 30 the creation of a fixed interest trust is treated as a donation from the settlor to the beneficiaries. The tax rate applicable depends on the degree of cognation. An assessment of gift tax on the entire trust funds can violate the principle of economic capacity, in particular, if the beneficiary is only entitled to a certain amount of the trust income. Therefore, the tax would have to be limited to the capitalized amount of the income.

In the event that the Swiss resident beneficiary has an entitlement to distributions of either capital or income he is taxed in analogy to an usufructuary. The amount of his entitlement to distribution will be capitalized and the capital value of his entitlement is subject to wealth tax. Any amount distributed to the beneficiary is subject to income tax unless made out of tax free capital gains or capital.

The settlor irrevocably transferred the trust assets to the trustee and has given up any economic interest in the trust funds. The trustee cannot be taxed as he is not the beneficial owner of the trust assets.

Beneficiaries of an irrevocable discretionary trust have in general no legal entitlement to receive distributions from the trust. They have a mere expectation of benefitting from the trust. Under Swiss tax law an expectation is not taxable. However, under the Circular No. 30 a Swiss resident beneficiary of an irrevocable discretionary trust may be subject to tax if he is qualified as the beneficial owner of the trust assets.

If the beneficiary does not qualify as a beneficial owner, then the Swiss resident settlor remains tax liable for the trust fund and the trust income just as if he had set up a revocable trust. Therefore, the trust fund and trust income are still attributed to the settlor and distributions to beneficiaries are treated as gifts.

The Circular No. 30 provides for an exception of this principle in the event that the settlor was resident abroad when the trust was set up. In that case the Circular No. 30 accepts that neither the trust fund nor the trust income can be attributed to the currently in Switzerland residing settlor or the beneficiaries. Only distributions received by a Swiss resident beneficiary will be taxed as income. In practice, some tax authorities, however, do not grant the tax exemption if the settlor set up the trust shortly before he immigrated to Switzerland and declare such a pre-immigration structuring as a tax evasion.

The distribution of capital gains is not tax-free because the trust assets are not attributed to the beneficiaries for tax purposes. Distributed capital gains qualify as income.

In Switzerland no duty exists for professional trustees to register with a supervisory authority. The private industry, including many of Switzerland's largest trust companies, however founded the Swiss Association of Trust Companies (SATC), mainly to develop the activities of trustees in Switzerland and to promote the adherence to certain professional and ethical standards. SATC issued minimum standards of professional credentials and a code of ethics. In 2012 SATC published a so-called "White Paper" with various proposals on the regulation of trustees in Switzerland, namely the requirement to obtain a license to carry out trustee activities in Switzerland.

The Swiss Federal Act regarding the Fight Against Money Laundering in the Financial Sector (AMLA) is also applicable to trustees who qualify as financial intermediaries. According to the practice of the Swiss Financial Market Supervisory Authority (FINMA)20 trustees are deemed financial intermediaries as they own the trust assets separately from their personal assets. This means that trustees have among others the duty to verify the contracting party's identity, to establish the beneficial owner's identity, to clarify the economic background and the purpose of unusual transactions. In addition the AMLA provides for reporting duties on the trustee in case of any suspicious transactions. Whether protectors fall under the AMLA depends on their powers under the trust.

The foundation according to Swiss law is a legally independent purpose fund or special fund. Depending of the purpose of a foundation, it can be distinguished between the common foundation and 3 legal special forms, namely the family foundation, the ecclesiastic foundation and the personnel welfare foundation.

According to Swiss law, family foundations are characterized in such a way that property is available for a family to pay the costs of education, facilities or support of family members or for similar purposes. The family foundation is different from the common foundation in that, according to the intention of the founder, the circle of beneficiaries is limited to members of a single, specific family.

According to constant legal practice of the Federal Supreme Court, the list of purposes for which family foundation may be set up is an exclusive list. These purposes have in common that family members who belong to the circle of beneficiaries should be supported in certain circumstances.

Family foundations do not need to be registered in the commercial registry in order to obtain legal personality. They are not subject to a regulatory authority, under reservation of public law. Finally, family foundations are exempted from the obligation to mandate an auditor.

Ecclesiastic foundations are mentioned several times in the Swiss Civil Code, however, the law does not provide a legal definition of the ecclesiastic foundation.

According to legal doctrine and jurisprudence, two conditions have to be met: on the one hand, a religious purpose is required, on the other hand, there must be a specific organizational connection to a religious community. Only foundations that serve the faith in God, are ecclesiastic.

A personnel welfare foundation is often chosen as a vehicle for pension funds that serve as a continuation of living standards after retirement.

The concept of an enterprise foundation is unknown in Swiss legislation. Enterprise foundations have emerged in practice. An enterprise foundation is characterized by an economic activity and pursues a specific property investment policy. It differs from traditional foundations in its organizational structure.

There are many purposes behind establishing an enterprise foundation. The topic of estate planning in the broad sense is at the forefront.

Enterprise foundations have two main forms. Either there is a foundation that conducts a commercial, manufacturing or other business in the pursuit of an economic or non-economic purpose, and which is therefore directly the responsible body of the enterprise itself. Or there is a foundation that is a substantial shareholder of an enterprise.

Switzerland is well known for its large number of international governmental and non-governmental organizations. With all these organizations active in Switzerland, it is natural that the Swiss Charitable Foundation is a frequently used entity. The combination of a favorable tax regime and a regulated environment is an advantageous one. In addition, the Federal Circulars of December 1990 and July 1994 provide a clear description of the relevant requirements. These factors combined make the Swiss Charitable Foundation an effective estate planning vehicle, that is suitable for charitable, international and philanthropist activities.

The deeds of a Foundation need to be executed by a public notary, the Foundation is then registered at the Registry of Commerce to acquire legal personality. In general a minimum initial capital of CHF 50,000 is requested.

A foundation is incorporated either by a public deed or by a testamentary disposition (last will and testament or inheritance agreement). The foundation is entered into the commercial registry based on the Foundation Charter and indicating the members of the Foundation Council.

The Foundation Charter must indicate the organs of the foundation and the nature of its administration. For the most part, the foundation is free to determine its own organization. The way the foundation is organized can be set down in more or less detail, depending on the needs of foundation. However, it is important that the organization fosters the most efficient use of the foundation’s funds.

The superior organ within a foundation is the Foundation Council, which is responsible for the supervision of the foundation’s business. The Foundation Council assumes all competences which are not expressly delegated to another body either in the Foundation Charter or in the respective regulations. The Foundation Council performs the following unalienable tasks:

It is a common practice that a Foundation Council consists of at least three natural persons or legal entities.

Foundations are subject to supervision by the community (federal, cantonal and municipal) to which they belong according to their designation. Foundations with an international scope are usually supervised by the Federal Authorities. In order to perform the legally required controls, foundations are required to file an annual report on their activities, annual financial statements, consisting of the balance sheet, the profit and loss statement and attachments, the auditors’ report, the approval of the reporting by the Foundation Council as well as an up-to-date list of the members of the Foundation Council.

When the Foundation is exclusively in the public interest, it can obtain a tax exemption (federal and cantonal), and as such gifts made and/or received by the foundation are tax-exempt. Being dedicated to public interest means, amongst others, that the Foundation should have activities in charitable, humanitarian, educational, cultural, health or scientific areas. In addition it cannot have any lucrative business involvement and the range of beneficiaries cannot be limited. The attribution of resources is irrevocable.

The competent federal or cantonal authority may dissolve the foundation upon application or on its own initiative, if the purpose has become unattainable and the foundation cannot be maintained by an amendment to the foundation deed, or if the purpose has become illegal or immoral. Any person who has an interest is entitled to apply for the dissolution of the foundation.

The Swiss Foundation law does not recognize any possibility of reassignment, which would allow the founders after a certain period to claim back the amount contributed into the foundation or parts thereof.

The implementation of a Swiss Foundation is more complex than to set up a Foundation in the Principality of Liechtenstein. Another alternative could be the set up of an Association which could have the same purpose like a Foundation.

Establishment of a Swiss foundation is much more complex than a Lichtenstein foundation. Another option is to create an Association with the same purpose as a foundation.

PriceEUR 10 200

including incorporation tax, state registry fee, NOT including Compliance fee

PriceIncluded

Commercial Registry incorporation fee

PriceEUR 9 050

including registered address and registered agent, NOT including Compliance fee

PriceEUR 275

DHL or TNT, at cost of a Courier Service

Pricefrom EUR 10 070

Paid-up “nominee director” set includes the following documents

Company’s tax residence certificate for access to double tax treaties network

Document issued by a state agency in some countries (Registrar of companies) to confirm a current status of a body corporate. A company with such certificate is proved to be active and operating.

Compliance fee is payable in the cases of: incorporation of a company, renewal of a company, liquidation of a company, transfer out of a company, issue of a power of attorney to a new attorney, change of director / shareholder / BO (except the change to a nominee director / shareholder), signing of documents

PriceEUR 385

simple company structure with only 1 physical person

PriceEUR 165

additional compliance fee for legal entity in structure under GSL administration (per 1 entity)

PriceEUR 220

additional compliance fee for legal entity in structure NOT under GSL administration (per 1 entity)

PriceEUR 495

PriceEUR 110